PW Consulting: Electronic Bird Repellent and Control Devices Market Poised for 7.85% CAGR on Rising Agricultural and Aviation Demand

Electronic Bird Repellent And Control Devices Market: Strategic Insights for 2026 — PW Consulting

Executive snapshot

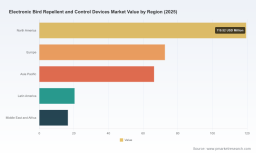

PW Consulting’s latest market study on Electronic Bird Repellent and Control Devices (base year 2025; forecast period 2026–2032) equips executives with the actionable intelligence needed to make confident decisions in 2026. The market, measured in USD Million, recorded notable expansion through 2020–2025 and stood at approximately USD 295.4 Million in 2025. Our forecast shows a sustained compound annual growth rate (CAGR) of 7.85% across 2026–2032, with the market trajectory pointing toward roughly half-a-billion dollars by the end of the forecast horizon. This growth is being driven by converging forces: technological innovation, changing biosecurity priorities in agriculture and aviation, rising commercial and municipal investments in humane wildlife control, and uneven regulatory landscapes that create both constraints and opportunities for differentiated solutions.

Electronic Bird Repellent And Control Devices Market

Why this report matters for 2026 decision cycles

-

Board-level planning: Our report translates market momentum into strategic options — buy, build, partner, or defer — with risk-adjusted scenarios calibrated to a 2026 planning window.

Electronic Bird Repellent And Control Devices Market -

Procurement and capex: We provide procurement-ready evaluation frameworks that quantify installation timelines, lifecycles, and payback ranges for key technology archetypes.

Electronic Bird Repellent And Control Devices Market -

R&D and product roadmaps: For technology owners and OEMs, the study highlights where investment in AI, sensors, and non-lethal deterrent mechanisms will most likely convert into commercial advantage.

-

M&A and corporate development: The competitive concentration metrics in the report show a market with clear leaders but meaningful opportunity for consolidation and bolt-on acquisitions in high-value niches.

What the report contains — practical, operational, and decision-focused

-

Robust market sizing and scenario modeling: We detail our methodology and assumptions used to derive the 2020–2025 history and 2026–2032 forecasts (USD Million basis), including sensitivity cases for accelerated AI adoption, regulatory tightening, and raw-material disruptions.

-

Segmentation intelligence without the noise: The market is segmented by product type (e.g., ultrasonic devices, laser systems, sound/acoustic repellers, electric track and visual deterrents), application (agriculture, aviation, commercial/industrial, residential), and region — each segment is analyzed for growth drivers, adoption barriers, and margin dynamics. Note: this release intentionally previews segment structures; granular figures and allocation tables are available in the full report.

-

Supplier heatmaps and capability matrices: We map vendors across technology readiness, service delivery, and geographic coverage to support shortlist creation for pilot and procurement rounds.

-

Operational playbooks: Includes deployment checklists, integration templates for combining electronic deterrents with physical barriers, and standardized testing protocols to measure efficacy across flight heights, species, and environmental conditions.

-

Commercial frameworks: Pricing benchmarks, channel economics, and tender templates tailored for airport authorities, agribusiness integrators, and municipal customers.

-

Regulatory and environmental compliance matrix: Jurisdiction-by-jurisdiction guidance highlighting where sonic/ultrasonic devices face legal limits or public pushback and how to design mitigation strategies accordingly.

-

Case studies and ROI calculators: Field-proven deployments with anonymized performance metrics, plus customizable ROI models to support business cases for pilots and rollouts.

Competitive landscape — who matters and why

The market displays a mix of long-standing manufacturers, specialist technology players, and newer entrants leveraging data and automation. Market concentration is meaningful but not prohibitive: the top three firms account for a significant share of revenue, while the top five widen that share materially, signaling room for mid-market vendors and innovators to gain traction in niche segments.

-

Bird-X, Inc. (Elmhurst, IL, USA) — A legacy player with a diversified portfolio spanning ultrasonic, sonic, and laser systems and deep distribution channels for both commercial and residential channels. Recent product introductions expanded their liquid deterrent and UV-marker offerings, and prior acquisitions have broadened their tech set. Bird‑X remains a model for scale-focused product diversification and route-to-market breadth.

-

Bird Control Group (Delft, Netherlands) — Known for AVIX automated and handheld laser systems, the company is a bellwether for laser deterrent adoption in agriculture and airports. Their patented approaches show how focused IP and performance claims can command specialized contracts, particularly where non-invasive methods are required.

-

Bird Gard LLC (Sisters, OR, USA) — A specialist in bioacoustic solutions. Their species-specific distress and predator-call systems illustrate demand for solutions tailored by ecology and crop type, underscoring the commercial value of behavioral science fused with electronics.

-

Bird Barrier America, Inc. (Carson, CA, USA) — Blends electronic deterrents with physical exclusion products; their integrated approach is increasingly attractive to customers seeking single-source providers capable of delivering both products and installation services.

-

Nixalite of America, Inc. (East Moline, IL, USA) — A manufacturing stalwart whose long-standing production base and emphasis on stainless steel and ruggedized components highlights the role of durable supply chains in preserving margins and field reliability.

-

iCHASE Co., Ltd. (Taipei, Taiwan / US presence) — A recent example of tech-led disruption: the company’s AI-powered deterrent with computer-vision tracking and adaptive strategies was introduced in late 2025 and signals a broader shift toward data-enabled deterrence, continuous monitoring, and closed-loop optimization.

Recent industry dynamics and implications

-

Innovation acceleration: The market is bifurcating between hardware-centric solutions and sensor/AI-driven systems that monetize data. The rollout of AI-enabled products that include tracking and adaptive behavior modification is a key inflection point for product roadmaps and service monetization.

-

Regulatory friction: Several jurisdictions are restricting sonic and ultrasonic devices on noise-pollution grounds. Where such restrictions exist, customers prefer laser, visual, or bioacoustic options — and suppliers must be prepared with compliance and community engagement strategies.

-

Supply chain realities: Electronic systems rely on specialized components (speakers, optics, stainless steel assemblies). Established manufacturers with local production capabilities or long-term supplier contracts are better positioned to manage lead times and quality control.

-

Consolidation signal: Given the reported concentration dynamics, M&A activity is likely to accelerate in adjacent niches — e.g., bioacoustics, AI analytics, or specialized laser systems — as larger firms seek to fill capability gaps quickly.

Strategic recommendations for 2026

For corporate leaders, public agencies, and investors, the following prioritized actions translate market understanding into concrete moves for 2026.

-

Immediate (0–6 months) — Launch targeted pilots with vendors that offer data capture and measurable efficacy; require vendors to provide anonymized performance baselines and standardized KPIs. If procurement spans urban/municipal settings, pre-screen suppliers for regulatory compliance and community-noise mitigation plans.

-

Near term (6–18 months) — Evaluate strategic partnerships or minority investments in AI-enabled specialists to secure access to telemetry and machine-learning models that improve deterrent performance over time. Standardize procurement templates and SLAs to include software updates, raw-data access, and translation of field metrics into ROI.

-

Medium term (12–24 months) — Build modular integration strategies that combine electronic deterrents with proven physical barriers. For multi-site operators (airports, large farms), prioritize vendors that can deliver managed services and remote monitoring to reduce on-site resource requirements.

-

Longer term (18–36 months) — Consider consolidation plays to internalize critical IP (bioacoustics, computer vision, laser optics) and to create compelling bundled offerings. Hedge regulatory risk by diversifying product portfolios across noise-neutral technologies.

How PW Consulting’s report supports these actions

The report is designed as an operational toolkit for decision-makers. It includes practical templates (tender language, test protocols, KPI dashboards), a prioritized shortlist of vendor archetypes, and scenario-based financial models to stress-test investment cases under different adoption and regulatory scenarios. For teams preparing 2026 budgets, the combination of a clear market growth rate (7.85% CAGR) and our practical deployment guidance reduces execution risk and shortens time-to-value for pilots and rollouts.

Next steps and access

This article previews the strategic depth inside PW Consulting’s full Electronic Bird Repellent and Control Devices Market report. If your 2026 planning requires detailed segment allocations, granular regional splits, vendor-level financials, or access to our supplier heatmaps and ROI calculators, please consult the full report. PW Consulting can also provide tailored briefings and a client workshop to translate these market insights into a bespoke action plan for your organization.

For detailed analysis of this topic, please visit the official page: Electronic Bird Repellent And Control Devices Market

Lacy Lee

Senior Marketing Manager

sales@pmarketresearch.com

00852-95632430

PW Consulting: www.pmarketresearch.com

Tags

PW Consulting

The Best-reviewed Subdivided Market Risk Analysis Firm in the US and East Asia.