PW Consulting: Blue Film Market to Grow at 7.82% CAGR, Rising from USD 970.08 Million in 2025 to USD 1,643.24 Million by 2032 — Asia‑Pacific Leads with USD 614.15M

Blue Film Market 2026: Strategic Imperatives for Semiconductor and Protective-Film Stakeholders

Executive summary

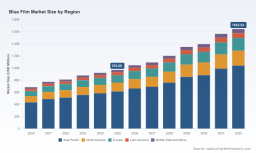

As semiconductor packaging, wafer-level processes, and industrial surface protection intersect with evolving materials economics, the global blue film market is entering a decisive growth phase. Our analysis shows the market expanded from approximately USD 685 million in 2020 to roughly USD 970 million in 2025, and—under the base-case scenario—will grow at a compound annual growth rate (CAGR) of about 7.82% through 2032, reaching an estimated USD 1,643 million. For executives planning capital allocation, sourcing strategies, or M&A activity in 2026, these topline dynamics frame a range of near-term strategic choices: scale selectively, secure feedstock optionality, and align product roadmaps to evolving semiconductor process tolerances.

Why this report matters for 2026 decision-makers

- Actionable foresight: The report translates medium-term demand growth into decision-ready scenarios for purchasing, capacity investment, and partnership timelines—critical for companies that must move from intent to execution in 2026.

- Risk-adjusted sourcing strategies: With polyethylene (PE) and other polymer feedstocks determining cost competitiveness, procurement teams will need scenario playbooks that factor in new supply capacity, price volatility, and regulatory constraints.

- Focused competitor intelligence: A concise, decision-oriented view of incumbent and emerging suppliers enables faster go/no-go determinations for in-licensing, co-development, or procurement trials.

Market trajectory and macro drivers

The blue film market is being pulled by two synchronized forces: semiconductor process intensification and broadened use of polymer films for protective and assembly functions. Between 2020 and 2025 the market has shown steady expansion; our forecast to 2032 reflects a resilient mid-single-digit-to-high single-digit growth profile (7.82% CAGR in the base case). That trajectory is sensitive to three macro drivers:

- Semiconductor demand cycles and the pace of advanced packaging adoption—higher-density packaging and wafer-level assembly increase demand for specialized dicing and back-grinding tapes.

- Upstream polymer markets—PE feedstock availability and price dynamics materially affect unit economics for PE-based blue films.

- Regulatory and quality compliance—environmental and EHS standards shaping material selection and end-market acceptance, including RoHS2-aligned formulations in many semiconductor applications.

Raw materials: a near-term structural inflection

Procurement and product teams must treat polyethylene not as a commodity line item but as a structural variable. Global PE production reached about 123.7 million metric tons in 2025 at an average price near USD 1,125/ton; importantly, new U.S. PE capacity—approximately 2 million t/yr—is scheduled to come online in the second half of 2026. That incremental capacity will shift buyer-supplier dynamics toward more favorable terms for consumers of PE-based films, provided logistics and grade specifications align.

At the same time, volatility in petroleum product prices continues to create supply-cost transmission to film converters. For firms making 2026 capital, product, or contract decisions, the implication is clear: negotiate flexible feedstock agreements, lock-in technical grades early, and model multiple price paths when assessing IRRs on new film lines.

Segment dynamics (what the executive summary omits)

The market is multi-dimensional across region, substrate chemistry, and application. While this release outlines trends and strategic implications, the complete report contains the granular regional and application allocations, price curves, and ASP sensitivity tables that underpin our forecasts. Executives seeking to optimize SKU strategy, channel focus, or plant location for 2026–2028 should review those detailed allocations in the full dossier; public summaries necessarily withhold the precise split data to preserve analytical integrity.

Competitive landscape: leaders, differentiators, and tactical plays

The blue film market exhibits meaningful concentration among established material specialists and chemical manufacturers. Three- and five-firm concentration metrics confirm a market structure where a handful of suppliers capture a dominant share, but the competitive dynamic supports niches for high-performance formulations and service-oriented supply models.

Key players profiled in our report include:

- Mitsui Chemicals Tohcello (Tokyo, Japan): Renowned for high-performance protective films and ICROS™ Tape, the company competes on advanced adhesion science and low-residue peelability—attributes critical to wafer dicing and surface protection. Their R&D cadence and established OEM relationships make them a preferred partner for qualification cycles in wafer fabs.

- Nitto Denko (Osaka, Japan): A leader in semiconductor wafer processing tapes (e.g., SWT series), Nitto combines stable adhesive platforms with robust manufacturing scale. They emphasize process stability and clean-release behavior across backgrinding and dicing operations.

- LINTEC Corporation (Tokyo, Japan): Supplier of non-UV BG tapes and dicing tapes, LINTEC differentiates through high-precision adhesion control and anti-static features—positioning that addresses growing concerns around electrostatic discharge in advanced packaging lines.

- Denka Company Limited (Tokyo, Japan): Focused on semiconductor-grade adhesives and films, Denka is notable for high tensile products and low-residue peelability that facilitate higher throughput in wafer handling.

- Furukawa Electric (Tokyo, Japan): With a materials portfolio that supports polymer films in packaging and protection, Furukawa brings cross-domain polymer know-how—useful for integrated packaging-material solutions.

- Sumitomo Bakelite (Tokyo, Japan): The company contributes to non-UV protective and dicing tape technologies with a focus on materials engineered for process robustness and compatibility with automated assembly lines.

Collectively, these firms combine deep materials IP, channel relationships with semiconductor OEMs and CMs, and robust qualification pipelines. The competitive plays we observe include premiumization of low-residue tapes, bundling of adhesion and anti-static functionalities, and pilot partnerships that accelerate qualification with advanced packaging customers.

Strategic choices for 2026

- For buyers (OEMs and CMs): move to multi-source procurement with technical-qualification hedges. Prioritize suppliers offering co-development pathways and pilot volumes rather than purely price-led bids.

- For film manufacturers: focus on modular capacity expansion and product differentiation via adhesive chemistry and contamination control. Target lead times and service-level guarantees to justify premium pricing.

- For investors and acquirers: prioritize assets with differentiated IP around adhesion and contamination control, and those with strategic customer-supplier contracts that shorten payback periods. Pay special attention to manufacturers positioned to capture the near-term supply benefits from additional PE capacity beginning in late 2026.

Practical contents of the full report

The Blue Film Market: 2026 edition is constructed as a playbook for executives and includes:

- Detailed market sizing and forecast models (2020–2032) with scenario analysis and sensitivity tables.

- Segmentation matrices by region, polymer type, and application—complete with ASP trends and adoption curves.

- Feedstock and input-cost modeling, including PE supply scenarios and price-path simulations to 2030.

- Supplier scorecards and capabilities mapping for major manufacturers, plus supplier selection templates.

- Go-to-market and commercialization checklists for new film grades and adhesive systems.

- M&A screening criteria and valuation primers tailored to the blue film value chain.

Note: this public summary intentionally omits the granular region/application breakdowns and the underlying model spreadsheets. Those proprietary datasets are included in the full report and are essential for operationalizing the recommendations above.

Practical next steps

- Procurement: request the supplier scorecards and sample qualification timelines to begin staggered trials in Q1–Q2 2026.

- R&D/Product: prioritize formulations that minimize particulate and residue under wafer-level process conditions; accelerate pilot lines for grades compatible with RoHS2 requirements.

- Corporate Development: use the report’s valuation filters to shortlist acquisition or minority-investment targets that alleviate feedstock exposure or add differentiated polymer IP.

About PW Consulting’s methodology

Our forecast synthesizes bottom-up shipment forecasts, primary interviews across fabs and converters, and an inputs-driven cost model that links polymer markets to film ASPs. We stress-tested the base-case 7.82% CAGR against two alternative scenarios—downside (demand-softening and protracted PE price inflation) and upside (accelerated advanced-packaging adoption and favorable feedstock pricing)—and produced valuation and supply-risk outputs for each.

How to access the full intelligence

This briefing is designed as a tactical preview. The full Blue Film Market report contains the complete datasets, model files, supplier scorecards, and the confidential regional/application splits required for execution. To purchase the report or to schedule a briefing with our lead analyst team, please visit PW Consulting’s Blue Film Market page or contact our sales desk for an executive briefing. Detailed modeling templates and supplier negotiation playbooks are available to corporate subscribers and advisory clients.

Closing perspective

2026 is a pivot year for stakeholders in the blue film ecosystem. New feedstock capacity, continued demand from semiconductor advanced packaging, and incremental regulatory pressures will create both margin pressure and opportunities for premium product adoption. Firms that translate the macro signals into concrete sourcing, product, and partnership moves in 2026 will capture outsized returns as the market scales toward the early-2030s. PW Consulting’s Blue Film Market report is structured to convert those signals into executable plans—bridging strategy and operations at the pace that today’s supply chains demand.

For detailed analysis of this topic, please visit the official page: Blue Film Market

Lacy Lee

Senior Marketing Manager

sales@pmarketresearch.com

00852-95632430

PW Consulting: www.pmarketresearch.com

Tags

PW Consulting

The Best-reviewed Subdivided Market Risk Analysis Firm in the US and East Asia.