PW Consulting: Open Circuit Combustible Gas Detector Market to Expand at 6.85% CAGR During 2026–2032, Says New Report

Open Circuit Combustible Gas Detector Market: Strategic Preview for 2026 Decisions

As PW Consulting’s Senior Strategic Advisor and Chief Industry Analyst, I am pleased to introduce a focused executive preview of our newly released Open Circuit Combustible Gas Detector Market research. Designed as a high-impact decision support tool for senior leaders planning 2026 investments, this briefing highlights the strategic implications of our findings while intentionally withholding the granular segmentation tables and proprietary models that are reserved for the full report.

Open Circuit Combustible Gas Detector Market

Why this market matters in 2026

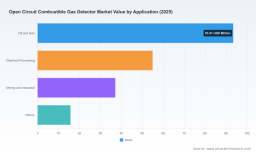

Open circuit combustible gas detection remains a critical safety and operational-control technology across energy, chemical, mining and industrial process industries. After a period of steady expansion through 2020–2025, the market reached an estimated USD 201.25 Million in 2025. Our forecast models — built on primary interviews, field validation and financial triangulation — project a compound annual growth rate (CAGR) of 6.85% across the 2026–2032 horizon, with continued tailwinds from stricter safety standards, renewed capex in hydrocarbon value chains, and adoption of next-generation sensing modalities.

Open Circuit Combustible Gas Detector Market

For executives mapping strategy in 2026, this creates a window to prioritize product investments, channel restructuring, and M&A activity informed by predictable growth and identifiable pockets of technological disruption. The remainder of this briefing translates our quantitative findings into practical imperatives.

Open Circuit Combustible Gas Detector Market

What the report delivers — practical, decision-ready content

PW Consulting’s full report synthesizes quantitative forecasting with tactical playbooks. Highlights include:

- Market sizing and trajectory: validated historical base (2020–2025), a 2025 base year snapshot, and scenario-based forecasts through 2032.

- Technology and product roadmaps: comparative analysis of infrared open-path, catalytic/heat-sensing open-circuit approaches and emerging laser-based detection systems, with practical adoption timelines and recommended R&D focus areas.

- Regulatory and compliance mapping: a compliance matrix referencing relevant industry standards (e.g., ANSI/ISA-92.00.04 and FM approvals) and their operational implications for product certification and field deployment.

- Procurement and total cost of ownership (TCO) models: capital, maintenance, calibration and lifecycle replacement pathways tailored to site types and risk profiles.

- Supply-chain and raw materials risk assessment: impact scenarios for inflationary pressure on sensor components, supplier concentration, and mitigation strategies including dual-sourcing and component re-specification.

- Go-to-market playbooks: channel optimization, OEM partnerships, and service-led differentiation strategies to expand share in industrial accounts.

- Competitive intelligence and M&A heatmap: strategic options for incumbents and new entrants, including bolt-on acquisition targets and capability gaps likely to shape consolidation.

Market structure and concentration — what leaders need to know

The sector’s competitive structure is characterized by a moderate level of concentration. The top three suppliers account for a sizable portion of the market, and the top five together approach a majority share. This dynamic creates a dual landscape: established vendors enjoy scale and installed-base advantages, while mid-tier and specialist vendors can win by focusing on product differentiation (e.g., false-alarm rejection, laser-based sensitivity, or integration into IIoT ecosystems).

For 2026 strategy, this implies a two-track approach: incumbents should defend and extend their service ecosystems and certification footprints, while challengers should target niche technical advantages and white-space verticals where rapid penetration is feasible.

Competitive landscape — profiles and strategic implications

-

Emerson (Rosemount / Spectrex) — A clear leader with established open-path infrared offerings designed for harsh hydrocarbon environments. Strategic imperative: continue leveraging brand strength and global service networks while accelerating integration of analytics and remote diagnostics to protect installed base and lock-in service revenue.

-

MSA Safety — Combines mature IR solutions with laser-based innovation and advanced false-alarm rejection. Strategic imperative: capitalize on connectivity and integrated safety systems to cross-sell to customers modernizing plant safety architectures.

-

Teledyne Gas & Flame Detection — Actively previewing next-generation detectors and laser-based H2S solutions. Strategic imperative: product pre-launches present opportunities to capture project-specification cycles; rapid field pilots and third-party validations will be decisive.

-

GDS Corp — A distributor and systems integrator focused on industrial deployments and aftermarket services. Strategic imperative: strengthen engineering services and bundled maintenance contracts to convert installation projects into recurring revenue streams.

-

Det-Tronics (UTC group) — Known for robust infrared open-path systems tailored to continuous monitoring. Strategic imperative: optimize cost structures and certification roadmaps to compete for large, safety-critical EPC and operator contracts.

Across vendors, our qualitative benchmarking highlights three differentiators that materially affect win rates: detection sensitivity and stability in adverse conditions, false-alarm mitigation through signal processing, and ease of integration into plant safety and asset management systems. Firms that bundle these capabilities with strong field service propositions will outcompete on lifecycle economics rather than headline unit price.

Regulatory and raw-material headwinds

Regulation remains a decisive driver of procurement cycles. Performance and certification expectations embedded in standards such as ANSI/ISA-92.00.04 and FM approvals are shaping specification documents for new-builds and major turnarounds. Compliance timelines should be treated as near-term catalysts for demand.

At the same time, rising raw material costs and inflationary pressures are constraining manufacturers’ gross margins. The report quantifies supplier-level cost sensitivity and offers mitigation tactics — from alternative materials and revised BOMs to hedging strategies and revised maintenance contracts that pass a portion of cost volatility to customers while preserving competitiveness.

Technology inflection points and adoption scenarios

Two technology themes will shape 2026+ product roadmaps:

- Laser-based detection: promises higher selectivity and longer ranges for specific target gases — attractive for specialized applications (e.g., H2S, hydrogen monitoring) but requiring rigorous field validation and new certification paths.

- Connected, analytics-enabled detection: integrating detectors into IIoT platforms for predictive maintenance and alarm prioritization reduces nuisance trips and supports operational efficiency claims that justify premium pricing.

Our scenario analysis outlines thresholds for adoption: vendors should prioritize pilot deployments where incremental safety or uptime value can be quantified and where regulatory compliance accelerates acceptance.

Actionable recommendations for 2026 planning

For leaders deciding on capital allocation and strategic moves in 2026, PW Consulting recommends the following prioritized actions:

- Reassess product roadmaps to align with laser and analytics adoption timelines — accelerate pilots now to be specification-ready when procurement windows open.

- Lock in service and certification capabilities — expand regional service coverage or partner with local integrators to reduce time-to-deploy for large operators.

- Hedge supply risks — identify single-source components and execute dual-sourcing or longer-term supply agreements to stabilize margins.

- Refine pricing to capture TCO value — transition from unit-focused pricing to outcome-based contracts bundled with calibration and analytics services.

- Target M&A selectively — prioritize targets that add complementary sensing technology, software analytics, or strong regional aftermarket presence.

What we intentionally withhold here — and why

This briefing is designed as a strategic “trailer”: it demonstrates the depth and applicability of our analysis to support 2026 decisions but intentionally omits the granular regional, application and type-level splits that underpin our full-model outputs. Those detailed matrices, supplier benchmarking scorecards, and downloadable Excel models are available only in the licensed report and online dashboards.

If you are preparing a capital plan, vendor RFP, or product roadmap for 2026, accessing the full data tables and scenario models will materially shorten decision cycles and reduce execution risk. The full report contains the segmented demand curves, use-case level TCO calculators, and step-by-step playbooks required to operationalize the strategic recommendations outlined above.

How to use this intelligence in board and investment forums

Present this briefing to your board or investment committee as an actionable risk/opportunity brief: anchor projections to the 2025 base, explain the 6.85% CAGR underpinning medium-term upside, and propose a 90–180 day plan for pilots, supplier negotiations, and potential bolt-on acquisitions. Use the full report to populate budget worksheets, RFP language, and integration checklists that will be needed for procurement and M&A execution.

Next steps

PW Consulting is available to brief executive teams, lead focused workshops, and provide bespoke modules of the full report tailored to procurement, engineering, or M&A agendas. For fast-moving programs, our analysts can deliver an accelerated briefing package that includes redacted but actionable decision matrices designed for secure boardroom use.

To request the full licensed report, the interactive data dashboards, or a customized executive briefing, please visit the PW Consulting report page or contact our client services team. The full dataset contains the region-, type- and application-level detail, supplier scorecards and downloadable financial models that underpin the strategic recommendations summarized here.

— PW Consulting, Advanced Industries Practice

For detailed analysis of this topic, please visit the official page: Open Circuit Combustible Gas Detector Market

Lacy Lee

Senior Marketing Manager

sales@pmarketresearch.com

00852-95632430

PW Consulting: www.pmarketresearch.com

Tags

PW Consulting

The Best-reviewed Subdivided Market Risk Analysis Firm in the US and East Asia.