PW Consulting: Vegan Probiotics Market to Grow at a Robust 7.85% CAGR Through 2032, New Report Finds

PW Consulting Releases Strategic Insight: Vegan Probiotics Market Report — Essential Intelligence for 2026 Decisions

As businesses plan resource allocation and product roadmaps for 2026, understanding where the vegan probiotics market is headed has moved from a useful input to a table-stakes requirement. PW Consulting’s new market study synthesizes five years of historical performance, near-term market dynamics, and a 2026–2032 forecast to deliver an operationally focused playbook for C-suite and investment teams. The global market has expanded rapidly through the early 2020s and, having reached approximately USD 1.25 billion in 2025, is projected to surpass USD 2.1 billion by 2032 — a compound annual growth rate of 7.85% over the forecast horizon. This trajectory underscores both attractive upside and an increasingly complex competitive and regulatory environment.

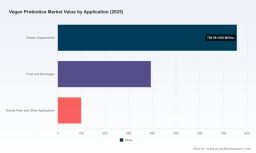

Vegan Probiotics Market

Why 2026 Is a Strategic Inflection Point

-

Market maturity meets new consumer expectations. Early adopters have validated product categories (supplements, beverages, and fortified foods). The next wave of growth will be driven by mainstreaming among flexitarian and lactose-intolerant consumers who demand clean-label, plant-based nutrition with clinically credible benefits.

Vegan Probiotics Market -

Regulatory clarity is tightening. In the U.S., probiotics are generally regulated as dietary supplements with specific labeling and claim substantiation requirements; in Europe, the pathway for health claims and novel-ingredient assessments is more stringent. These differences mean market entries and cross-border launches require bespoke compliance strategies rather than standardized global claims.

Vegan Probiotics Market -

Cost and supply-side pressures are real and quantifiable. Our industry checks show plant-based substrates and specialty media have experienced supply-chain disruptions that translated into roughly a mid-teens increase in raw material costs in recent years. At the same time, production cost drivers — notably shelf-life validation and cold-chain logistics for live cultures — elevate unit economics versus some conventional supplement lines.

-

Competitive structure is evolving. The landscape now spans global consumer brands, specialized ingredient suppliers, and nimble DTC challengers. Scale is important, but differentiation by strain, delivery format, and clinical evidence is increasingly the deciding factor for premiumization.

What the Report Delivers — Practical Outputs for Executives

Our report is built as a decision-support tool rather than as a purely academic exercise. It combines strategic narrative with actionable templates that executives can deploy immediately:

-

Executive dashboard: concise KPIs and a scenario-based outlook that isolates the variables that will matter most in 2026 (price, cold-chain cost, clinical substantiation timelines, and market access friction).

-

Commercial playbooks: go-to-market roadmaps for supplements, beverages, and fortification in packaged foods — including trade-off matrices for direct-to-consumer, retail, and foodservice channels.

-

Regulatory playbook: jurisdiction-specific guidance on labeling, permissible structure-function claims, and triggers for novel-food or GRAS pathways — essential reading for any cross-border product launch.

-

Supply chain and cost-model toolkit: unit-cost calculators that factor in cold-chain, shelf-life testing, and raw-material inflation scenarios, enabling CFOs to stress-test margins across formats and geographies.

-

Partner and M&A map: an annotated ecosystem of ingredient suppliers, contract manufacturers, and co-packing specialists ranked by capability (strain library, non-dairy media expertise, fill–finish capabilities).

-

Clinical and claims prioritization matrix: a pragmatic framework to allocate finite R&D dollars toward the studies that unlock the most valuable claims and commercial uplift.

To preserve the strategic value of the work and to ensure clients derive differentiated advantage, the report intentionally holds back detailed segment-level revenue tables and granular regional splits in this public summary. Those tables and the underlying datasets are available to subscribers and enterprise clients.

Competitive Landscape: Reading the Arena

The competitive map includes long-standing fermented-beverage specialists, mainstream supplement brands, ingredient innovators, and digitally native challengers. Key players covered in the analysis include consumer brands that have extended into vegan formulations, ingredient houses that enable plant-based productization, and challengers focused on niche positioning.

-

Incumbent beverage and culture companies continue to leverage brand heritage and distribution networks to introduce dairy-free formulations that retain heritage consumers while capturing plant-forward buyers.

-

Large supplement brands are moving aggressively into vegan probiotics in capsule and powder forms, leveraging scale manufacturing and retailer relationships to secure shelf space and private-label contracts.

-

Ingredient suppliers and strain developers are the unsung strategic lever: firms that can demonstrate strain robustness on plant-based media and provide scalable starter cultures will be prime acquisition targets.

Notable recent developments we highlight include a major supplement brand launching an expanded probiotic–prebiotic–fiber line in 2025, regulatory progress where a specialist probiotic supplier received formal safety recognition enabling broader use of a plant-adapted strain, and a 2026 product introduction from a well-known vegan beverage brand that marries probiotics with plant protein. Each of these events is discussed in the report with tactical implications for market entrants and incumbents.

Strategic Opportunities and Risk Mitigation

-

Opportunity — Formulation convergence: Combining probiotics with plant protein, prebiotics, or targeted nutraceuticals creates differentiated value propositions that resonate with health-conscious, environmentally minded consumers.

-

Opportunity — Format innovation: Beyond capsules and powders, fermented beverages and ready-to-drink formats that solve for stability/cold-chain constraints can capture new consumption occasions, especially in on-the-go and foodservice channels.

-

Opportunity — Ingredient partnerships: Strategic alliances with strain houses and contract developers reduce time-to-market and transfer technical risk associated with non-dairy propagation.

-

Risk mitigation — Cost hedging: Procurement strategies and forward contracts for specialty plant substrates, combined with flexible manufacturing agreements, help protect gross margins against ingredient volatility.

-

Risk mitigation — Regulatory playbook: Early engagement with regulatory counsel and investment in structured substantiation studies prevent costly reformulation or relabeling after launch, especially for cross-border campaigns.

Actionable Roadmap: What Companies Should Do in Q1–Q4 2026

-

For CPG incumbents: Prioritize a two-track strategy — defend core retail channels with shelf-stable, validated formulations while piloting premium, cold-chain ready SKUs for foodservice and DTC that emphasize clinical claims.

-

For ingredient suppliers and CDMOs: Invest in demonstrable plant-based propagation expertise and package stability testing; build modular supply agreements that can support co-development with mid-sized brands.

-

For private equity and strategic investors: Focus diligence on companies that control unique strain IP or possess demonstrated scale in non-dairy media; value accretive bolt-ons include clinical trial assets and fill–finish capability to lower go-to-market risk.

-

For retailers and wholesalers: Reassess category adjacencies and merchandising rules to reflect multi-format growth — consider joint promotional campaigns with brands that can substantiate claims quickly and reliably.

Methodology and Why Our Numbers Matter

The study uses 2025 as the base year, tracks historical performance over 2020–2025, and projects market outcomes across the 2026–2032 forecast window. Market sizing is expressed in USD (millions) and grounded in primary interviews with ingredient suppliers, brand managers, contract manufacturers, and channel partners, supplemented by channel shipment data and financial disclosures. Our forecast scenarios incorporate sensitivity to raw-material inflation, cold-chain cost trajectories, and regulatory timelines for health-claim validation. The resulting projected CAGR of 7.85% reflects a balance of continuing demand expansion and rising technical and compliance costs — a combination that favors strategic, well-capitalized, and technically capable players.

Closing — How This Report Shapes 2026 Strategy

For executives preparing 2026 budgets and product roadmaps, the choice is between reactive, fragmented moves and deliberate, analytically grounded action. PW Consulting’s Vegan Probiotics Market Report offers the latter: a synthesis of market sizing, regulatory intelligence, competitive mapping, and practical implementation tools designed to convert insight into market share. The public summary above highlights the forces that will shape the next phase of growth; the full report contains the granular, subscription-only datasets and operational templates needed to act with precision.

Companies assessing entry or expansion in the vegan probiotics arena should treat the coming year as an opportunity to convert technical capability into commercial differentiation. For access to the full dataset, scenario models, and bespoke advisory support, visit our client portal or contact PW Consulting’s Strategy team for an enterprise briefing and sample playbook tailored to your business model.

For detailed analysis of this topic, please visit the official page: Vegan Probiotics Market

Lacy Lee

Senior Marketing Manager

sales@pmarketresearch.com

00852-95632430

PW Consulting: www.pmarketresearch.com

Tags

PW Consulting

The Best-reviewed Subdivided Market Risk Analysis Firm in the US and East Asia.