PW Consulting: TV ODM Market Poised for 3.8% CAGR (2026–2032) as Asia‑Pacific Leads Global Demand

Tv ODM Market 2026: Strategic Imperatives from PW Consulting’s New Industry Brief

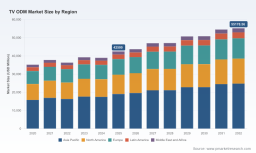

PW Consulting’s latest Tv Odm Market report (base year 2025; forecast 2026–2032) reframes how industry leaders should approach supplier selection, capacity planning and product-roadmap investments in 2026. With the global TV ODM market estimated at approximately USD 42.5 billion in 2025 and projecting a compound annual growth rate (CAGR) of 3.8% over the 2026–2032 forecast window, the sector is entering a phase where structural cost pressures, supply-chain realignment and selective technology upgrading will decide winners and losers. This briefing summarizes the strategic value of the full report for corporate decision-makers while deliberately reserving the granular segment and regional tables to the full research package.

Tv Odm Market

Why this report matters for 2026 decisions

-

Timing: 2026 marks a transition from post-pandemic demand rebound to a structurally mature market. Incremental growth exists, but margins will be determined by cost control and execution speed rather than top-line expansion alone.

Tv Odm Market -

Cost sensitivity: Display panels now represent a dominant share of TV manufacturing cost. Early 2026 saw panel and component cost inflation—large-size LCD panels registered upward pressure—exposing OEMs and ODMs to margin squeezes if procurement and product-mix decisions are not realigned.

Tv Odm Market -

Policy risk and sourcing: Geopolitical and trade policy moves, including discussions in major markets around tariffs on imported display components, introduce execution risk for China-centric supply chains and elevate the value of diversified manufacturing footprints.

What’s inside the full Pw Consulting Tv Odm Market report

-

Comprehensive market model (2020–2025 historical; 2026–2032 forecast) with revenue flows and sensitivity tests that model price, volume and component-cost shocks.

-

Bottom-up cost build for representative TV assemblies, showing component-level margins and where price pass-through is feasible across product tiers.

-

Practical supplier playbooks: criteria-based selection matrices, contract terms to prioritize, and dual-sourcing architectures for mitigating tariffs and logistic risk.

-

Supply-chain maps and capacity overlays, including factory commissioning timelines and near-term capacity additions, to help planners avoid bottlenecks.

-

Competitive intelligence packets profiling leading ODMs, key customers, proprietary capabilities, and M&A possibilities—structured to support vendor prioritization and partner diligence.

-

Scenario analyses (tariff shock, panel-price spike, demand softness) with recommended mitigation playbooks and trigger points for contingency actions.

-

Actionable M&A and JV decision framework for vertical integration, capacity acquisition or brand-led product differentiation strategies.

Note: To preserve strategic value for licensors and buyers, the public brief intentionally omits granular regional/application splits and detailed price matrices found in the full report available from PW Consulting.

Market outlook — what the numbers imply

Our forecast anticipates the global TV ODM market will grow from the 2025 base to a larger market by 2032, with mid-single-digit CAGR reflecting an industry shaped by incremental unit demand, rising ASPs in premium tiers, and cost pressures from key inputs. The trajectory is not uniform: supply-side capacity moves, panel-price volatility and segment-specific adoption (e.g., higher-value backlight and emissive technologies) will create pockets of above-market performance alongside areas of intense margin competition.

Two structural points matter for 2026 planning:

-

Panel and component costs now drive margin volatility. Display panels account for a substantial percentage of manufacturing cost; small percentage swings in panel pricing or IC costs can materially alter unit economics for mid- and large-size SKUs.

-

Capacity additions and realignments are material and rapid. Several contracted manufacturers have announced or commissioned new capacity lines and international expansions—moves that re-shape order-book availability and bargaining power for major brands.

Competitive landscape — reading the supplier map for partnership strategy

The ODM landscape combines a handful of very large, diversified contract manufacturers with several specialist and regional players. Market concentration metrics indicate the top-three and top-five players together command a meaningful share of the market, creating a dynamic in which scale, integrated supply-chains and capacity availability are decisive negotiation levers.

-

MOKA (TCL MOKA) — A leading turnkey TV ODM with strong shipment history and access to the TCL ecosystem. Its positioning as a full-service ODM and recent platform partnerships make it an attractive partner for brands seeking rapid SKU expansion with integrated software and hardware support.

-

AMTC — Deepening its international footprint with significant capacity builds in low-cost manufacturing locations, targeting North America and broader export markets. Their strategic factory expansions are designed to capture allocation from brands pursuing market diversification.

-

HKC — A top-tier OEM/ODM and panel supplier partner with diversified factory sites and new large-scale capacity online. HKC’s mix of brand customers and multiple manufacturing bases provides options for brands requiring scale and geographic spread.

-

Express Luck, TPV, BOE, Foxconn and others — Each brings a differentiated play: Express Luck with rapid scale-up plans from specialized parks; TPV with monitor-to-TV convergence expertise; BOE and Foxconn with vertical integration and global OEM credibility. These providers form the backbone of large contract programs and influence component allocation dynamics.

Recent operational moves underscore the competitive shifts: commissioning of new high-capacity plants, ODM-platform partnerships to accelerate smart-TV rollouts, and trade-show engagements to showcase turnkey solutions. These actions tighten capacity timelines and accelerate commoditization of some services while creating premium pockets around platform integration and advanced display technologies.

Strategic implications and recommended actions for 2026

For executives planning the 2026 roadmap, the report translates market signals into prioritized actions across four constituencies: brands/OEMs, ODMs/suppliers, retailers/distributors, and financial sponsors.

-

Brands & OEMs — Treat 2026 as a year to reallocate risk: (a) lock mid-term panel supply agreements with price escalation clauses; (b) adopt layered sourcing (home-region + alternate low-cost sites) to mitigate tariff or logistic disruptions; (c) consolidate platform partners for software and service bundles where differentiation matters.

-

ODMs & Contract Manufacturers — Prioritize capacity elasticity and vertical cost capture. Investments in flexible production lines, closer integration with panel suppliers, and offering platform-level services (UI/OS, certification support) will command premium margins versus pure box-building.

-

Component Suppliers — Expect buyers to push down the supply chain risk. Offer structured hedging solutions, multi-year contracts with minimum volumes, and co-investment models for factories to lock in allocation.

-

Private equity & strategic investors — Seek targets that combine scale with unique software/platform capabilities or localized manufacturing advantages. The most attractive assets will be those that can de-risk panel procurement and deliver platform-led differentiation to brand customers.

Operationally, PW Consulting recommends immediate steps for 2026 planning horizons:

-

Begin Q3 2026 supplier re-negotiations with explicit clauses for tariff-triggered adjustments and extended lead-time commitments.

-

Run a two-scenario procurement stress-test: (1) moderate panel price rise, (2) tariff shock plus panel-IC inflation. Use outputs to set inventory targets and safety-stock policies.

-

Prioritize ODMs that can deliver turnkey platform integration (HW + OS + app ecosystem) if your customer proposition depends on rapid time-to-market for smart-TV features.

-

For product strategy, combine targeted investment in premium display technologies with a disciplined cost roadmap for mainstream SKUs to avoid margin erosion driven by component cost swings.

How PW Consulting supports 2026 execution

Our full Tv Odm Market report provides the granular datasets, supplier scorecards and scenario models necessary to operationalize the recommendations above. PW Consulting also offers bespoke advisory services: supplier diligence, contract negotiation support, tariff-impact modeling and transaction advisory for M&A or JV activity in the TV supply chain.

To preserve the commercial integrity of our datasets, detailed regional and application splits and the full company-level financial tables are available only in the complete report and through our client portal. If your 2026 strategy depends on precise capacity maps, supplier allocation scenarios or granular SKU-level economics, access to the full report is a recommended first step.

Next steps

-

Download the executive dataset and order the complete Tv Odm Market report from PW Consulting for access to the full segmentation, scenario workbooks and vendor scorecards.

-

Book a strategic briefing with our TV & Display practice to translate findings into a 90–180 day action plan tailored to your role—brand, retailer, supplier or investor.

In a market where panel economics, policy shifts and manufacturing agility will dictate competitive positioning in 2026, the right information and the right partner will determine whether you protect margins, win shelf space, and capture the next wave of premium demand. PW Consulting’s Tv Odm Market report is designed to make those decisions clearer and executable.

For detailed analysis of this topic, please visit the official page: Tv Odm Market

Lacy Lee

Senior Marketing Manager

sales@pmarketresearch.com

00852-95632430

PW Consulting: www.pmarketresearch.com

Tags

PW Consulting

The Best-reviewed Subdivided Market Risk Analysis Firm in the US and East Asia.