PW Consulting Forecast: Microtubule Inhibitor Drugs Market to Expand at a 5.5% CAGR During 2026–2032

Microtubule Inhibitor Drugs Market — 2026 Strategic Preview: PW Consulting Report Highlights

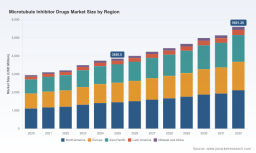

PW Consulting’s latest market study on Microtubule Inhibitor Drugs provides a focused strategic playbook for life-sciences executives planning decisions in 2026. The market has expanded steadily in the early 2020s — growing from roughly USD 2.95 billion in 2020 to about USD 3.85 billion in 2025 — and is projected to continue expanding at a compound annual growth rate of 5.5% through our 2026–2032 forecast horizon, reaching approximately USD 5.60 billion by 2032. This growth is not uniform: it is being reshaped by novel clinical approvals, evolving ADC payload strategies, and shifting reimbursement dynamics. Our report synthesizes these forces into actionable intelligence designed to shorten decision cycles and improve investment outcomes.

Microtubule Inhibitor Drugs Market

Why this report matters for 2026 decision-makers

-

Speed of choice: executives face trade-offs between advancing proprietary microtubule chemotypes, licensing ADC payloads, or reallocating capital to other oncology classes. The report models the commercial and development trade-offs across those pathways so you can rank opportunities by risk-adjusted ROI.

Microtubule Inhibitor Drugs Market -

Regulatory and payer inflection points: recent accelerated approvals for microtubule-inhibitor ADCs have altered the evidence and access bar. Our work translates regulatory precedent into market-access scenarios and pricing sensitivity analyses.

Microtubule Inhibitor Drugs Market -

Competitive intensity and consolidation signals: concentration metrics show the market is neither a pure commodity nor a closed oligopoly — with the top three firms holding meaningful but not dominant share and the top five consolidating a larger majority. That structure opens distinct windows for specialized entrants, licensing plays, and M&A arbitrage.

What’s inside the PW Consulting deliverable (select highlights)

-

Integrated financial models: top-down and bottom-up forecasting engines calibrated to 2020–2025 historicals and flexible across three commercialization scenarios (base, accelerated uptake, constrained access). Models are packaged in editable spreadsheets so teams can run sensitivity checks on timelines, pricing, and market-access outcomes.

-

Actionable go-to-market playbooks: indication sequencing, channel strategy, and launch planning templates tailored for branded agents, generics, and ADC payload partnerships.

-

Clinical and pipeline mapping: therapy-class heatmaps linking ongoing trials, mechanism-of-action differentiation, and likelihood-of-approval scoring to expected commercial value.

-

Regulatory and HTA frameworks: jurisdiction-specific dossiers and evidence-roadmap templates reflecting recent approvals and accelerated pathways relevant to microtubule strategies.

-

Partnering & M&A playbook: valuation templates, term-sheet checklists, and a prioritized list of target capabilities (manufacturing scale, payload chemistry, linker technology) most likely to move the needle on deal value.

-

Risk/opportunity matrix: a prioritized catalog of disruptive threats (resistance mechanisms, competing mechanisms, reimbursement pushback) and opportunity accelerants (ADC payload optimization, combination regimens, biomarker stratification).

Market dynamics and recent inflection events

The microtubule inhibitor class is being reshaped on two fronts: therapeutic modality convergence and regulatory precedent. Antibody–drug conjugates (ADCs) that deploy microtubule inhibitor payloads have translated established cytotoxic mechanisms into targeted delivery strategies, improving therapeutic windows and opening new indications. In 2025, regulators granted accelerated approval to a c‑Met-directed microtubule inhibitor ADC for NSCLC, and later in the year an ADC with a microtubule payload received approval for relapsed multiple myeloma. These approvals are meaningful beyond the labeled indications — they set evidentiary expectations for toxicology, manufacturing controls, and post-approval confirmatory studies that will influence investment timelines across the sector.

Commercial dynamics are equally consequential. ADCs with well-established microtubule payload chemistries continue to command solid positioning across a range of oncology indications. Payers are still refining value frameworks for these hybrids: reimbursement is often conditional on demonstrated survival benefit or on managed-entry agreements. Our report models the likely payer responses in major markets and outlines contract structures that preserve revenue while accelerating patient access.

Competitive landscape — who’s shaping strategy

-

Pfizer Inc. — A long-tenured player in microtubule therapeutics through brand and generic paclitaxel offerings. The company leverages scale in manufacturing and a broad oncology commercial footprint to defend established indications and to explore lifecycle opportunities.

-

Sanofi S.A. — A specialist approach with cabazitaxel in castration‑resistant prostate cancer highlights playbooks for targeted lifecycle management and indication-focused positioning.

-

Bristol‑Myers Squibb — Active in microtubule-related domains through both marketed agents and ADC payload development; their dual pathway of product commercialization plus ADC R&D demonstrates a hedge strategy that many mid-sized innovators emulate.

-

Eisai Co., Ltd. — Non-taxane microtubule-modifier positioning shows how niche chemotypes can sustain relevance in specialty oncology segments and later be repurposed for orphan indications.

-

Eli Lilly and Company — Uses broad oncology R&D capacity to selectively fund microtubule-related programs, illustrating how platform diversification changes competitive calculus.

-

AbbVie Inc. — Recent accelerated approval of a c‑Met-directed microtubule inhibitor ADC demonstrates how focused ADC strategies can rapidly translate into clinical and commercial momentum when backed by robust biomarker selection and clinical execution.

Collectively, these players illustrate three viable strategic postures for 2026: defend incumbent indications and efficiencies; specialize in differentiated chemistries and narrow indications; or converge around ADC payload and linker partnerships to access higher-margin, targeted opportunities. Our report profiles likely tactical moves for each posture and provides checklists to evaluate competitor responses.

Strategic actions recommended for 2026

Executives reading this preview should translate insight into five near-term priorities:

-

Reassess portfolio allocation against ADC timelines. Prioritize assets that can be paired with proven payload/linker platforms or that address high-unmet-need pockets where payers will accept higher cost-per-QALY thresholds.

-

Fast-track evidence-generation strategies that align with accelerated approval precedents: design confirmatory trials and real-world evidence plans in tandem with early regulatory engagement to secure managed-access pathways.

-

Pursue targeted partnerships for payload access rather than attempting in-house chemistry rebuilds unless a clear, proprietary advantage exists. Our valuation models show partnering reduces time-to-market and capital intensity in most base cases.

-

Build payer engagement playbooks before launch. Use adaptive contracting, outcomes-based agreements, and indication-based pricing pilots to mitigate access risk.

-

Prepare manufacturing scale and CMC contingencies for ADCs. Supply-chain and CMC readiness remain common failure modes for rapid launches; preemptive capacity commitments are a competitive differentiator.

How PW Consulting accelerates executive decisions

The report is structured to be both a diagnostic and a working tool. It does not simply describe market movements — it equips teams with models, templates, and prioritization rubrics that can be executed in 60–90 day sprints. Examples of tangible outputs clients receive include editable go/no-go scorecards for licensing discussions, launch-cost roll-ups by indication, and a deal-term comparator for ADC payload transactions.

In keeping with a “trailer” approach, this press briefing highlights report insights and strategic implications while intentionally withholding the granular regional and application split tables, as well as certain segment-level revenue breakouts. These granular datasets are part of the full report package and are available through our official distribution channels for clients seeking to run proprietary scenarios and to extract market-entry playbooks customized to company-specific constraints.

Immediate next steps for leaders

-

Request the full PW Consulting Microtubule Inhibitor Drugs Market report to access the scenario-models, segment-level forecasts, and the proprietary competitor scoring matrix used to generate our recommendations.

-

Use the included workshop agenda to convene R&D, commercial, and M&A leaders; run a 2‑day prioritization lab to translate insights into a 12‑month roadmap.

-

Engage our advisory team for a tailored deep-dive: we can run company- or asset-specific valuation stress tests and co-develop a launch or partnering strategy that aligns with your balance sheet and risk tolerance.

Microtubule inhibitor therapeutics remain a foundational oncology class, now entering a new phase driven by conjugation technologies and tighter payer scrutiny. For decision-makers planning 2026 actions, the right combination of evidence strategy, partnership choice, and commercial preparedness will determine who captures the next generation of value. PW Consulting’s report provides the empirical backbone and practical toolset to make those choices with confidence.

For detailed analysis of this topic, please visit the official page: Microtubule Inhibitor Drugs Market

Lacy Lee

Senior Marketing Manager

sales@pmarketresearch.com

00852-95632430

PW Consulting: www.pmarketresearch.com

Tags

PW Consulting

The Best-reviewed Subdivided Market Risk Analysis Firm in the US and East Asia.