PW Consulting: Prefabricated & Modular Data Centers Market Poised to Expand at a 16.45% CAGR Through 2032

Prefabricated and Modular Data Centers Market — Strategic Outlook for 2026 (PW Consulting)

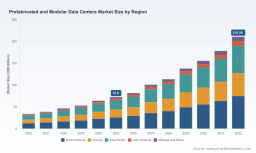

As organizations confront an inflection point where AI-scale compute, edge distribution, and tighter energy regulation collide, PW Consulting’s latest market study on Prefabricated and Modular Data Centers delivers a timed, decision-grade synthesis for boardrooms and engineering teams planning through 2026. Built on a 2025 base-year analysis and a 2026–2032 forecasting horizon, our model projects a sustained compound annual growth (CAGR) of 16.45% across the forecast window. The market we track has grown from the low‑30s (USD Billion) in 2020 to roughly USD 72.5 Billion in 2025 and continues toward a multi‑hundred‑billion-dollar opportunity by 2032 — an expansion that fundamentally reshapes sourcing, site selection, and energy risk calculus for enterprises and hyperscalers alike.

Prefabricated And Modular Data Centers Market

Why this study matters for 2026 business and technical decisions

- Structural demand drivers: Rapid adoption of high-density AI racks and distributed edge architectures is accelerating preference for factory-built modules and containerized pods that minimize on-site construction complexity and time to production.

- Regulatory and energy stress: New policy moves in 2026 — including multi‑state legislation in the U.S. requiring data centers to internalize the cost of new grid infrastructure, and voluntary Ratepayer Protection commitments by major hyperscalers — materially change the economics of site choice and utility procurement.

- Cost and capacity pressure: Rising residential electricity tariffs and the visible contribution of data-center-driven load growth to utility rate filings mean companies must integrate grid-upgrade exposure into TCO models, not treat it as an externality.

- Vendor innovation cycle: Leading suppliers are already delivering modular solutions purpose‑built for liquid cooling, high-power busways, and factory-integrated power/cooling stacks — creating differentiated value for AI and HPC workloads.

What the report delivers — practical, executable assets

PW Consulting deliberately frames this report as an operator’s toolkit, not a pure market narrative. Subscribers receive:

Prefabricated And Modular Data Centers Market

- Proprietary market-size model (2020–2025 historical, 2026–2032 forecast) with scenario toggles for adoption curves, cooling technology mix, and edge vs. hyperscale penetration.

- TCO and payback calculators configurable for CapEx/Opex profiles, grid-upgrade cost pass-through scenarios, and varying PUE and cooling technology parameters.

- Vendor scorecards and procurement playbook: capability matrices, integration risks, manufacturing lead‑time benchmarks, and negotiation levers to compress supplier SLAs into firm delivery timelines.

- Site-selection and regulatory heatmap: a pragmatic checklist mapping permitting risk, grid interconnection exposure, and state-level legislative trends that affect energy charges and upgrade obligations.

- Reference architectures and integration checklists for AI/high-density deployments, including liquid-cooling boundary conditions, containment strategies, and power distribution templates.

- Implementation roadmaps and pilot design templates for rapid validation (3–9 month pilots) to de‑risk larger rollouts.

- Risk register and mitigation playbooks addressing supply-chain disruption, raw-material cost volatility, and workforce constraints in factory vs. field assembly.

Competitive landscape — who matters and how to use this intelligence

Market concentration metrics show a market with meaningful leaders but ample room for specialist providers (our CR3 and CR5 measures indicate a mid‑concentration profile). Understanding supplier strategy and product roadmaps is table stakes for 2026 procurement. Highlights from our competitive analysis:

Prefabricated And Modular Data Centers Market

- Schneider Electric (Rueil‑Malmaison, France) — Continues to scale its EcoStruxure modular portfolio and Prefabricated Pod solutions. Recent product launches focus on high-density AI readiness, integrated liquid cooling, and high-power busway support, positioning Schneider as an end‑to‑end systems integrator for customers seeking rapid, low‑risk deployments.

- Vertiv (Columbus, Ohio, USA) — Aggressively moving to factory‑integrated platforms with its OneCore and SmartRun lines; recent global launches and strategic collaborations underscore a playbook centered on repeatable, high-throughput manufacturing and tight vendor‑end user integrations for AI-scale projects.

- Huawei (Shenzhen, China) — Offers a broad family of FusionModule products oriented to telco edge and scalable prefabricated solutions, emphasizing modular scaling and rapid field deployment in distributed architectures.

- Eaton (Dublin, Ireland) — Positions itself on power resilience and integrated UPS infrastructure, addressing customers for whom uptime and power-quality are primary constraints.

- Specialist integrators and fabricators (e.g., BMarko Structures, CenCore Group, Compu Dynamics Modular, PodTech, TAS, Delta Electronics) — These firms emphasize customization, security compliance (including TEMPEST and other mission-critical standards), and niche capabilities (containerization, custom pod design, or high-density liquid cooling). They often serve edge, colocation, and regulated verticals where bespoke engineering trumps scale.

Recent vendor moves (product launches and strategic partnerships in late 2025 and early 2026) indicate a competitive phase focused on AI‑ready features — liquid cooling, busway power distribution, and factory QA for rapid field integration. For buyers, this creates a clear bifurcation: engage a large systems integrator for end-to-end speed and interoperability, or select specialized fabricators when security, customization, or edge footprint matters more.

Strategic implications and recommended actions for 2026 decision cycles

- Treat grid exposure as a first‑order cost: Integrate utility‑upgrade risk into your financial model and require suppliers to quantify interconnection timelines and any dependencies on local utility reinforcement.

- Adopt a two‑track sourcing strategy: (1) standardized factory-built modules from large integrators for core, high-volume builds; (2) niche builders for edge or regulated sites where customization, security, or local compliance is critical.

- Prioritize modular architectures that minimize on‑site civil works and permit staged capacity increases — this reduces up-front capital and gives flexibility to pivot to denser cooling technologies as rack power increases.

- Negotiate vendor SLAs around upgradeability and retrofitability: ensure pods and modules are designed for lifecycle upgrades (e.g., converting from air to liquid cooling) without full replacement.

- Run accelerated pilots: validate factory acceptance procedures, transport logistics, and multi‑vendor interoperability before committing to volume buys.

- Build a regulatory-response playbook: monitor state legislation and utility filings and design contracts and tariffs that allocate responsibility for grid upgrades transparently.

- Embed supply‑chain resilience clauses: secure priority long‑lead items, and require vendors to publish manufacturing capacity and second‑source options for critical components.

How to deploy the report in your 2026 planning cycle

- Quarter 1: Use the market model and heatmap to finalize site shortlists and quantify utility exposure for each candidate site.

- Quarter 2: Run vendor scorecard assessments and initiate pilot contracts with staged acceptance and clearly defined performance gates.

- Quarter 3: Execute a procurement round leveraging our negotiation playbook to align delivery timelines to utility interconnection schedules.

- Quarter 4: Scale deployments using validated reference architectures, with continuous P&L tracking using our TCO templates and ongoing regulatory monitoring.

PW Consulting’s research is intentionally prescriptive: it does not stop at “what” is happening — it provides the operational tools needed to turn market insight into executable plans that reduce time to value and control energy and regulatory risk.

About the report and next steps

This executive overview is a condensed navigator. The full PW Consulting Prefabricated and Modular Data Centers Market report (base year 2025; forecast 2026–2032) contains the granular tables, region and application segmentations, supplier financial and capability matrices, and downloadable model files that enterprise teams use to build procurement RFIs, capital plans, and deployment schedules. In accordance with our “preview” approach, detailed segment-level figures and complete supplier scorecards are intentionally reserved for the full report to preserve the utility of those datasets for subscribers and clients.

To request the full report, schedule a briefing, or engage PW Consulting for a tailored vendor selection workshop or pilot design, visit our report page or contact the PW Consulting advisory team. We help clients translate the projected market momentum — reflected in the robust historic growth and the 16.45% forecast CAGR — into defensible, auditable deployment programs aligned with both performance and regulatory objectives.

For detailed analysis of this topic, please visit the official page: Prefabricated And Modular Data Centers Market

Lacy Lee

Senior Marketing Manager

sales@pmarketresearch.com

00852-95632430

PW Consulting: www.pmarketresearch.com

Tags

PW Consulting

The Best-reviewed Subdivided Market Risk Analysis Firm in the US and East Asia.