PW Consulting: Automotive Interior & Exterior Trim Market Hits USD 43,590 Million in 2025; Forecast to Grow at 4.7% CAGR Through 2026–2032

Automotive Interior & Exterior Trim Market: Strategic Imperatives for 2026 — A PW Consulting Brief

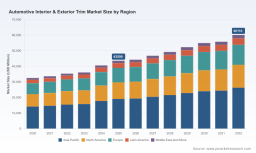

As OEMs and suppliers navigate the confluence of electrification, sustainability mandates, raw-material volatility, and shifting consumer expectations, the automotive interior and exterior trim market emerges as a critical battleground for margin protection, product differentiation, and regulatory compliance. PW Consulting’s latest market study — covering historical performance from 2020–2025 and offering a forward-looking forecast through 2032 — delivers the strategic insights executives need to shape decisions in 2026 and beyond. The global market, measured in USD Million, remains on a steady expansion path with a compound annual growth rate (CAGR) of 4.7% over the forecast period, underscoring durable demand even as structural change accelerates.

Automotive Interior Exterior Trim Market

Why this report matters for 2026 decision-makers

- Tactical sourcing and cost management: With documented resin-price shocks and input-cost pass-through pressures in early 2026, purchasing and procurement leaders must redesign contracts and hedging approaches. Our analysis quantifies sensitivity to polymer price moves and presents tailored sourcing scenarios for short-, medium- and long-term horizons.

- Materials and sustainability readiness: Revised regulatory targets in key markets are raising the bar for recycled-content adoption in vehicle trim. The report translates policy changes into product-level implications and a pragmatic roadmap for achieving compliance without sacrificing supplier margins or aesthetics.

- Portfolio and product strategy: Interior and exterior trim is no longer a commoditized component set. New requirements for smart surfaces, integrated electronics, and premium tactile experiences create monetization paths that require calibrated R&D and industrial investments — we outline prioritized feature sets and go-to-market sequencing.

- M&A and vertical-integration playbooks: Market concentration metrics show meaningful room for consolidation-led scale. Our deal-readiness framework helps corporate development teams evaluate targets, structure earn-outs, and model synergies while preserving customer continuity.

Macroeconomic and market context

PW Consulting’s topline findings place the market on a positive trajectory from the 2025 baseline into the 2032 horizon. The CAGR of 4.7% reflects a combination of technology-led upscaling (smart trim, integrated cockpits), ongoing replacement demand in mature markets, and robust vehicle production in certain emerging markets. This growth is, however, unevenly influenced by three cross-cutting dynamics that every 2026 plan must account for:

Automotive Interior Exterior Trim Market

- Raw-material volatility: Polypropylene (PP) and other resin price swings have reintroduced cost uncertainty in 2026, with notable contract increases and feedstock-driven pressure that impact dashboards, door panels, and exterior moldings. Our report provides sensitivity matrices to model the P&L impact of different resin-price trajectories and recommends strategic procurement levers.

- Regulatory tightening on recycled content: The revised EU End-of-Life Vehicles (ELV) Directive and analogous initiatives elsewhere are creating binding recycled-content targets for new vehicles. We translate these regulatory requirements into material-mix decisions and highlight high-probability compliance pathways, including mechanical recycling partnerships and chemical-recycling pilots.

- Technological convergence and premiumization: Demand for integrated functionality (e.g., haptics, UV/IR-aware coatings, smart surfaces) is driving content-per-vehicle growth in selected segments. Suppliers that combine systems expertise with materials science are best positioned to capture this incremental content.

What the report contains — operational, actionable intelligence

Beyond headline market sizing and a forecast through 2032, this study is expressly designed to be operational for C-suite and business-unit decision-makers. Key deliverables include:

Automotive Interior Exterior Trim Market

- Proprietary market-sizing methodology and forecast scenarios (base, upside, downside) calibrated to production-shift assumptions and policy environments.

- Supplier economics models — unit-cost build-ups for representative interior and exterior modules, including raw-material, labor, tooling amortization, and logistics components.

- Raw-material sensitivity analyses and procurement playbooks that model the P&L impact of resin-price spikes and propose contractual structures (indexed agreements, collars, multi-year supply frameworks).

- Regulatory-impact mapping that converts high-level compliance targets into product-design constraints and cost implications, with mitigations tailored to OEMs and tier suppliers.

- Competitive landscaping and capability-mapping across leading suppliers, with a supplier-decision matrix to guide outsource vs. insource choices and strategic partnership selection.

- M&A playbook and integration checklist covering valuation multiples, synergy capture, operational due diligence, and post-merger retention of key OEM contracts.

- Commercial-closing toolkits — negotiation templates, warranty exposure calculators, and contract clauses that protect margin in a volatile input market.

Competitive landscape: strategic implications for suppliers and OEMs

The supply base for trim remains diversified, with leading global players occupying strong positions across modules and geographies. Market concentration metrics show room for scale-led moves: the top three suppliers together represent a meaningful but not dominant share of the market (CR3 ~28.5%), while the top five raise that share further (CR5 ~42.8%). This structure creates strategic choices for both sides of the value chain.

- Integrated system suppliers (e.g., Magna International Inc., Yanfeng Automotive Interiors): These firms leverage breadth — offering complete body interiors, cockpits, instrument panels, and trim systems — to win platform-level awards. Their advantage lies in systems integration and the ability to internalize incremental electronics and smart-surface content. For OEMs, partnering with such suppliers can speed time-to-market for complex interiors; for competitors, differentiation requires focused R&D investments or niche specialization.

- Interior specialists (e.g., Grupo Antolin, DRÄXLMAIER Group): Their depth in headliners, door panels, and premium surfaces positions them well for OEM programs focused on tactile quality and sustainability. Recent positive order intake and financial performance from some players highlight sustained OEM demand for high-quality interior solutions.

- Seating-focused firms with trim capabilities (e.g., Lear Corporation, Adient plc, Toyota Boshoku): Seat systems remain a high-content area where surface materials and mechanisms converge. Awards and recognition for seating and E-Systems underscore the strategic value of integrated seating+trim offerings, especially as interior differentiation shifts toward occupant experience.

- Tier suppliers with diversified portfolios (e.g., Continental AG, Toyoda Gosei, IAC Group): These organizations offer modular flexibility and can support rapid localization strategies for OEMs. Their capability to adapt product mixes across regions is an asset in environments of demand variability.

Recent industry moves underscore the dynamic nature of the landscape. Notable transactions and developments in 2025–2026 — including major corporate divestments and capital transactions — are reshaping competitive positioning and creating new standalone platforms in the interiors space. Industry awards and investment in sustainability projects also highlight the premium suppliers place on both performance recognition and decarbonization efforts.

How executives should use this intelligence in 2026

PW Consulting recommends a three-part agenda for manufacturers, suppliers, and investors planning for 2026:

- Stabilize margins through procurement redesign: Implement tiered contract structures with indexation for volatile resins, establish multi-supplier strategies for critical polymers, and negotiate flexibility clauses tied to feedstock indices. Use our sensitivity models to set internal trigger points for hedging or price renegotiation.

- Accelerate sustainable-materials adoption on a cost-validated path: Prioritize recycled-content pilots in non-visible components to build supply-chain scale, while preparing validated substitutes for high-visibility surfaces through co-development with material innovators. The report’s regulatory-impact pathways help reconcile compliance timelines with cost targets.

- Differentiate via systems and premium feature roadmaps: Invest selectively in integrated electronics, haptics, and smart-surface technologies that raise content-per-vehicle in targeted segments. For suppliers, bundle capabilities that are hardest to replicate; for OEMs, structure supplier tiers to reward innovation that materially improves perceived interior value.

Limitations and how to get the full picture

This briefing deliberately emphasizes strategic implications and operational playbooks while withholding certain granular sub-segmentation tables and region- or application-level numerical breakdowns that are included in the full PW Consulting report. The complete study contains detailed regional and application splits, unit-cost models, supplier scorecards, and downloadable Excel models that allow you to run bespoke scenarios for your business.

Next steps

For commercial teams, procurement leaders, and corporate development groups preparing 2026 plans, PW Consulting offers tailored briefings and custom scenario workshops that apply the study’s core models to your specific product mix, supplier roster, and exposure to material-price risk. Schedule a strategy session with our automotive interiors team to convert market insights into a prioritized action plan aligned to your 2026 objectives.

To access the full report and the proprietary datasets that underpin our forecasts and operational tools, please visit the PW Consulting publications page or contact our Automotive Practice lead for an executive briefing.

For detailed analysis of this topic, please visit the official page: Automotive Interior Exterior Trim Market

Lacy Lee

Senior Marketing Manager

sales@pmarketresearch.com

00852-95632430

PW Consulting: www.pmarketresearch.com

Tags

PW Consulting

The Best-reviewed Subdivided Market Risk Analysis Firm in the US and East Asia.