PW Consulting Forecasts Maternal Health Devices Market to Expand at a 7.15% CAGR from 2026–2032

Maternal Health Devices Market 2026: Strategic Intelligence for Executives — PW Consulting Industry Brief

Executive summary

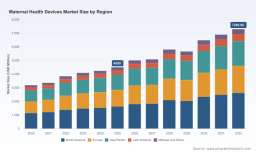

PW Consulting’s new Maternal Health Devices Market report (base year 2025; historical 2020–2025; forecast 2026–2032) arrives at a pivotal moment for medical device manufacturers, hospital systems, payors and investors. Our analysis shows a robust macro trajectory: the market expanded steadily through 2020–2025 and reached a multi-billion dollar scale by the 2025 baseline, with a projected compound annual growth rate (CAGR) of approximately 7.15% across the 2026–2032 forecasting window. This forecast reflects a convergence of regulatory enabling events, reimbursement reforms, digital-health adoption and capital investment cycles in perinatal care.

Maternal Health Devices Market

Why this matters for 2026 decision-making

-

Timing: 2026 is a strategic inflection point. New procedural CPT codes supporting remote patient monitoring became effective January 1, 2026, creating fresh pathways to monetize digital maternal-fetal monitoring services.

Maternal Health Devices Market -

Regulatory momentum: Breakthrough clearances for fully wireless platforms and beltless patch systems are accelerating clinical adoption and opening new clinical workflows in labor, delivery and the postpartum setting.

Maternal Health Devices Market -

Capital and procurement pressure: Hospitals face rising equipment and bed costs; procurement committees are prioritizing solutions that optimize bed utilization and reduce length of stay while aligning with maternal levels-of-care verification programs.

Market trajectory and structural dynamics

Our proprietary model traces the market from 2020 through 2025 and projects through 2032, capturing cyclical procurement patterns, reimbursement shifts and technology adoption curves. The market’s mid-single-digit to low-double-digit growth phases are driven by three structural forces: (1) digitization of maternal care (wearables, wireless monitoring, integrated perinatal informatics), (2) regulatory and reimbursement enablers that monetize remote and continuous monitoring, and (3) provider consolidation and certification programs that standardize risk-appropriate maternal services.

Concentration metrics reveal a market where the three largest firms account for a meaningful but not overwhelming share of total revenues (CR3 ~42.5%), while the top five firms cover a majority (CR5 ~58.8%). This structure creates a dual pathway for entrants and incumbents: scale-based competition in platform-level offerings and niche opportunities for agile innovators in wearables, consumables and software-enabled services.

Competitive landscape — what we observed

The competitive field is in flux, blending legacy medtech powerhouses with high-growth digital innovators. Established players maintain strength through broad monitoring portfolios and channel depth; smaller, focused companies are winning regulatory and clinical milestones with differentiated, wireless-first value propositions.

-

Platform incumbents: Global diagnostics and monitoring leaders continue to leverage integrated hospital solutions and enterprise contracts to protect market share. Their product roadmaps increasingly emphasize interoperability and hospital workflow integration as a means to lock in long-term service revenue.

-

Wireless innovators: New entrants focused on beltless and patch-based monitoring have secured pivotal regulatory clearances and are executing targeted commercialization strategies. These devices are reshaping patient mobility and enabling remote-care pathways that were previously impractical in obstetrics.

-

Consumables and procedure-focused vendors: Companies providing consumables and point-of-care obstetric tools are capitalizing on recurring-revenue models and clinical partnerships to maintain stable, margin-rich revenue streams.

Recent regulatory and commercial milestones reinforce these trends. Notable clearances and product expansions include wireless and beltless solutions obtaining 510(k) clearances and expanded indications, creating both opportunity and competitive risk for incumbents that rely on tethered monitoring paradigms.

Operational insights: what the report delivers

PW Consulting’s report is deliberately practical and built for executives who must convert insight into action in 2026. Key operational deliverables include:

-

A market-sizing framework calibrated to observed procurement cycles and new reimbursement codes, with scenario modeling for alternative uptakes of wireless and remote monitoring technologies.

-

A regulatory and reimbursement playbook mapping FDA pathways, CPT code adoption curves and payer contracting levers relevant to maternal-fetal monitoring and telehealth-enabled services.

-

Commercial go-to-market blueprints for four archetypal vendor strategies: platform scale-up, niche specialist, software-as-a-service aggregator and distributive-reseller model.

-

Hospital procurement and rollout templates that align clinical evidence-generation, pilot deployment and capital planning with Joint Commission verification expectations and CMS program incentives.

-

A detailed M&A and partnership roadmap including valuation sensitivity tools, integration risk matrices and prioritized target profiles for bolt-on acquisitions.

Note: The executive deliverables above are summarized to preserve the actionable intelligence contained in the full report. Detailed regional, product and end-user breakdowns, as well as price decks and addressable-market overlays, are available in the full release.

Strategic implications and recommended actions for 2026

Companies and health systems should treat 2026 as a year for decisive investment and selective consolidation. Our recommendation framework is purpose-built for boards, C-suite leaders and business unit heads tasked with near-term targets and multi-year positioning.

-

Prioritize wireless-first R&D and modular architectures: Allocate R&D spend toward interoperable, software-upgradable platforms that can support multiple clinical workflows (inpatient, ambulatory, home). This preserves upgrade pathways and reduces the need for full replacement cycles in hospital capex planning.

-

Embed reimbursement capture into product design: Align clinical evaluation plans and real-world evidence strategies with the documentation required for remote monitoring CPT codes and payor contracting. Early demonstration of clinical and economic value will accelerate coverage decisions.

-

Adopt hybrid commercial models: Combine direct enterprise sales into hospital systems with subscription-based services to create predictable revenue streams and improve unit economics. For smaller suppliers, partnerships with distribution networks can accelerate scale without heavy upfront capex.

-

Pursue selective M&A to close capability gaps: Evaluate acquisitions that provide regulatory-cleared wireless modules, home-health integration software, or perinatal analytics capabilities. Use our M&A playbook to balance strategic fit with integration risk.

-

Design pilots for care-path transformation: Work with progressive hospital systems to run tightly scoped pilots that measure clinical outcomes, nurse workload, and bed-turnover impact. These pilots should inform value-based contracting and support payor negotiations.

Implications for investors and payors

Investors should look for differentiated IP in wireless sensing, cloud-native analytics and reimbursement-aligned business models. Payors and health systems should prioritize investments that demonstrably reduce adverse maternal outcomes and downstream neonatal costs. The market’s growth profile and concentration dynamics create opportunities for both strategic investors and specialized private equity to shape category consolidation.

How the dynamics are likely to evolve through 2032

Our scenario work suggests three potential pathways depending on technology adoption speed, payor responsiveness and clinical guideline harmonization: accelerated adoption (faster shift to home and hybrid care models), steady incumbency (incremental wins for existing systems), and disruptive fragmentation (rapid emergence of multiple software-service providers). The base-case forecast assumes steady but meaningful adoption of wireless and remote monitoring technologies, supported by reimbursement and regulatory alignment, producing a continued multi-year growth trajectory at roughly the 7.15% CAGR identified for the 2026–2032 horizon.

About the PW Consulting Maternal Health Devices Market report

The report is a comprehensive strategic resource for executives and investors. It includes: full market sizing and forecast models, segmented demand analysis, regulatory and reimbursement matrices, competitive landscaping with vendor scorecards, clinical evidence sequencing, go-to-market playbooks, pricing and profitability benchmarking, and M&A candidate screening. Our methodology integrates primary interviews, hospital procurement data, device shipment and ASP proxies, and regulatory/reimbursement mapping to ensure decisions are underpinned by evidence and scenario-ready financial models.

To preserve the value of our integrated intelligence and to support client-specific advising engagements, the full report contains detailed regional, product- and end-user-level breakdowns, downloadable model workbooks and configurable scenario tools. These are available on our website and through direct engagement with PW Consulting’s healthcare strategy team.

Next steps

-

Executives: Request the full report and schedule a tailored briefing to map the findings to your product and market strategies for 2026.

-

Investors: Contact our transactions team for a hotlist of actionable targets and valuation sensitivities grounded in our sector models.

-

Health systems and payors: Engage PW Consulting to design pilots that operationalize reimbursement opportunities and measure clinical and economic impact in real-world settings.

PW Consulting’s Maternal Health Devices Market report is designed to be the operational playbook for 2026—delivering both the strategic vantage and the practical steps necessary to convert momentum into market leadership. For access to the full intelligence suite, model workbooks and bespoke advisory services, please visit our report page or contact our healthcare practice leads.

For detailed analysis of this topic, please visit the official page: Maternal Health Devices Market

Lacy Lee

Senior Marketing Manager

sales@pmarketresearch.com

00852-95632430

PW Consulting: www.pmarketresearch.com

Tags

PW Consulting

The Best-reviewed Subdivided Market Risk Analysis Firm in the US and East Asia.