PW Consulting Forecast: Industrial Valves & Actuators Market to Surge to USD 231.04 Billion by 2032, Backed by a 5.45% CAGR

Industrial Valves and Actuators Market 2026: A Strategic Preview for Corporate Decision-Makers

As capital budgets tighten and supply chains recalibrate in 2026, industrial players face complex choices about where to invest, which partnerships to pursue, and how to future‑proof product portfolios. PW Consulting’s latest Industrial Valves and Actuators Market study — anchored on a 2025 base and projecting through 2032 — distills the competitive, commercial, and operational signals executives need to make those choices with confidence.

Industrial Valves And Actuators Market

Market Snapshot — The Big Picture You Must Keep in Sight

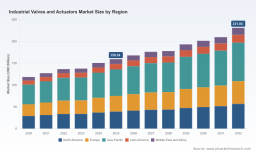

The sector has shown resilient growth across the 2020–2025 historical window and continues on an upward trajectory into the forecast period. Our model starts from a robust 2025 base and projects the market forward at a steady compound annual growth rate of 5.45% through 2032. Under our central case the market climbs materially across the decade, reflecting continued demand for automation, electrification of actuation, and heavy investment in infrastructure and energy transition projects.

Industrial Valves And Actuators Market

Two concentration metrics also matter for strategic positioning: the three‑firm concentration ratio (CR3) and five‑firm concentration ratio (CR5) sit at approximately 28.5% and 41.8% respectively — an industry structure that combines global platform players with a long tail of specialized, regional and service‑oriented firms. That dynamic creates distinct opportunities for scale players to capture system solutions and for niche vendors to monetize expertise and aftermarket services.

Industrial Valves And Actuators Market

Why This Report Matters for 2026 Decision Cycles

- Capital allocation and portfolio strategy. With steady market growth but mounting input‑cost pressures, the report provides the evidence base you need to prioritize R&D, electrification programs, and aftermarket investments over low‑margin OEM commoditization.

- Supply chain and sourcing optimization. Elevated steel pricing and durable tariffs on hot‑rolled coil have reset the math for where to source castings and machined bodies. Our scenarios quantify the sensitivity of margins to raw‑material inputs and offer practical hedging and nearshoring strategies.

- M&A and alliance screening. The market’s moderate consolidation metrics and recent strategic transactions create windows for bolt‑on acquisitions and platform expansion. The study identifies the target profiles that most improve scale or technical breadth.

- Commercial and pricing playbooks. As buyers seek digital integration and lower lifecycle cost, the report maps the willingness‑to‑pay curve for smart actuation, service contracts and retrofit offerings, enabling differentiated pricing strategies.

- Risk and compliance planning. Regulatory shocks and trade policy shifts are now recurring strategic risks; our analysis translates these into quantified scenarios to stress‑test investments and manufacturing footprints.

What’s Inside the Report — Practical, Execution‑Oriented Deliverables

Designed for C‑suite and business‑unit leaders, the PW Consulting study balances rigorous forecasting with concrete operational playbooks. Key deliverables include:

- Proprietary market model and scenario suite (base, upside, downside) through 2032, with sensitivities for commodity pricing, electrification adoption, and capital market cycles.

- Go‑to‑market frameworks for OEMs and aftermarket service providers, including customer segmentation, margin waterfalls, and channel economics.

- Manufacturing footprint decision tool that evaluates total landed cost, tariffs exposure, lead time targets, and service coverage trade‑offs.

- Technology adoption roadmaps that quantify near‑term opportunities from electric actuators, digital actuators, and integrated valve‑instrumentation packages, plus guidance on product platform rationalization.

- Supply‑chain playbook addressing index‑based commodity contracts, strategic inventory policy, and supplier qualification standards for high‑value components.

- Deal origination templates and valuation heuristics tailored to valves and actuation assets, supporting rapid screening of acquisition targets.

- Operational best practices for aftermarket growth — warranty design, remote diagnostics commercialization, and parts log‑management to lift lifetime revenue per installed unit.

Note: To preserve strategic advantage and encourage direct engagement, this summary intentionally omits the granular regional and application split tables and detailed subsegment revenue points available in the full report on our site.

Competitive Landscape — How the Leading Players Are Positioning

The competitive field blends diversified industrial groups, specialist actuator manufacturers, and integrated automation firms. Several firms are particularly noteworthy for their strategic moves and product positioning:

- Emerson Electric Co. — Leveraging a broad portfolio spanning Fisher control valves to Bettis actuators and smart valve technologies, Emerson continues to push integrated automation as a differentiator for end‑to‑end process control customers.

- Flowserve Corporation. — A focus on engineered valves and severe‑service applications, complemented by actuator platforms, positions Flowserve to capture high‑value segments; its recent acquisition activity underscores a push to strengthen offerings in critical infrastructure sectors.

- Rotork plc. — Specializes in intelligent actuation, and its emphasis on electrification and wastewater projects highlights the growing premium for digital and energy‑efficient solutions.

- Bray International, Crane Co., Velan, KSB, SAMSON, AVK — These manufacturers compete across complementary niches (butterfly valves, isolation valves, water and gas markets) and often win through modular product design and local service networks.

- SLB (Cameron) and Baker Hughes — Energy‑focused players provide upstream and midstream valve systems where stringent performance and certification requirements favor established OEMs.

- Specialist actuator suppliers (Parker Hannifin, AUMA) — They are capturing the shift to electric actuation and motion control integration with OEMs and systems integrators.

Recent corporate developments offer directional clarity: Flowserve’s strategic acquisition activity in early 2026 consolidates engineered valve capabilities; Rotork’s 2025 results emphasize electrification and wastewater project wins; Emerson’s full‑year messaging underscores automation tie‑ins as a growth lever. Industry forums — such as the Valve Forum organized by the Valve Manufacturers Association — continue to spotlight technological advances, including gas‑charged hydraulic actuators for nuclear applications, which remain an important niche with high entry barriers.

Key Industry Dynamics to Watch in 2026

- Raw‑material price volatility and trade policy. Elevated hot‑rolled coil prices and persistent tariffs are reshaping total cost of ownership. Manufacturers will need active procurement strategies and closer supplier partnerships.

- Electrification of actuation. Demand is accelerating for electric actuators because of lower maintenance, energy efficiency, and better digital integration. This trend has implications for product roadmaps and aftermarket services.

- Service‑first revenue models. As installed bases age, recurring revenue from predictive maintenance, retrofit kits and remote diagnostics will outpace unit sales growth for many firms.

- Consolidation vs. specialization. Moderate market concentration enables M&A for scale benefits, while niche expertise remains valuable for safety‑critical and severe‑service applications.

- Regulatory and certification complexity. Nuclear, offshore, and power segments impose strict requirements that favor suppliers with proven compliance and qualification records.

Actionable Recommendations for 2026 Executives

- Reprioritize R&D spend toward electric and digitally enabled actuation; quantify lifecycle TCO advantages and embed those narratives into commercial propositions.

- Stress‑test manufacturing networks for tariff and freight scenarios; where economics permit, pursue nearshoring or localized machining centers for high‑weight components.

- Accelerate aftermarket offerings — instrumented service contracts and retrofit kits deliver margin and lock in installed base revenue.

- Pursue targeted M&A that closes capability gaps (e.g., severe‑service valves, digital actuation software) rather than broad scale buys that dilute focus.

- Adopt commodity‑indexed procurement and strategic safety stocks to smooth margin volatility while negotiating supplier performance and innovation commitments.

How PW Consulting Empowers Your 2026 Decisions

Our report pairs predictive market modeling with executable playbooks designed for rapid implementation. If you are evaluating capex plans, M&A targets, product investment trade‑offs, or supply‑chain rework for 2026, PW Consulting provides the scenario modeling, commercial heuristics, and operational templates to translate strategy into deliverable outcomes.

For executives who need the complete dataset — including regional and application-level breakdowns, granular segment forecasts, and the full competitive benchmarking matrix — the full report is available through our publication portal. The high‑resolution tables and company scorecards are intentionally gated: they are designed to support confidential decision processes and to provide subscribers with the fine‑grained intelligence required to act decisively.

Contact PW Consulting to schedule a briefing and a customized scenario walk‑through. Our analysts can map the report’s outputs to your asset base, P&L sensitivities, and strategic milestones to create a prioritized action roadmap for 2026 and beyond.

For detailed analysis of this topic, please visit the official page: Industrial Valves And Actuators Market

Lacy Lee

Senior Marketing Manager

sales@pmarketresearch.com

00852-95632430

PW Consulting: www.pmarketresearch.com

Tags

PW Consulting

The Best-reviewed Subdivided Market Risk Analysis Firm in the US and East Asia.