PW Consulting: Purpura Treatment Market to Rise from USD 520.0 Million in 2025 to USD 774.21 Million by 2032 at a 5.85% CAGR, Fueled by IVIG/Biologics and ITP Demand

Purpura Treatment Market — 2026 Strategic Preview: PW Consulting’s Intelligence Brief

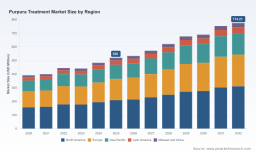

PW Consulting today releases an executive preview of its upcoming Purpura Treatment Market report, timed to inform high-stakes decisions for calendar-year 2026. Built on a rigorous base year of 2025 and a historical series from 2020–2025, our forecast extends through 2032. The sector exhibits steady expansion at a compound annual growth rate (CAGR) of 5.85% (USD, revenue in Million). After recovering from near-term volatility, the market reached approximately USD 520 Million in 2025 and our model projects continued expansion into the latter part of the decade.

Purpura Treatment Market

Why this intelligence matters for 2026 decision-makers

-

Regulatory inflection points in 2025 have altered the competitive and clinical landscape. Multiple approvals and label expansions have reshaped treatment algorithms, particularly for chronic and pediatric cases.

Purpura Treatment Market -

Payer policies and coverage criteria are tightening around prior-line failures and bleeding risk, creating both headwinds and strategic opportunities for differentiated assets.

Purpura Treatment Market -

Supply-side constraints—most notably plasma-derived therapies—impose operational and pricing risks that require proactive supply-chain and sourcing strategies.

-

The market structure shows a meaningful degree of concentration among top players, but room remains for targeted entrants and novel mechanisms of action.

What the full PW Consulting report delivers (practical, transaction-ready content)

-

Integrated market model (base year 2025; historical 2020–2025; forecast 2026–2032) with scenario toggles for uptake curves, pricing sensitivity, and reimbursement scenarios.

-

Clinical and pipeline assessment mapped to commercially relevant endpoints, including timelines to regulatory milestones and probability-adjusted approval modeling.

-

Comprehensive payer landscape and coverage playbooks—detailing common prior authorization criteria, payer levers, and contracting templates for outcome-based arrangements.

-

Go-to-market playbooks for incumbents and late entrants: segmentation of physician specialties, channel mix, key opinion leader (KOL) engagement plans, and field force sizing benchmarks.

-

Manufacturing and supply risk matrix covering plasma sourcing, fractionation capacity, and biologics CMO options, paired with mitigation strategies for inventory-sensitive therapies.

-

M&A and licensing scorecards identifying high-value archetypes, earnout structures, and cost-synergy estimates to accelerate inorganic growth.

Note: This preview intentionally omits the proprietary segment-level tabulations, detailed country splits, and price-by-indication matrices contained in the paid report—those are preserved to protect client value and to encourage direct engagement with our interactive deliverables.

Market dynamics and strategic implications

Several converging dynamics drove our 2025-to-2032 outlook. First, regulatory developments during 2025 broadened the treatable population for certain novel mechanisms—altering demand curves for both established and newer agents. Second, payer behavior increasingly prioritizes evidence of durable benefit versus durable cost, elevating the importance of robust real-world evidence (RWE) programs. Third, manufacturing realities—particularly for IVIG and other plasma-derived inputs—introduce supply-side cyclicality that impacts short-term availability and pricing negotiations.

The net effect is a market that is predictable in aggregate growth but heterogeneous at the product and channel level. Products with clear differentiation—whether via mechanism, pediatric-friendly formulations, or demonstrated steroid-sparing effects—stand to secure premium positioning, while commoditized supply (e.g., undifferentiated generics or volume IVIG) will face margin pressure and contracting scrutiny.

Competitive landscape — leaders, inflection points and tactical moves

Our competitive analysis identifies a cluster of established biopharma and specialty companies actively shaping the category. Recent company developments in 2025 highlight the tactical themes you should expect in 2026:

-

Amgen (Nplate) continues to leverage established market presence and long-term clinician relationships for thrombopoietin receptor agonist coverage—but must balance lifecycle management against emergent competitors.

-

Novartis has demonstrated a strategic push toward combination and sequencing strategies, supported by positive Phase III data in late-stage programs; these data create optionality for label expansion and partnership negotiations.

-

Sobi’s recent pediatric approval and formulation innovations illustrate how line-extension and formulation work can materially change access dynamics in younger populations.

-

Sanofi’s entry with a BTK inhibitor reshapes the modality map and will force incumbent portfolio owners to reassess positioning on safety, outpatient administration, and combination strategies.

-

Rigel’s continued commercialization activities and IP resolution work underscore the importance of legal and lifecycle clarity when forecasting persistent-market shares.

-

Grifols, as a leading plasma/IVIG provider, drives discussions on supply security, allocation priorities and downstream pricing for acute, rapidly effective interventions.

-

argenx’s FcRn-blocker success in certain territories highlights the potential of targeted biologics to capture high-value niches, particularly where RWE supports rapid payer acceptance.

Our market-concentration analysis shows that the top three players control a substantial portion of value, while the top five consolidate well over half of the market—creating a competitive environment where partnerships, price differentiation, and targeted clinical evidence matter more than ever.

Actionable strategic recommendations for 2026

-

Prioritize pediatric and label-extension strategies where incremental approvals can unlock new payer-covered cohorts—early engagement with regulators and pediatric networks is essential.

-

Invest in RWE and health economics early: design registries and pragmatic trials that speak to durability, steroid-sparing outcomes, and hospital utilization impacts to support favorable reimbursement.

-

Secure supply chains for plasma-dependent therapies via long-term supplier agreements, vertical partnerships, or CAPEX commitments to fractionation capacity.

-

Adopt flexible contracting: outcomes-based pricing and indication-based contracting models will accelerate adoption in risk-averse payer environments.

-

Screen M&A and licensing opportunities for biologics and adjunctive technologies that complement existing portfolios, using PW’s target scorecards to prioritize deals that de-risk reimbursement timelines.

-

For new entrants, focus launch resources on clearly defined subpopulations and high-volume centers of excellence where early KOL adoption can cascade into broader coverage.

Methodology and confidence drivers

Our forecast draws on a triangulation of inputs: company financials and filings, regulatory filings, trial registries, claims and commercial diagnostics data, interviews with clinical and payer champions, and proprietary adoption curve modeling. The report uses a base year of 2025, considers historical trends from 2020–2025, and produces scenario-adjusted projections through 2032 (reported in USD, revenue unit: Million). The blended CAGR of 5.85% reflects both conservative and upside scenarios depending on regulatory, supply-chain and payer outcomes.

How to use this intelligence in 90 days

-

Commercial teams: align field segmentation and KOL efforts to updated clinical pathways; incorporate our payer playbooks into contracting conversations now.

-

Clinical development leads: refine late-stage plans to address endpoints that most influence coverage (durability, steroid-sparing, hospitalization avoidance).

-

Corporate development: use our M&A scorecards to prioritize bolt-on biologics and to structure earn-outs that bridge regulatory risk.

-

Supply chain and procurement: begin securing multi-year plasma supply agreements and evaluate CMO options for scaling biologics production.

Next steps — accessing the full intelligence

This executive preview highlights the strategic contours and near-term imperatives we see for the Purpura Treatment Market. To protect the commercial integrity of our work and to deliver bespoke value to clients, detailed segment-level tables, country-by-country breakdowns, price-by-indication forecasts, and our interactive modeling workbook are available only in the full report.

For immediate access to the complete report, interactive model, and bespoke consultation packages tailored to your organization’s stake in the purpura treatment landscape, please visit our report page or contact PW Consulting. Our team stands ready to translate this intelligence into executable plans for M&A diligence, portfolio reshaping, and launch acceleration in 2026.

About PW Consulting

PW Consulting specializes in high-impact strategy and market intelligence for life sciences and specialty care. We combine deep therapeutic expertise, rigorous quantitative modeling, and pragmatic commercial experience to help clients convert market insight into measurable outcomes.

For detailed analysis of this topic, please visit the official page: Purpura Treatment Market

Lacy Lee

Senior Marketing Manager

sales@pmarketresearch.com

00852-95632430

PW Consulting: www.pmarketresearch.com

Tags

PW Consulting

The Best-reviewed Subdivided Market Risk Analysis Firm in the US and East Asia.