PW Consulting: CNF Software Market Poised to Expand at a 22.4% CAGR During 2026–2032PW Consulting Forecasts 5.28% CAGR for Anti COVID‑19 Compound Library Market Through 2032

PW Consulting Strategic Brief: CNF Software Market — A 2026 Decision-Maker’s Playbook

Executive snapshot

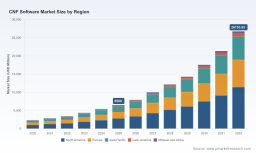

Cloud-Native Network Functions (CNFs) have moved from experimental lab projects to strategic production programs. Our newest Cnf Software Market report — with base year 2025 and a forecast spanning 2026–2032 — shows a market that expanded rapidly over the first half of the decade and is set to scale materially through 2032 at a compound annual growth rate (CAGR) of 22.4%. The market was approximately USD 6.5 billion in 2025 and, at current trajectories, is expected to reach roughly USD 26.8 billion by 2032. For infrastructure owners, service providers, system integrators, and hyperscalers, 2026 is a pivot year: choices made now determine competitive positioning and total cost of ownership across the next technology cycle.

Cnf Software Market

Why this report matters for 2026 strategic decisions

-

Timing: With CNF deployments transitioning from pilots to multi-site production, 2026 is the year to shift from proof-of-concept risk-tolerance to industrial-scale economics and governance.

Cnf Software Market -

Vendor economics: The market displays moderate concentration among top vendors (CR3 ~42.5%, CR5 ~58.2%), meaning incumbents still hold significant influence while specialized suppliers and open-source integrators have meaningful runway to capture differentiated niches.

Cnf Software Market -

Standards and portability: Cloud-native toolchains — notably Kubernetes aligned with ETSI NFV MANO patterns and Container Infrastructure Service Management (CISM) practices — are maturing. This reduces lock-in risk but raises integration and certification requirements that buyers must explicitly manage.

-

Talent and operations: The developer pool supporting cloud native has expanded dramatically — industry tracking noted nearly 20 million cloud-native developers in Q1 2026, with rapid growth in specialized skills. This labor dynamic is reshaping build-versus-buy calculus and outsourcing models.

What the report delivers — practical, operational guidance

This is not a conceptual market essay. The report is a practitioner's toolkit designed to convert CNF momentum into repeatable, low-risk deployments. Key deliverables include:

-

Vendor benchmark and interoperability matrix: independent scoring across performance, cloud portability, observability, security posture, and ecosystem certifications.

-

Migration playbooks: phased transition paths from legacy VNFs to CNFs, including fall-back strategies for service continuity and blue/green deployment patterns for 5G workloads.

-

Architecture blueprints: validated reference architectures for public, private, and hybrid cloud models aligned to telecom-grade resiliency and latency targets.

-

TCO and risk models: scenario-based financial models that quantify capex/opex trade-offs, developer and operational staffing impacts, and risk-adjusted ROI for multi-year programs.

-

Certification and compliance mapping: how to structure third-party validation, how to use CNF certification programs effectively, and what to expect from operator acceptance criteria.

-

Implementation checklists and runbooks: operational playbooks for CI/CD pipelines, observability stacks, security hardening, and DPU/accelerator integration.

Competitive landscape — who matters and why

The vendor ecosystem is heterogeneous: large network equipment vendors, cloud-native platform companies, security specialists, and focused CNF product firms. Our analysis profiles strategic strengths and trade-offs among leaders and innovators to help procurement and architecture teams prioritize engagements.

-

Nokia (Espoo, Finland) — Strength: deep telco CNF portfolio for packet core and communication suites optimized for Kubernetes. Strategic value: operator-grade CNFs with strong commitments to CNCF contributions and telecom reliability practices. Ideal for service providers requiring integrated core CNF stacks with proven field validation.

-

Ericsson (Stockholm, Sweden) — Strength: dual-mode 5G core CNFs and cloud-native infrastructure centric solutions with a growing third-party CNF certification program. Strategic value: an emerging hub for open CNF ecosystems; useful where operators mandate certified interoperability for multi-vendor deployments.

-

F5 (Seattle, USA) — Strength: advanced traffic management and security CNFs with DPU-acceleration and recent innovations focused on edge and 5G. Recent product releases (May 2026) add features like provider-edge MPLS support, accelerated data plane on NVIDIA BlueField DPUs, and deeper integration with Red Hat OpenShift. Strategic value: performance-sensitive data-plane functions and edge deployments where acceleration matters.

-

Cisco (San Jose, USA) — Strength: broad CNF portfolio including containerized broadband and mobile network functions backed by deep routing and service assurance expertise. Strategic value: large operators and enterprises that favor integrated stack support across traditional networking and cloud-native boundaries.

-

Ribbon Communications (Plano, USA) — Strength: CNF versions of session border controllers, policy and routing, and IMS core. Strategic value: vendors with legacy voice/data logic who can accelerate operator migrations with functionally equivalent CNF offerings.

-

Titan.ium Platform (Canada) — Strength: specialist CNFs for signaling, routing, subscriber data management, and security with microservices-first designs. Strategic value: focused platforms for greenfield 5G and edge deployments where agility and microservice granularity are priorities.

-

Red Hat (Raleigh, USA) — Strength: OpenShift as the de facto enterprise Kubernetes platform with validated partner integrations across Nokia, Ericsson and F5 CNFs. Strategic value: platform-level certification and lifecycle management for operators standardizing on OpenShift-based CNF stacks.

Recent ecosystem developments you cannot ignore

-

Product and acceleration: F5’s May 2026 release and subsequent partnerships amplify a trend — CNFs are increasingly integrated with DPU and accelerator technologies. If your use case requires deterministic data-plane performance, hardware-accelerated CNFs shift the architecture conversation.

-

Open validation and certification: Ericsson’s expanded third-party CNF certification program is an indicator — operator-grade acceptance will increasingly depend on formal validation against cloud-native infrastructure stacks.

-

Developer base and skills: industry data from Q1 2026 confirms a surge in cloud-native development capacity. While this increases hiring options, it also raises the cost of experienced telecom-grade CNF engineers and makes triage of partner-delivered managed services essential.

-

Standards alignment: Kubernetes + ETSI NFV MANO patterns and CISM practices are becoming normative for orchestration and operations. Architecture and procurement must explicitly require compliance and roadmaps for upstream contributions.

Practical strategic recommendations for 2026

-

Define a minimum viable production (MVP) standard: require vendor proof-points for orchestration, observability, failover, and recovery at scale rather than accepting lab-only demos.

-

Prioritize interoperability tests and third-party certification as gating criteria in RFPs — not just feature checklists. Certification is now a differentiator for deployment risk reduction.

-

Adopt a cloud-agnostic lifecycle policy: require CNFs to support validated deployment on target Kubernetes platforms (including OpenShift where applicable) and define clear SLAs for portability and day-two operations.

-

Invest in a small center of excellence (CoE) for CNF operations in 2026: the CoE should house architects, platform engineers, and SREs who can run CI/CD, observability, and security pipelines to accelerate vendor onboarding.

-

Make performance acceleration part of architecture assessments: include accelerator (DPU/NIC offload) readiness in proof-of-concept criteria for data-plane-heavy CNFs.

-

Model staffing vs managed services: use scenario financials to compare hiring skilled CNF engineers versus contracting validated managed service partners — account for tooling cost, training ramp, and provider SLAs.

-

Enforce a telemetry-first posture: require CNFs to emit standardized metrics, traces, and structured logs to integrate seamlessly into centralized observability and assurance platforms.

How this report supports procurement and program leads

The report equips decision-makers with the evidence, templates, and decision logic required for 2026 procurement cycles. It translates macro growth and concentration trends into actionable vendor shortlist criteria, financial scenarios, and an implementation calendar aligned to carrier rollouts and enterprise cloud strategies. Our vendor scoring and playbooks are purpose-built to reduce procurement friction and accelerate time-to-service without sacrificing resilience.

Next steps and call to action

2026 will be defined by a bifurcation: organizations that convert CNF capability into operational advantage, and those that re-run legacy architectures on cloud wrappers with marginal gains. PW Consulting’s Cnf Software Market report provides the operational roadmaps, vendor intelligence, and financial models to ensure your program is in the first group. For the complete set of segmented findings, validated vendor scores, and the granular implementation matrices that underpin our recommendations, please consult the full report on our website.

For executive briefings, program workshops, and customized migration modeling aligned to your network and cloud portfolio, contact PW Consulting to schedule a strategy session.

For detailed analysis of this topic, please visit the official page: Cnf Software Market

Lacy Lee

Senior Marketing Manager

sales@pmarketresearch.com

00852-95632430

PW Consulting: www.pmarketresearch.com

Tags

PW Consulting

The Best-reviewed Subdivided Market Risk Analysis Firm in the US and East Asia.