PW Consulting: E‑Beam Accelerators Market Poised to Grow at a 4.15% CAGR During 2026–2032, New Insight Predicts

E Beam Accelerators Market — Strategic Preview for 2026

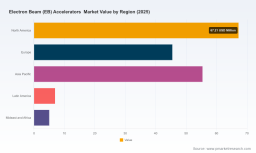

PW Consulting’s new E Beam Accelerators Market briefing is designed as a decision-grade orientation for executives preparing capital, product, and go-to-market choices in 2026. The market has demonstrated steady, measurable growth from the early 2020s and — based on our baseline models — is expected to progress from an estimated USD 180.0 Million in 2025 to roughly USD 270.0 Million by 2032 at a compound annual growth rate (CAGR) of 4.15%. This preview highlights the strategic implications of those macro dynamics, explains how the full report translates them into operational choices, and points to the tactical actions senior leaders should be primed to take in the coming 12–24 months.

E Beam Accelerators Market

Market trajectory and what it means for corporate planning

The electron beam (E-beam) accelerators market has moved beyond niche laboratory use to an increasingly commercial and industrial footing. Historical performance through the 2020–2025 base period shows a resilient recovery and diversification of demand — a pattern our forecast extends across 2026–2032. The steady mid-single-digit CAGR masks important asymmetries: pockets of rapid adoption where regulatory or quality imperatives (for example, medical sterilization or food safety initiatives) intersect with industrial process economics; and slower uptake where incumbent thermal or chemical approaches remain entrenched.

E Beam Accelerators Market

For 2026 planning cycles, the headline numbers imply two practical things for decision makers:

E Beam Accelerators Market

- Time window for conversion: the market’s growth profile supports multi-year ROI horizons for capital-intensive installations, but also rewards staged deployment (pilots → scale) to de-risk technology fit and throughput assumptions.

- Segmentation-driven returns: aggregate growth is meaningful, but value accrues unevenly across energy classes, applications, and geographies — making targeted strategy and supplier selection essential to extract premium margins.

What the full PW Consulting report delivers (operationalized)

This brief is a deliberate entry point. The full intelligence packet is built to be directly executable for procurement, strategy, and M&A teams and includes:

- Forecast models with scenario sensitivity (base, accelerated adoption, technology disruption) and downloadable worksheets you can plug into internal financial models.

- Benchmarking dashboards that compare vendors on technical performance, total cost of ownership (TCO), service ecosystem, and installation footprint.

- Practical vendor selection frameworks — scoring matrices that align technical specifications (energy class, throughput, footprint) with end-use KPIs (yield, cycle time, regulatory compliance).

- Regulatory and standards risk mapping tailored to major markets and verticals, plus an escalation matrix for certification timelines and contingency routing.

- Sample RFPs, commissioning checklists, and operational validation protocols to shorten procurement and commissioning cycles.

- Strategic playbooks for three common enterprise objectives: capacity expansion (sterilization/medical), product differentiation (materials modification), and vertical integration (build-to-own irradiation capabilities).

- M&A screening filters and synergy calculators to evaluate tuck-in targets or platform acquisitions in a market with concentrated yet fragmentary capability.

Dynamics shaping 2026 decisions — drivers, risk vectors, and accelerants

Several dynamics will disproportionately affect near-term outcomes and should be prioritized in board and operating plans for 2026:

- Regulatory and procurement pushes in sterilization and packaging. Governments and large OEMs continue to favor irradiation solutions that can reliably deliver sterility assurance levels or extended shelf life without chemical residues; such mandates accelerate adoption where capital and operating ecosystems are present.

- Supply-chain and localization considerations. The delivery of first-of-country installations and local irradiation centers has material commercial impact: as capacity and local expertise roll out, lead times shrink and procurement risk is reduced, but incumbent suppliers may be challenged.

- Service and digitalization as differentiators. Suppliers that pair hardware with monitoring, predictive maintenance, and production-line integration are capturing higher share of wallet. Recent contracts for line-monitoring solutions illustrate how service-enabled offerings convert into production stability and customer stickiness.

- Trade, certification, and export dynamics. Cross-border deliveries and installations are increasingly shaped by certification regimes and geopolitical factors; companies with global installation experience and compliant supply chains hold a distinct advantage.

Competitive landscape — who matters and why

The E-beam ecosystem is populated by specialized equipment manufacturers, systems integrators, and service-centric providers. Market concentration is moderate: the top three firms account for a meaningful slice of demand while the top five control a clear majority — a dynamic that creates both predictable partner options and tactical openings for challengers (CR3 ≈ 45%, CR5 ≈ 65%). Below we synthesize strategic profiles of the core vendors featured in our coverage and the tactical signals they are sending to the market.

- NHV Corporation (Japan) — NHV’s product portfolio spans low to high energy accelerators and a suite of integrated services. Their recent moves illustrate a shift toward embedded production monitoring and operator support: in March 2026 NHV signed a first-use contract for an EPS monitoring system with a tire manufacturer, reflecting the supplier’s strategy to embed software and services into hardware sales. They also maintain visible presence at trade forums (notably Wire 2026), signaling emphasis on sales-led engineering partnerships.

- CGN Dasheng (China) — A vertically capable designer and installer, CGN Dasheng has been expanding reach into overseas markets. Their delivery of a first electron accelerator into the European Union in October 2025 demonstrates export competence and the operationalization of cross-border installations — a capability that reduces buyer friction in markets prioritizing near-term commissioning.

- Vivarad (France) — A long-established supplier of mid-to-high energy systems with a substantial installed base. Their global installed units and industrial focus make them a natural partner for customers seeking proven industrial solutions rather than custom one-offs.

- Wasik Associates (United States) — Noted for custom, turn-key systems tailored to wire, cable, and medical applications; their strength is in niche configurations and rapid response engineering for specialist applications.

- Mevex (Canada) — Positioned on the higher-power end of the spectrum with capabilities in both electron and X-ray irradiation systems; their technology emphasis aligns with high-throughput sterilization and heavy industrial use cases.

- IBA Industrial (Belgium) — Supplier of Rhodotron® accelerators and a key vendor for industrial sterilization and materials processing. IBA’s publicized contract to install a Be-Efficient irradiation solution in Germany (announced in 2024) showcases the role of large-format, high-throughput systems in national-level capacity projects.

- Energy Sciences Inc. (United States) — A leader in low-voltage E-beam systems for flexible packaging and coatings; their rapid-cure, process-level integration capability positions them well for packaging converters and coatings formulators.

These vendors illustrate a spectrum of go-to-market models: product-centric hardware suppliers, systems integrators that bundle installation and validation, and service-enabled players that monetize uptime and analytics. Competitive advantage is increasingly defined by after-sale services, regulatory know-how, and installed-throughput references rather than unit price alone.

Strategic playbook for 2026 — actionable recommendations

Executives can translate the market outlook into concrete actions. Our top recommendations for 2026 planning are:

- Adopt a phased capital strategy. Use controlled pilots to validate throughput, regulatory acceptance, and product acceptance before committing to full-scale installations. This reduces technical risk and enables contract structures that link final investment to validated outcomes.

- Prioritize suppliers offering integrated monitoring and service ecosystems. Shorter time-to-production and predictable OEE gains frequently offset higher equipment list prices.

- Map regulatory timelines into procurement cadence. For sterilization and food irradiation, certification gating can materially shift project timelines — build compliance milestones into supplier contracts and risk-sharing clauses.

- Evaluate alliance and M&A options for midstream capability. With moderate concentration at the top, acquisitions of smaller integrators or service specialists can accelerate market entry with lower execution risk than greenfield builds.

- Secure supply-chain redundancy for high-value components. Lead times and cross-border logistics remain non-trivial; contracts with multiple qualified vendors for key subsystems reduce schedule risk.

- Invest in in-house commissioning expertise. Firms that develop insourced validation and maintenance capabilities achieve faster ramp-to-rate and command higher margin capture across the life of an installation.

Why PW Consulting’s report matters to 2026 decisions

Decision-makers face a choice: proceed from generic vendor proposals and isolated benchmarks or ground investment and M&A decisions in a cohesive dataset and executable playbook. The full PW Consulting report transforms headline market growth and vendor intelligence into operational plans — detailed TCO calculators, vendor scorecards, and scenario-modeled forecasts tailored to your use cases.

We designed the report to be a working artifact for strategy committees, procurement teams, and R&D portfolio managers. It preserves the granularity required to answer “what-if” questions about energy-class selection, capacity sizing, and partner fit, while shielding the proprietary models and segmentation tables that underpin those recommendations — exactly the level of access your board or investment committee will expect when approving capital deployment or acquisition spend.

To access the full dataset, downloadable models, and vendor scorecards — including the granular segmentation and forecast tables that executive teams use to sign off on capital and partnership strategies — visit the PW Consulting report landing page. The preview above is intentionally high-level: it surfaces the strategic contours, execution levers, and supplier dynamics you need to know now while reserving the actionable segmentation and scenario outputs for the full report.

For boards and executive teams entering 2026 planning cycles, the decisive advantage will come from integrating market forecasts with procurement and validation playbooks — not from raw market numbers alone. PW Consulting’s E Beam Accelerators Market report is built to make that integration immediate and auditable.

For detailed analysis of this topic, please visit the official page: E Beam Accelerators Market

Lacy Lee

Senior Marketing Manager

sales@pmarketresearch.com

00852-95632430

PW Consulting: www.pmarketresearch.com

Tags

PW Consulting

The Best-reviewed Subdivided Market Risk Analysis Firm in the US and East Asia.