PW Consulting Forecasts Three-Dimensional Topological Insulator Market to Surge at a 22.46% CAGR

Three Dimensional Topological Insulator Market: Strategic Imperatives for 2026

As organizations plan capital allocation and technology roadmaps for 2026, PW Consulting’s latest Three Dimensional Topological Insulator Market report delivers a decision-grade, actionable view of an industry transitioning from academic curiosity to nascent commercial adoption. This executive briefing outlines the report’s strategic value to corporate leaders, R&D heads, supply-chain managers and investors — offering a high-level tour of the evidence and recommendations without disclosing the detailed subsegment tables and proprietary forecasts preserved for subscribers.

Three Dimensional Topological Insulator Market

Why 2026 is a Pivot Year

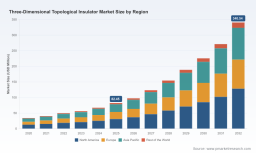

Three dimensional (3D) topological insulators are moving into a phase where materials availability, deposition technology, and device integration converge to create commercially relevant product pathways. Our model — anchored on a 2025 base year — estimates the total market at approximately USD 82.45 Million in 2025, increasing to roughly USD 97.51 Million in 2026 and growing to an estimated USD 340.54 Million by 2032 under the central scenario. The forecast period spanning 2026–2032 assumes a compound annual growth rate (CAGR) of 22.46%.

Three Dimensional Topological Insulator Market

These headline figures are not academic projections: they reflect measurable adoption signals in quantum computing research programs, spintronic demonstrators, advanced optoelectronic prototyping and continuity with thermoelectric supply chains. For executives considering near-term bets, 2026 represents the first practical inflection point where procurement commitments, supply-chain resilience and early commercial partnerships can materially affect market positioning through 2030.

Three Dimensional Topological Insulator Market

What the Full Report Contains (Practical, Executable Insights)

- Validated market-sizing and scenario frameworks from 2020–2032, including base-year benchmarking and sensitivity analyses to raw-material and regulatory shocks.

- Demand drivers and technology adoption curves broken down by device pathway, maturity stage and adoption risk — designed to support go/no-go decisions in 2026.

- Supply-chain diagnostics highlighting critical input exposures (including chalcogenides and tellurium sourcing), supplier concentration, and second-/third-tier risk maps.

- Commercialization playbooks for materials suppliers, device OEMs and system integrators: partner archetypes, licensing strategies, and suggested investment timelines tailored to company size and risk appetite.

- Regulatory and trade-impact scenarios, with mitigation options for export-control and raw-material volatility that could affect 12–24 month project deliveries.

- Deal-level advisory (M&A and JV scouting), including a short-list of acquisition archetypes, due-diligence checklists and integration considerations for technology-led roll-ups.

To respect competitive sensitivities and the “trailer” principle of this release, granular segment-by-segment revenue tables and regionally disaggregated share data are accessible only in the full report.

Supply-Chain and Raw Material Dynamics: The Immediate Risk Layer

Our analysis identifies raw-material dynamics as the dominant near-term risk to adoption velocity. Tellurium — a key chalcogenide component in several prototypical 3D topological insulator chemistries — experienced acute price and availability pressure in 2024–2025. Independent commodity monitoring and public-source reporting indicate sharp year-over-year price escalations and export-control frictions, which have created tangible procurement lead-time extensions and cost pass-through risks.

Notably, regulatory measures in key producing jurisdictions have lengthened export licensing cycles and introduced end-user verification requirements that can add weeks to procurement timelines. For firms executing device validation programs in 2026, this means procurement strategy must shift from just-in-time to resilient-sourcing models. Practical responses include forward-buy contracts, qualification of alternative chemistries, supplier partnerships for guaranteed allocations, and investment in recycling/recovery streams.

Competitive Landscape: Who Matters and Why

The supplier ecosystem is populated by specialized crystal growers, materials distributors and thin-film equipment vendors. Market concentration is meaningful: our top-line concentration metrics show that the top three suppliers control a substantive portion of the market, while the top five widen that control further — underscoring a market where early commercial relationships and long-standing materials expertise matter.

Key players profiled in the report and their strategic positions include:

- HQ Graphene (Groningen, Netherlands; https://www.hqgraphene.com) — Distinguished by high-quality single-crystal offerings of prototypical 3D topological insulators. Their quality focus positions them as a preferred supplier for research institutions and device labs aiming for reproducible experiments.

- American Elements (Los Angeles, California, USA; https://www.americanelements.com) — A volume-oriented materials supplier providing high-purity powders, crystals and sputtering targets; attractive for firms seeking standardized forms for scale-up and manufacturing trials.

- Stanford Advanced Materials (SAM) (Lake Forest, California, USA; https://www.samaterials.com) — Provides chemical vapor deposition (CVD) films and tailored crystal compositions, enabling device developers focused on thin-film integration and process compatibility.

- Kurt J. Lesker Company (KJLC) (Jefferson Hills, Pennsylvania, USA; https://www.lesker.com) — Supplies high-purity sputtering targets and evaporation materials. Their strength is in deposition consumables and process-consistent materials for thin-film device makers.

- MSE Supplies LLC (Tucson, Arizona, USA; https://www.msesupplies.com) — Acts as a distributor and channel consolidator for research and early industrial users, smoothing access to harder-to-source crystals and films.

- 2D Semiconductors (Nuevogen LLC) (Phoenix, Arizona, USA; https://2dsemiconductors.com) — Focuses on high-quality single crystals and layered chalcogenides with guaranteed topological properties, increasingly relevant to device integrators demanding reproducible material characteristics.

These suppliers play different roles in the early value chain: some are quality-centric crystal houses favored by research labs, others provide industrial-grade targets and targets for deposition, and a few act as critical channel partners who can bridge R&D needs with pilot-scale production. For 2026 planning, the strategic question is not merely “who supplies” but “who can commit to multi-year capacity and validation support.”

Strategic Implications and Recommended Actions for 2026

PW Consulting recommends a three-track approach for firms building a 2026 plan around 3D topological insulators:

- De-risk Procurement and Qualification

- Map true bill-of-materials exposure at the device and module level; identify single-source chokepoints and quantify lead-time elasticity.

- Establish multi-sourcing for critical chalcogenides and negotiate allocation guarantees where possible.

- Accelerate qualification of alternative chemistries and recycled feedstocks to insulate production from short-term supply shocks.

- Align Technical Roadmaps with Commercial KPIs

- Translate materials performance metrics into device-level KPIs (e.g., coherence improvements, spin-relaxation benchmarks, thermal conversion improvements) that justify near-term procurement and capital decisions.

- Prioritize process steps that reduce materials intensity or allow substitution without degrading device performance.

- Execute Partner-Led Scale-Up and M&A Playbooks

- Identify upstream partnerships (crystal growers, target manufacturers) that offer co-investment in capacity tied to off-take agreements.

- For larger OEMs, consider targeted acquisitions of specialty-material houses to secure supply and capture margin in a concentrated upstream market.

Decision Triggers and KPIs for 2026

To operationalize the above, senior leaders should adopt a concise set of decision triggers for 2026:

- Procurement continuity: execute minimum 12–18 month allocation commitments if supplier lead times exceed critical thresholds for device launches.

- Technology validation: proceed to pilot-line investment only when reproducible device-level metrics meet predefined performance and yield thresholds over successive lots.

- Financial viability: require project IRR and payback windows to account for plausible raw-material price shocks and supply interruptions in scenario stress tests.

Regulatory and Geopolitical Considerations

Trade and export controls have emerged as non-linear risks. Recent public reporting documents extended export licensing timelines and heightened end-user scrutiny in key supply countries, adding weeks to procurement cycles and complicating just-in-time sourcing. Companies preparing 2026 budgets must factor these administrative frictions into both lead-time assumptions and contingency inventory policies.

How PW Consulting’s Report Helps You Act

The full Three Dimensional Topological Insulator Market report translates the market’s headline growth trajectory into operational choices. Subscribers will receive:

- Detailed, drillable market models (including sensitivity pivots) that support capital allocation decisions.

- Supplier scorecards and a prioritized watchlist of potential acquisition or partner candidates.

- Negotiation playbooks for long-lead materials and practical checklists for qualifying alternative chemistries.

- Regulatory-monitoring templates and a decision-tree for export-control scenarios that can be embedded into procurement and legal workflows.

Concluding Perspective

The 3D topological insulator ecosystem is entering a commercially meaningful growth phase: the market baseline of roughly USD 82.45 Million in 2025, moving past USD 97.51 Million in 2026, and tracking to several-fold expansion by 2032, underscores the opportunity. But opportunity without operational readiness invites execution risk. The combination of concentrated upstream supply, raw-material price and regulatory volatility, and nascent device integration pathways means that strategic foresight — not merely technical optimism — will determine market winners.

For decision-makers planning 2026 commitments, PW Consulting’s report is structured to convert market intelligence into executable actions: procurement contracts, partner selection, manufacturing investments, and scenario-tested financial models. To access the full dataset, segment-level analysis and supplier scorecards that inform the tactical next steps, please consult the full report available from PW Consulting.

For detailed analysis of this topic, please visit the official page: Three Dimensional Topological Insulator Market

Lacy Lee

Senior Marketing Manager

sales@pmarketresearch.com

00852-95632430

PW Consulting: www.pmarketresearch.com

Tags

PW Consulting

The Best-reviewed Subdivided Market Risk Analysis Firm in the US and East Asia.