PW Consulting Forecasts 9.85% CAGR for Prostate Cancer Diagnostics & Treatment Market, Projected to Reach USD 117,684.46 Million by 2032

Prostate Cancer Diagnostics and Treatment Market: Strategic Imperatives for 2026 — A PW Consulting Preview

Executive Preview

As life sciences leaders prepare their 2026 agendas, the prostate cancer diagnostics and treatment landscape presents one of the most consequential opportunities and strategic challenges of the decade. Our latest market study — anchored on a 2025 base year and a detailed 2026–2032 forecast — projects sustained double‑digit expansion (CAGR 9.85% across the forecast period), with total market value roughly doubling from the mid‑2020s into the early 2030s. This growth is being driven by converging forces: regulatory approvals extending indications into earlier disease stages, rapid adoption of precision diagnostics and PSMA‑targeted approaches, and a widening therapeutic toolkit that now spans next‑generation androgen receptor inhibitors, PARP combinations, radioligand therapies, and advanced imaging solutions.

Prostate Cancer Diagnostics And Treatment Market

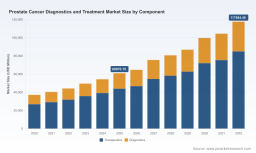

Market Trajectory — What the High‑Level Numbers Tell You

-

From a historical base in the early 2020s, the overall market has accelerated into the mid‑2020s and is projected to continue expanding through 2032. The combination of therapeutic innovation and diagnostic-enabled patient selection underpins a near‑term compounding annual growth rate of approximately 9.85%.

Prostate Cancer Diagnostics And Treatment Market -

This momentum reflects both product‑level tailwinds (new approvals and indication expansions) and infrastructure investments (PSMA‑PET adoption, radioligand delivery capacity, and molecular diagnostic labs) that together increase addressable patient populations and per‑patient care value.

Prostate Cancer Diagnostics And Treatment Market -

Market concentration metrics indicate a moderately concentrated space: the top three firms capture a meaningful share of revenue, while the top five account for a majority — a structure that creates strategic openings for focused challengers, diagnostics specialists, and radiopharmaceutical innovators.

Recent Industry Dynamics That Will Set 2026 Agendas

-

Regulatory momentum is shifting effective therapies into earlier lines of treatment. Recent approvals in 2025 expanded indications for androgen receptor inhibitors and PARP combination regimens; such moves are accelerating clinical adoption and raising the strategic importance of early‑line data generation.

-

Precision selection requirements are tightening. Regulatory bodies increasingly demand companion diagnostics to identify BRCA mutations or PSMA expression as prerequisites for prescription of certain targeted therapies, elevating the commercial value of diagnostic partnerships and in‑house testing capabilities.

-

Radioligand therapies and PSMA imaging are maturing into reimbursed standards where robust imaging evidence exists, creating commercial viability for radiopharmaceutical players and for integrated diagnostic‑therapeutic go‑to‑market models.

-

Patent cliffs are reshaping competitive dynamics. Key androgen receptor inhibitors face loss of exclusivity across major markets in the 2026–2027 window — a change that will drive pricing pressure, accelerate generic entry scenarios, and demand rapid lifecycle management strategies from originators.

What PW Consulting’s Report Delivers — Practical, Transactional, and Strategic

Beyond market size projections, our study is structured to be immediately actionable for commercial teams, corporate development officers, and clinical program leaders. Highlights include:

-

Comprehensive demand model and sensitivity analyses: built to run customizable scenarios (pricing, reimbursement, diagnostic adoption curves) so clients can stress‑test forecasts under alternative regulatory or payer conditions.

-

Segmentation and patient‑flow modeling: granular views by disease stage, diagnostic pathway, and treatment sequence — presented in interactive tables and downloadable data files (note: granular splits and individual segment figures are available in the full report).

-

Pipeline and clinical readouts assessment: rolling risk/benefit profiles for late‑stage assets, with time‑to‑peak models and competitive overlap maps to identify white space for combinations or label expansions.

-

Commercial and market‑access playbooks: launch sequencing, evidence generation roadmaps, payer threshold calculators, and diagnostic reimbursement strategies tailored to radioligands, PARP‑based regimens, and AR pathway inhibitors.

-

M&A and partnering playbook: valuation frameworks for diagnostics, radiopharmaceuticals, and platform assets; due diligence checklists; integration scorecards; and a prioritized list of strategic archetypes for bolt‑on versus transformative acquisitions.

-

Client‑ready materials: executive slide decks, go‑to‑market checklists, and workshop facilitation kits for alignments across R&D, commercial, and market access functions.

Competitive Landscape — Strategic Implications for Leading Players

The competitive map is increasingly bifurcated between large integrated pharma firms with therapeutic portfolios plus diagnostic partnerships, and specialized diagnostics/imaging/radiopharmaceutical companies focused on enabling technologies and patient selection. Key strategic observations include:

-

Integrated pharma (e.g., Johnson & Johnson, Astellas/Pfizer, Bayer, AstraZeneca): incumbents with broad therapeutic franchises are pursuing label expansions into earlier disease stages and combination strategies. They are investing not only in clinical programs but also in companion diagnostics and payer evidence to protect premium pricing even as generics loom.

-

Radiopharmaceutical leaders (e.g., Novartis, Telix): radioligand therapies are transitioning from niche salvage settings into earlier lines where PSMA expression and imaging support use. These players are focused on manufacturing scale, supply chain robustness, and demonstrating real‑world cost‑effectiveness to unlock reimbursement.

-

Diagnostics and imaging specialists (e.g., F. Hoffmann‑La Roche, Siemens Healthineers, GE HealthCare, Abbott, Myriad, MDxHealth, Lantheus): as regulatory guidance increasingly ties therapy to biomarker status, diagnostics companies become gatekeepers to therapeutic uptake. Their strategic lever is integration — whether via companion diagnostics, imaging platforms, or joint value‑based contracting models.

-

Mid‑sized innovation players and clinical test providers (e.g., OPKO, specialized molecular diagnostics firms): these firms can capture outsized value by owning patient stratification touchpoints, but must demonstrate reproducible clinical utility and seamless lab‑to‑clinic workflows to scale.

Strategic Imperatives for 2026 Decision‑Makers

-

Prioritize diagnostic linkage in clinical development. Any late‑stage therapeutic program without a clear companion diagnostic pathway will face regulatory and reimbursement friction. Early co‑development or licensing with validated diagnostic providers is now table stakes.

-

Prepare for post‑patent pricing dynamics. Manufacturers of legacy androgen receptor inhibitors should accelerate lifecycle strategies (combination trials, label diversification, value‑based agreements) to defend revenue ahead of generic entry windows.

-

Invest in radioligand infrastructure or partner aggressively. Given the capital and regulatory complexity of radiopharmaceuticals, pragmatic partnerships with imaging centers, nuclear medicine networks, and regional suppliers can accelerate rollout while de‑risking operational exposure.

-

Adopt a payer‑centric evidence plan. Payers increasingly demand PSMA‑PET–linked outcomes and cost‑effectiveness analyses for coverage decisions; invest in real‑world evidence generation and health economic models early.

-

Use M&A selectively to buy capabilities, not just products. Diagnostic platforms, manufacturing scale for radioligands, and digital care pathways provide higher strategic optionality than one‑off molecule acquisitions in a market moving toward integrated care models.

How PW Consulting Helps — The Strategic Value for 2026

Our report is designed as a decision‑support toolkit for corporate leaders calibrating budgets, clinical programs, and commercial launches in 2026. Clients gain:

-

Fast, defensible market sizing and scenario outputs that map to board‑level KPIs;

-

Actionable market‑access playbooks focused on the reimbursement evidence payers will require;

-

Competitive and partnership roadmaps that identify where to build versus buy; and

-

A confidential advisory option for bespoke model adjustments, integration planning, and live workshops to align cross‑functional stakeholders.

Why This Is a ‘Trailer’ — What We’re Not Releasing Here

To preserve the commercial integrity of the research and to ensure clients get full transactional value, this communication intentionally highlights strategic conclusions and high‑level data (overall market trajectory and concentration indicators) while withholding granular segment‑level figures, regional splits, and detailed revenue per therapeutic or diagnostic subtype. These segmented tables, interactive dashboards, and downloadable financial models are available exclusively in the full PW Consulting report and are provided to licensed clients for integration into corporate planning processes.

Next Steps

If your 2026 strategy will touch clinical development prioritization, launch sequencing, diagnostics partnerships, or M&A in prostate cancer, we recommend three immediate actions:

-

Acquire the full PW Consulting Prostate Cancer Diagnostics and Treatment Market report to access the interactive models and segment‑level forecasts;

-

Schedule a tailored briefing with our senior industry team to map findings to your product portfolio and near‑term decision calendar;

-

Engage PW Consulting for a short‑form workshop to translate market scenarios into a 12‑ to 24‑month operational plan across R&D, commercial, and access functions.

PW Consulting’s analysis equips executives with the evidence and frameworks needed to convert the market’s rapid scientific and regulatory evolution into durable commercial advantage. For full datasets, segmental breakdowns, and client licensing options, please consult the full report on our website or contact our advisory team directly.

For detailed analysis of this topic, please visit the official page: Prostate Cancer Diagnostics And Treatment Market

Lacy Lee

Senior Marketing Manager

sales@pmarketresearch.com

00852-95632430

PW Consulting: www.pmarketresearch.com

Tags

PW Consulting

The Best-reviewed Subdivided Market Risk Analysis Firm in the US and East Asia.