PW Consulting: GaN Wafers Market Set to Surge at 18.5% CAGR During 2026–2032PW Consulting Forecast: Platinum–Rhenium Catalysts Market Set to Hit USD 688.9 Million by 2032

Gan Wafers Market 2026 Strategic Outlook: Why PW Consulting’s New Report Is Essential for Executive Decision-Making

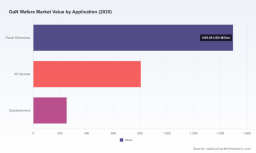

PW Consulting’s latest Gan Wafers Market research report—anchored on a 2025 base year and projecting through 2032—arrives at a decisive moment for semiconductor executives, investors, and procurement leaders. The market has already expanded rapidly, rising from roughly USD 1.05 billion in 2020 to USD 2.55 billion in 2025. Our model projects continued acceleration at a compounded annual growth rate (CAGR) of 18.5% during 2026–2032, resulting in a multi-fold increase in absolute market value by the end of the forecast window. This trajectory, paired with concentration metrics that point to a market where the top three and top five players control a meaningful share, creates both immediate operational risk and strategic opportunity for stakeholders planning activity in 2026.

Gan Wafers Market

What the report delivers: practical, decision-ready intelligence

- Proprietary market model and downloadable financial workbook—scenario-ready and stress-tested—enabling CFOs and strategy teams to quantify revenue and margin sensitivity under alternative growth, price, and material-cost paths.

- Actionable supply-chain map that traces substrate-to-epitaxy flows and identifies chokepoints—material suppliers, specialty equipment, and capacity constraints—allowing procurement teams to prioritize mitigation levers.

- Technology maturity matrix that compares substrate approaches (bulk GaN, GaN-on-Si, GaN-on-SiC, and engineered substrates) on yield, cost-per-wafer, and scale-up risk—designed to inform R&D roadmaps and capex allocation.

- Competitive benchmarking and risk heatmaps for manufacturing scale-up (including 200–300 mm transitions), foundry service positioning, and IP ownership—useful for M&A screening and partner selection.

- Regulatory and raw-material scenario playbooks built around export-control shocks and price volatility—practical templates for supply agreements, hedging, and inventory strategies.

- Commercial go-to-market playbooks and segment adoption case studies that translate technical choices into demand forecasts for power electronics, RF, and optoelectronics—designed for business-unit planning.

We intentionally designed the report to be more than a descriptive survey: every chapter concludes with clearly prioritized recommendation sets and “if-then” execution templates so teams can move from insight to action within sixty to ninety days.

Gan Wafers Market

Why this matters for 2026 decision cycles

Three simultaneous forces are reshaping strategic choices in 2026. First, the market’s growth rate (18.5% CAGR in our baseline forecast) implies sizable near-term revenue opportunities, but this growth is not evenly distributed across technologies or supply chains. Second, market concentration—where leading groups command a significant portion of capacity—creates windows for both consolidation and targeted niche plays. Third, material- and policy-driven volatility (described below) injects supply-side risk that directly impacts commodity-intensive manufacturing economics.

Gan Wafers Market

For executives, this confluence implies that 2026 is the year to make irreversible bets: converting piloted processes to high-volume manufacturing, committing to substrate partnerships, or locking in long-term material contracts. Delay can mean losing preferential access to capacity or facing sharply higher input costs; premature commitment risks technology lock-in. The report’s scenario engine and decision-tree outputs are expressly tailored to help leaders pick the right moment and scale for each bet.

Competitive landscape: who matters and why

- Eta Research Ltd. (Shanghai, China; https://www.etaresearch.com/)—a bulk GaN specialist using an HVPE process that emphasizes free-standing wafers. Its product mix, including UID and semi-insulating variants, positions it as a materials-lead supplier for laser diodes, power, and RF device manufacturers. Strategic implication: forms a logical supply partner for companies seeking shorter lead-times on bulk substrates and flexible doping options.

- Sanan Optoelectronics / Sanan Semiconductor (China; https://www.sanan-semiconductor.com/)—large-scale epi and foundry capabilities with aggressive capacity expansion plans. Strategic implication: attractive foundry partner for OEMs wanting scale and integrated epi services; rival for vertically integrated players looking to protect downstream margins.

- Sumitomo Electric Industries (Japan; https://global-sei.com/)—focus on vapor-phase epitaxy and larger-diameter GaN-on-GaN wafers, plus materials innovation (e.g., performance-oriented substrates). Strategic implication: high-performance and high-reliability customers should track Sumitomo for premium substrate roadmaps and co-development opportunities.

- NGK Insulators (Japan; https://www.ngk-insulators.com/)—proprietary liquid-phase growth yielding low-dislocation substrates. Strategic implication: RF and optical-device makers prioritizing crystalline quality will find NGK’s offering strategically valuable for yield and performance gains.

- IQE plc (Cardiff, UK; https://www.iqep.com/)—broad epitaxy portfolio across substrates and an active partnership approach, exemplified by recent joint development activity. Strategic implication: firms seeking a partner for device platform development (e.g., 650V power devices) should evaluate IQE-led collaborations.

- Wolfspeed, Inc. (Durham, NC, USA; https://www.wolfspeed.com/)—established in GaN-on-SiC and RF power devices, with a strong device-manufacturing footprint. Strategic implication: incumbency in high-performance RF and power segments gives Wolfspeed leverage in setting technology and sourcing norms.

Across this competitive set, the pattern is clear: growth will favor organizations that combine material competence with foundry services or device-level capabilities. Partnerships and joint development agreements will be the fastest path to de-risking scale-up and entering high-value applications.

Recent developments and the policy-shock playbook

Key industry developments illustrate both opportunity and vulnerability. In mid-2025 several milestone events signaled a technology inflection: a leading semiconductor firm announced progress toward scalable 300 mm GaN wafers with customer samples slated for late 2025; another supplier demonstrated GaN-HEMTs on polycrystalline diamond substrates; and an epitaxy specialist entered a joint development arrangement to accelerate a 650V GaN power platform targeting automotive and data-center customers. These technical advances lower the cost-per-watt threshold for GaN adoption and expand addressable end-markets.

At the same time, raw-material and policy noise has become a persistent strategic input. Recent changes in gallium export policy and observed unit-price spikes (industry estimates show substantial YoY increases) have exposed a supply chain vulnerability: a handful of primary producers account for the vast majority of global mined gallium. For markets or regions dependent on imports, that concentration translates directly into procurement risk and margin pressure.

Our report therefore includes a “policy-shock playbook” with practical measures: multi-sourcing matrices, conditional inventory triggers, forward-contract templates with pass-through clauses, and a capital-program checklist for onshoring or recycling investments. These are built as executable items, not high-level suggestions.

How to use this report in practice (90‑day, 12‑month, and 36‑month roadmaps)

- 90 days: Run the supplied scenario model against your product roadmap—test price and material shocks, and produce a procurement action plan. Begin supplier due diligence for at least two non-correlated sources.

- 12 months: Lock in tiered supply agreements and evaluate one strategic equity or JDA with a substrate/epitaxy partner. For device OEMs, initiate pilot runs on alternative substrate options mapped in the report.

- 36 months: Execute capacity expansions or foundry agreements aligned to the highest-return segments identified in our scenario analysis; consider vertical integration where margins and market control justify capex.

Why PW Consulting’s approach is different

Many studies describe the Gan wafers market; few provide the executable link between wafer physics, supply-chain constraints, and boardroom capital decisions. Our report blends an engineer’s technical rigor with a strategist’s focus on implementable choices—complete with downloadable models, supplier scorecards, and playbook templates. Importantly, while this press summary outlines major themes and firm-level positioning, the full report contains the granular segmentation, supplier-level scoring, and interactive financial models that executives need to finalize 2026 budgets and partnership commitments.

Next steps

If your team is preparing capital requests, negotiating multi-year supply contracts, evaluating M&A targets, or scoping a production technology shift in 2026, PW Consulting’s Gan Wafers Market report should be your working document. The public summary demonstrates our analytic depth; the full report provides the confidential segmentation, supplier scores, and scenario-ready models required to move from strategy to execution.

For detailed analysis of this topic, please visit the official page: Gan Wafers Market

Lacy Lee

Senior Marketing Manager

sales@pmarketresearch.com

00852-95632430

PW Consulting: www.pmarketresearch.com

Tags

PW Consulting

The Best-reviewed Subdivided Market Risk Analysis Firm in the US and East Asia.