PW Consulting Forecast: Waist‑Level Viewfinder Market to Expand at a Modest 1.45% CAGR Through 2032

Waist-Level Viewfinder Market 2026: Strategic Preview from PW Consulting

As demand patterns for tactile, analog-inspired shooting experiences persist alongside the growth of mirrorless systems, the waist-level viewfinder (WLV) market occupies a unique niche at the intersection of professional medium-format heritage and consumer-driven accessory innovation. PW Consulting’s latest Waist-Level Viewfinder Market report (base year: 2025; historical coverage: 2020–2025; forecast: 2026–2032) delivers an action-oriented evidence base designed to inform strategic choices for 2026 planning cycles—whether you are an OEM, accessory specialist, private-equity investor, or retailer seeking differentiated growth pathways.

Waist Level Viewfinder Market

Why this market matters in 2026

-

Convergence of vintage ergonomics and modern imaging: Manufacturers are reintroducing waist-level mechanics—either integrated or as modular accessories—creating a revived product category that resonates with professionals and enthusiasts seeking deliberate, slower capture experiences.

Waist Level Viewfinder Market -

Accessory-driven volume growth: The accessory ecosystem is expanding rapidly, enabling lower-cost entry points for mirrorless adopters while preserving the premium segment dominated by legacy medium-format players.

Waist Level Viewfinder Market -

Consolidation and concentration: Market concentration is meaningful—our research identifies a high three- and five-company concentration ratio, highlighting a landscape where a small set of global players capture a large share of revenue and influence standards, distribution, and aftermarket activity.

High-level market trajectory (macro snapshot)

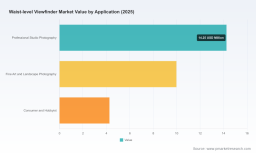

PW Consulting’s top-line market model estimates the global Waist-Level Viewfinder market at USD 28.5 Million in the base year 2025. The market demonstrates steady expansion under a tempered growth regime: the model projects a compound annual growth rate (CAGR) of approximately 1.45% over the forecast period 2026–2032, taking the market toward roughly USD 31.5 Million by 2032. Historical trend lines from 2020 through 2025 inform our scenario baselines and stress-test assumptions for supply-chain shocks, consumer sentiment shifts, and upstream component pricing.

Dynamics shaping supply and demand

-

Product innovation and retro revival: Industry events and prototype demonstrations in early 2026 underscore a deliberate push to reintroduce waist-level optical experiences into digital bodies. These moves are both product- and narrative-driven: brands are leveraging tactile, mirror-based viewing designers’ appeal to differentiate in a crowded mirrorless market.

-

Accessory ecosystem growth: A vibrant third-party supplier base has emerged, producing compact, universal WLV accessories compatible with modern camera mounts. This accessory segment acts as both a gateway for new users and a margin-rich channel for specialist manufacturers, altering traditional OEM-only value chains.

-

Channel innovation and aftermarket dynamics: The used-market and aftermarket support for legacy medium-format systems continue to sustain demand for interchangeable waist-level finders, while e-commerce and specialist retailers extend reach for boutique and mass-market WLV accessories.

-

Concentration and competitive pressure: With the largest players holding a significant share of the market—evidenced by elevated CR3 and CR5 metrics—new entrants must either target niche, cost-sensitive subsegments or pursue rapid differentiation via features, co-branding, or distribution partnerships.

Competitive landscape — who to watch

The WLV arena blends legacy, premium OEMs with nimble accessory manufacturers. Our qualitative and quantitative analysis profiles the competitive set to clarify where competitive pressure is highest and where white space remains.

-

Hasselblad (Gothenburg, Sweden) — The archetypal medium-format incumbent continues to anchor the high-end segment, offering waist-level finding systems as standard or optional elements for established V- and H-series platforms. Hasselblad’s brand equity and professional channel relationships keep it central to any premium-focused strategy.

-

Ulanzi (China) — A leading accessory innovator in the mirrorless value chain. Ulanzi’s product orientation targets universal compatibility, rapid iteration, and aggressive go-to-market tactics that broaden WLV adoption beyond traditional medium-format users into mainstream mirrorless communities.

-

CHI / Chinotechs (China) — Focused on retro-styled WLV optics, CHI’s metal-bodied designs appeal to enthusiasts and boutique retailers. Recent product launches reflect an emphasis on build quality and authentic viewing experiences, a strategic contrast to low-cost disposable accessories.

-

Reflx Lab (China) — Represents the compact universal accessory trend, concentrating on compatibility and portability for hybrid shooters who prize modularity in both digital and film workflows.

-

Mamiya (Japan, legacy presence) — While Mamiya’s core camera business is historical, its ecosystem and aftermarket support continue to underpin demand for interchangeable waist-level solutions in the used and rental markets.

-

Canon (Tokyo, Japan) — Recent prototype demonstrations at early-2026 trade events signal a strategic exploration of retro-inspired, waist-level optical systems within digital camera designs. Canon’s move is particularly consequential because it could validate the category at scale and reshape OEM investment calculus.

Recent product and market movements

-

Prototype demonstrations by a major OEM at a flagship trade show in early 2026 have re-ignited conversation about integrating waist-level optical viewing into modern digital bodies—an important validation signal for suppliers and investors.

-

Late-2025 and early-2026 product introductions from accessory specialists emphasize higher build quality, configurable framelines, and universal mounting approaches—factors that are expanding the total addressable market by lowering adoption friction for mirrorless users.

-

On the retail and distribution side, an increasing number of specialist channels are bundling WLVs with learning content and workshop experiences—an important demand-generation tactic that elevates product desirability beyond pure function.

What PW Consulting’s report delivers — practical content for decision makers

The report is crafted as an operator’s playbook for 2026 strategic choices. Core deliverables include:

-

Proprietary top-line model: annualized market sizing from historical years through the 2026–2032 forecast, with scenario toggles for low/central/high demand and supply constraints.

-

Concentration & competitive heatmaps: an independent assessment of market share distribution, pricing pressure points, and segment-level profitability (note: detailed segment tables and company-level revenue splits are available in the full report).

-

Supplier & product scorecards: capability matrices for OEMs and third-party accessory manufacturers covering engineering depth, manufacturing flexibility, go-to-market capabilities, and aftermarket/recommerce strength.

-

Go-to-market playbooks: tailored strategies for premium OEMs, accessory brands, and retailers—spanning direct-to-consumer models, channel partnerships, co-branded collaborations, and experiential marketing to capture latent demand.

-

M&A and partnership roadmap: prioritized target archetypes, valuation primers, and integration risk checklists to support inorganic growth or bolt-on plays for scale-oriented players.

-

Risk framework and sensitivity model: a calibrated stress test for component cost inflation, manufacturing lead-time disruptions, and shifts in consumer sentiment toward analog-style capture.

Strategic implications for 2026 decision cycles

-

For premium OEMs: Treat waist-level viewing as a strategic product platform rather than a niche accessory. Consider modular options (interchangeable finders) to monetize both new-body sales and aftermarket upgrades, while protecting margins through branded, service-backed offerings.

-

For accessory manufacturers: Prioritize durability, compatibility, and distribution partnerships. The most successful accessory players will combine engineering credibility with community-driven marketing and retail visibility.

-

For retailers and channels: Curate experiential retail programs that position waist-level viewing as a creative tool—workshops, rental partnerships, and bundled offerings will accelerate conversion and justify premium ASPs.

-

For investors: Focus on consolidation plays that address distribution and margin expansion. Given the market’s concentrated nature, mid-market acquisition targets that enhance channel reach or proprietary hardware capabilities can yield outsized returns.

How to use the report in your 2026 planning

-

Use the scenario model to stress-test inventory and capex decisions against asymmetric demand paths and component availability.

-

Leverage the supplier scorecards to build preferred vendor lists and to negotiate volume-based pricing tied to multi-year commitments.

-

Apply the go-to-market playbooks to prioritize pilot markets, define merchandising bundles, and structure co-marketing agreements with complementary brands.

Data integrity and methodology

Our market sizing combines primary interviews with manufacturers, distributors, and specialist retailers, triangulated with secondary sources and transactional data. Forecasts are produced using a combination of time-series extrapolation for macro baseline trends plus bottom-up product adoption models for accessory migration, calibrated against observed launch cadence and trade-show signals in 2025–2026.

A final note — the trailer approach

This briefing is intentionally targeted: it exposes the macro dynamics, the high-level numbers, and the actionable strategic pathways that matter for 2026 decisions while preserving the detailed segment-level tables, regional splits, and granular company revenue models for the full report. PW Consulting’s detailed tables contain the exact segment breakouts, regional and application-specific forecasts, price/volume elasticity matrices, and downloadable models you will need to execute operational and M&A moves.

To access the complete dataset, scenario files, and supplier scorecards that underpin these conclusions, please visit the official report page where the full intelligence package and purchase options are available.

For detailed analysis of this topic, please visit the official page: Waist Level Viewfinder Market

Lacy Lee

Senior Marketing Manager

sales@pmarketresearch.com

00852-95632430

PW Consulting: www.pmarketresearch.com

Tags

PW Consulting

The Best-reviewed Subdivided Market Risk Analysis Firm in the US and East Asia.