PW Consulting: Clinical Disorder Treatment Market Set to Reach USD 892,100 Million by 2032 (Forecast 2026–2032)

Clinical Disorder Treatment Market: Strategic Imperatives for 2026 — PW Consulting Market Brief

PW Consulting’s new Clinical Disorder Treatment Market report (base year 2025) provides a practice-focused, decision-ready intelligence pack designed to shape executive strategy for 2026 and beyond. Anchored in a rigorous historical analysis (2020–2025) and a seven-year forecast window (2026–2032), the report synthesizes market sizing, regulatory shifts, pipeline breakthroughs, provider delivery-model evolution, and competitive positioning to deliver a concise set of actions that commercial, clinical and investment leaders can operationalize immediately.

Clinical Disorder Treatment Market

Market at a Glance — Momentum and Near-Term Trajectory

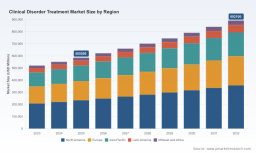

The clinical disorder treatment market demonstrated robust expansion through the early 2020s, reaching approximately USD 585,500 Million (USD Million, base year 2025). PW Consulting’s modeling projects continued industry growth at a compound annual growth rate (CAGR) of 6.18% across the 2026–2032 forecast horizon, with the total market size approaching the high USD hundreds of billions by 2032. This steady healthy expansion reflects converging tailwinds: increasing diagnosed prevalence of mental health conditions, broader reimbursement for behavioral health services, and a widening therapeutic toolkit that includes novel pharmacologies, biologics, device-based interventions and digital therapeutics.

Clinical Disorder Treatment Market

Why This Report Matters for 2026 Decisions

- Timing is critical: 2026 represents an inflection for market structure — regulatory acceleration for novel modalities, high-impact FDA approvals in late 2024–2026, and imminent patent expiries will reshape commercial levers and pricing dynamics.

- Policy and supply chain risk: geopolitical scrutiny of pharmaceutical supply chains and domestic production metrics are changing supplier selection and sourcing strategies for APIs and finished-dose manufacturing.

- Provider delivery transformation: the normalization of hybrid and digitally-enabled care models is shifting referral paths and unit economics in outpatient vs. inpatient settings.

- Fragmented competitive arena: a mix of large pharmaceutical incumbents, generics manufacturers, specialized behavioral health operators and emerging psychedelic/neuromodulation entrants creates both consolidation opportunities and white space for differentiated services.

What the Report Contains — Practical, Transaction-Ready Intelligence

This is not an academic survey; it is a toolkit for action. Key deliverables include:

Clinical Disorder Treatment Market

- Transparent market sizing and historical trend tables (2020–2025) and probabilistic forecast scenarios (2026–2032) incorporating baseline, upside (accelerated adoption), and downside (policy or reimbursement constraints) cases.

- Regulatory heatmap and pathway playbook — evaluating expedited pathways, priority voucher implications for psychedelic therapeutics, and practical steps for engagement with regulatory agencies.

- Patent event calendar and generic risk assessment tailored to therapeutic classes and molecules, with impact quantification on revenue erosion timelines and mitigation levers (line extensions, formulation patents, branded generics strategies).

- Commercial readiness matrices for novel modalities (e.g., intranasal/esketamine models, newly approved atypical antipsychotics, and emerging psychedelic-supported therapies), covering go-to-market staffing, reimbursement dossiers, and distribution channel design.

- Provider and payer playbooks: adoption curve projections for digital/hybrid treatment models, bundled payment scenarios, and utilization management frameworks that payers can deploy.

- Deal and M&A modeler: valuation sensitivities for platform acquisitions (behavioral health providers, digital therapeutics), bolt-on targets, and debt/leverage scenarios for roll-up strategies.

- Risk and resilience assessment for supply chains, including country-of-origin exposure and recommended sourcing hedges for APIs and specialty manufacturing.

Competitive Landscape — Strategic Takeaways

The market remains relatively unconsolidated at the top, creating space for both scale economies and nimble specialization. The report profiles leading pharmaceutical companies, specialty service chains, and generics suppliers, translating capabilities into clear competitive advantages and vulnerabilities.

- Johnson & Johnson (Janssen) — With an established esketamine franchise and a broad neuroscience portfolio, J&J is positioned to leverage real-world evidence and integrated delivery relationships to defend premium pricing and expand label opportunities.

- Eli Lilly — A prominent R&D engine in depression and CNS disorders; strategic priority will be converting pipeline depth into differentiated commercial offerings and securing payer access ahead of competitor formulary moves.

- Pfizer & GlaxoSmithKline (GSK) — Global distribution strengths and deep commercial footprints give these players an advantage in rapid scale-up of new indications, but lifecycle management will be critical as generics pressure increases.

- AstraZeneca & Otsuka — Established antipsychotic franchises create durable cash flows; the near-term imperative is responding to patent expirations and defending market share via combination therapies and newer formulations.

- H. Lundbeck, Bristol-Myers Squibb, Novartis, AbbVie, Takeda — Regional strengths and selective CNS pipelines make these companies natural acquirers or collaborators for specialty platforms and digital partners.

- Teva — As a major generics supplier, Teva’s role in price compression post-patent expiry is central to payer strategies and will materially affect branded product ceilings.

- Acadia Healthcare & Universal Health Services — Large behavioral health networks that control capacity across inpatient, residential and outpatient settings — potential consolidators of fragmented service delivery markets and key commercialization partners for new therapeutics requiring facility-based administration.

Recent Developments That Recast Opportunity Maps

- Regulatory acceleration in early 2026 introduced priority designations for certain psychedelic and related modalities, signaling faster potential routes to commercialization for psilocybin- and methylone-based programs. This materially alters time-to-market assumptions for novel classes.

- FDA approvals and label expansions in 2025–2026 for formulations and indications (including expanded uses for esketamine and newly approved atypical antipsychotics) change the near-term competitive set and uptake patterns.

- Patent expirations in late 2026 for several marketed agents are anticipated to increase generic competition and necessitate pre-emptive lifecycle strategies from impacted originators.

- Policy attention to domestic production and supply-chain resilience — including public statements and proclamations in 2025–2026 — is driving procurement and sourcing choices at both corporate and governmental levels.

Implications for Key Stakeholders

- Biopharma executives: Accelerate scenario planning around patent cliffs and novel-therapy uptake, prioritize portfolio diversification into non-traditional modalities, and fast-track payer evidence generation for differentiated value claims.

- Behavioral health providers: Invest in outpatient and hybrid capabilities, standardize clinical pathways for new therapeutics (including psychedelic-assisted care), and form strategic alliances with payers to pilot bundled reimbursement.

- Payers and health systems: Design coverage frameworks for high-cost but high-value therapies (e.g., facility-delivered or multi-session interventions), update utilization management protocols for hybrid care, and incorporate long-term cost-benefit analyses into formulary decisions.

- Investors and M&A teams: Prioritize platform assets that address fragmentation — orchestrating roll-ups of outpatient clinics, digital therapeutics, and specialty pharmacies — and focus due diligence on regulatory runway and API supply risks.

A Six-Step Roadmap for 2026 Execution

- Stress-test the core portfolio under multiple regulatory and pricing scenarios, incorporating the new expedited pathways and potential rapid generic entry points.

- Develop a prioritized evidence generation plan (RWE and pragmatic trials) to secure reimbursement and accelerate adoption for high-impact indications.

- Lock in diversified API and manufacturing sources; implement supply-chain contingency models that account for import reliance and geopolitical risk.

- Build commercial partnerships with large behavioral health networks and digital health providers to shorten channel friction and capture patient flow.

- Design dynamic pricing and access strategies that can adapt across markets as generics enter and as novel modalities are reimbursed.

- Deploy a targeted M&A screening framework focused on capabilities (e.g., facility capacity, digital engagement platforms, RWE generation assets) rather than geography alone.

Conclusion — What PW Consulting Recommends Next

2026 will be a year when strategy execution outpaces strategy planning. PW Consulting’s Clinical Disorder Treatment Market report provides the calibrated intelligence leaders need to move from insight to action — without overexposing tactical segmentation that competitors could exploit. Our analysis quantifies the magnitude of opportunity and disruption at the market level, maps regulatory and patent events onto revenue and access scenarios, and lays out concrete commercial and M&A playbooks tailored to 12 types of strategic actors.

To review the full, granular datasets, proprietary segment forecasts, regional breakdowns, disorder-type and service-setting analyses, and the detailed company scorecards that underpin our recommendations, please consult the complete PW Consulting report and supporting data annex on our website. The executive summary here is intended to galvanize immediate planning; the full deliverable provides the operative detail required to act decisively in 2026.

For detailed analysis of this topic, please visit the official page: Clinical Disorder Treatment Market

Lacy Lee

Senior Marketing Manager

sales@pmarketresearch.com

00852-95632430

PW Consulting: www.pmarketresearch.com

Tags

PW Consulting

The Best-reviewed Subdivided Market Risk Analysis Firm in the US and East Asia.