PW Consulting: Transfer Glove Box Market Poised to Reach USD 418.39 Million by 2032, Backed by a 6.15% CAGR

Transfer Glove Box Market — Strategic Preview for 2026 Decision-Makers

Executive summary

PW Consulting’s latest market study on Transfer Glove Boxes provides a forward-looking, actionable framework for procurement leaders, R&D heads, and portfolio strategists planning capital and product roadmaps in 2026. At a macro level the market is established and expanding steadily: using 2025 as the base year, the total addressable market is estimated at approximately USD 275.5 Million and is projected to approach the mid‑hundreds by the end of our 2026–2032 forecast window, tracking at a 6.15% compound annual growth rate (CAGR). Market concentration remains moderate, with the top three and top five suppliers controlling meaningful but not overwhelming shares—an important context for competitive sourcing and partnership strategies.

Transfer Glove Box Market

Why this matters for 2026

-

Capital timing: With hospital and pharmaceutical capital cycles showing elevated spend and aging assets, 2026 will be a year when many organizations decide whether to retrofit existing containment systems or invest in next‑generation glove box platforms.

Transfer Glove Box Market -

Regulatory inflection: Ongoing enforcement and clarification of sterile processing standards (FDA guidance and EU GMP Annex 1) and compounding/containment expectations (USP <797> and USP <800>

make compliance-driven upgrades unavoidable for many operators.

make compliance-driven upgrades unavoidable for many operators.

Transfer Glove Box Market -

Technology convergence: Demand drivers from advanced therapeutics, high-potency APIs, and materials science (including battery R&D) are broadening the technical requirements for transfer systems—forcing purchasers to balance bespoke engineering against scalable, serviceable platforms.

Market trajectory — what the headline figures imply

The market’s steady CAGR of 6.15% reflects a mix of replacement demand, regulatory-led upgrades, and new greenfield installs across life sciences, electronics, and specialty manufacturing. The near‑term plateau around our 2026 estimate signals a short window for firms to lock in supplier commitments before a re-acceleration driven by larger programmatic investments later in the decade. For executives, the takeaway is clear: decisions taken in H1–H2 2026 will disproportionately affect capital deployment and supplier relationships through 2028–2029.

Competitive landscape — patterns, not plateaus

The supplier ecosystem for transfer glove boxes is characterized by a blend of specialist manufacturers and larger, diversified equipment providers. Several strategic themes dominate:

-

Specialist engineering and containment excellence: Manufacturers with deep expertise in stainless steel isolators and containment engineering continue to command premium positioning for high-potency and radiopharmaceutical applications. Their value proposition rests on validated leak-tight designs, advanced transfer systems, and compliance-first documentation.

-

Modularity vs. integrated systems: Some vendors emphasize modular PMMA and adaptable envelope solutions that can be reconfigured across workflows; others push integrated vacuum and DPTE-style transfer systems as turnkey solutions for aseptic API handling. Buyers should evaluate which approach minimizes total cost of ownership (TCO) for their specific operating profile.

-

Service and aftermarket as differentiation: With market concentration indicating a competitive but not monopolistic landscape, aftersales service, validation support, and spare parts logistics are increasingly decisive in procurement decisions.

Key vendors profiled in the report include European specialists known for high-containment stainless steel systems, Italian engineering houses with strong radiopharmaceutical and aseptic interfacing expertise, established North American manufacturers supplying sterile compounding isolators, and modular solution providers targeting laboratory and semiconductor research. Each vendor is assessed on product architecture, regulatory tooling, aftermarket readiness, and channel footprint.

Recent vendor moves and regulatory context

-

Product innovation: Several vendors launched or updated containment platforms in 2025, expanding product lines for radiopharmacy synthesis and Annex 1-compliant aseptic isolators. These announcements evidence a shift toward purpose-built solutions for narrow, high-value use cases.

-

Regulatory drivers: The industry continues to operate under the twin imperatives of ISO 5 (Class 100) critical-zone control for aseptic processes and updated compounding standards that mandate rigorous containment for hazardous drugs. Compliance with USP <797> and USP <800> remains a gating factor in procurement specifications.

-

Capital environment: Hospitals and health systems maintained elevated capital expenditures into FY24 and FY25, amplifying replacement cycles for containment equipment. Procurement teams should model financing and leasing options as part of 2026 purchasing strategies to manage balance-sheet impacts.

Strategic implications by buyer profile

-

Pharmaceutical manufacturers and CMOs: Prioritize suppliers that demonstrate validated aseptic transfer interfaces and robust leak-testing regimes. Expect multi-year service contracts and FAT/SAT processes to add 8–12% to project budgets—factor these into procurement timelines.

-

Radiopharmacy and nuclear medicine sites: Specialized vendor capabilities (containment for specific isotopes and regulatory compliance attestations) will be non-negotiable. Shortlist vendors that can provide documented compliance with cETL/us and similar regional certifications.

-

Academic and industrial research labs: Flexibility and rapid deployment matter most. Consider portable and modular enclosures that allow for frequent reconfiguration; evaluate suppliers with strong standardization to reduce lead times and validation overhead.

-

Battery and semiconductor R&D: Atmosphere control and particulate management are the differentiators. Engage vendors early to co-develop interface standards that preserve R&D throughput while ensuring operator safety.

What 2026 procurement teams should do — an actionable checklist

-

Run a compliance gap analysis that maps your existing processes against FDA/EU Annex 1 and USP <797>/<800> requirements. Identify containment elements that are vulnerable to inspection or product loss.

-

Adopt a supplier scorecard that weights engineering validation, aftermarket SLAs, spare parts logistics, and lifecycle cost—don’t let up-front price dominate the decision.

-

Model three financing scenarios (outright purchase, capital leasing, and performance-based contracts) to maintain flexibility given the elevated capital intensity in the sector.

-

Pilot before scale: for non-standard processes or high-value payloads, run a short-term pilot with clear KPIs (containment performance, throughput impact, validation time) to de-risk full rollouts in 2027–2028.

-

Prioritize vendors that offer documented regulatory support and pre-packaged validation protocols to shorten qualification cycles and reduce internal QA burden.

What the PW Consulting report contains (practical deliverables)

The full study is designed as a procurement-to-deployment playbook. It combines proprietary quantitative modeling with practical tools, including:

-

A base-year market model (2025) and a seven-year forecast (2026–2032) with scenario-based sensitivity analyses tied to regulation and capital-cycle assumptions.

-

Vendor playbooks: product architecture maps, service & spare-parts assessment, and validated checklists for FAT/SAT and qualification activities.

-

Procurement templates: weighted supplier scorecards, RFQ language tailored to aseptic and hazardous-compound use cases, and an ROI/TCO calculator designed for glove box investments.

-

Operational readiness modules: installation and retrofit roadmaps, environmental monitoring sampling plans aligned with ISO and USP guidance, and a risk register with mitigation playbooks.

-

Go-to-market intelligence for vendors: segmentation frameworks, partnership matrices, and aftermarket growth strategies (service bundles, consumables, validation-as-a-service).

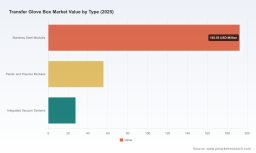

Note: To preserve competitive sensitivity and focus readers on strategic decision-making rather than raw segment figures, the report abstracts detailed regional and application splits in the public summary. Paid subscribers receive the full segmentation tables, regional build-outs, and granular pricing benchmarks necessary for contract negotiation.

How buyers and suppliers should position for 2026

-

Buyers: Treat 2026 as a window to secure long-term service relationships while prices remain competitive. Use pilots and staged rollouts to validate supplier claims and reduce integration risk.

-

Suppliers: Differentiate through validated compliance, shortened lead times, and creative aftermarket financing. Vendors that can bundle equipment with validation and monitoring services will capture higher lifetime value.

-

Private equity and strategic investors: The sector’s moderate concentration and consistent growth profile create selective opportunities—particularly for service-oriented businesses and firms with strong IP in containment engineering.

Methodology and confidence

Our analysis combines historical shipment and revenue tracking (2020–2025), primary interviews with procurement and technical leaders across end markets, vendor financials, and policy/trend overlays. Confidence intervals reflect a base-case CAGR of 6.15% through 2032, with scenario bands that capture regulatory tightening and capital-cycle shifts. Market concentration metrics indicate room for competitive entry but reward technical differentiation and post-sales service excellence.

Next steps — where to get the full intelligence

This article is a strategic preview intended to surface the high‑impact choices facing organizations in 2026. The full PW Consulting Transfer Glove Box Market report contains the granular segmentation, regional demand curves, supplier scorecards, and downloadable procurement templates needed to operationalize these insights. For licensing, bespoke briefings, or to request the complete dataset and vendor-ready RFQ templates, visit our report page or contact the PW Consulting industry team.

For detailed analysis of this topic, please visit the official page: Transfer Glove Box Market

Lacy Lee

Senior Marketing Manager

sales@pmarketresearch.com

00852-95632430

PW Consulting: www.pmarketresearch.com

Tags

PW Consulting

The Best-reviewed Subdivided Market Risk Analysis Firm in the US and East Asia.