PW Consulting: Anti-Asthmatics & COPD Drugs Market to Grow at a 4.2% CAGR During 2026–2032, New Insight Report Reveals

Anti‑Asthmatics and COPD Drugs Market: Strategic Preview for 2026 — PW Consulting Intelligence Brief

As healthcare executives, investors and policy leaders prepare strategies for 2026, PW Consulting’s latest market intelligence on Anti‑Asthmatics and COPD drugs provides a focused, operationally oriented vantage on a therapeutic area undergoing both evolutionary and disruptive change. Our report — built on a 2020–2025 historical base and a 2026–2032 forecast horizon — combines quantitative market modelling with decision‑grade qualitative analysis to translate complex clinical, regulatory and commercial signals into practical choices for the coming 18–36 months.

Anti Asthmatics And Copd Drugs Market

Why this market matters in 2026

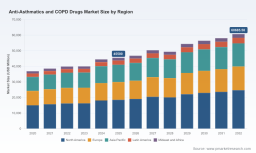

The global Anti‑Asthmatics and COPD drugs market has demonstrated steady expansion through the first half of the decade, rising from a multi‑billion dollar base in 2020 to an estimated USD 45,500 Million (USD Million unit) in 2025. Our forecast expects continued growth at a compound annual growth rate (CAGR) of 4.2% across the 2026–2032 window, reflecting a balance between aging populations, evolving treatment algorithms and rising uptake for novel mechanisms and care models.

Anti Asthmatics And Copd Drugs Market

For 2026 decision‑makers, three high‑level strategic implications follow:

Anti Asthmatics And Copd Drugs Market

- Structural growth provides optionality: a mid‑single digit CAGR supports incremental investment across R&D, life‑cycle management and commercial expansion without presupposing blockbuster returns from any single molecule.

- Clinical and access inflection points are accelerating launch economics: approvals of first‑in‑class and biologic add‑on therapies, together with product‑specific reimbursement constructs, are reshaping launch sequencing and pricing negotiation strategies.

- Sustainability and device innovation are becoming non‑negotiable: regulatory and payer expectations on environmental impact and delivery platforms are moving from reputational differentiators to commercial gating factors.

What PW Consulting’s report delivers for 2026 planning

We designed the report as a practical, board‑level toolkit and an execution manual for commercial teams. Key deliverables include:

- Market sizing and scenario forecasts (2020–2032) calibrated to real‑world uptake curves and reimbursement milestones, allowing users to stress‑test portfolio value under conservative, base and upside cases;

- Launch readiness playbooks for novel inhaled molecules, biologics and combination therapies, covering clinical positioning, payer evidence generation, coding and contracting levers;

- An actionable regulatory and HTA tracker that synthesizes the latest GOLD guidance updates, recent biologic approvals and emerging device standards into decision‑grade implications for label strategy and post‑market surveillance;

- Commercial segmentation frameworks oriented to payer archetypes and hospital vs. ambulatory channels, with tailored go‑to‑market tactics for hospital tenders, specialty pharmacies and primary care adoption;

- Supply‑chain and manufacturing risk maps, highlighting capacity constraints for inhaler components, propellant transition timelines and mitigation actions for critical COGS exposure;

- M&A and partnering heat maps identifying opportunities for bolt‑on respiratory assets, inhaler device collaborations and biologic portfolio extensions, accompanied by modelled valuation sensitivities;

- Comprehensive Excel datasheets and financial models that integrate price erosion scenarios, refill adherence assumptions and novel‑mechanism market entry timelines to produce board‑ready ROI outputs.

Competitive landscape — what matters in 2026

The therapeutic space remains led by established pharmaceutical leaders and a small group of fast‑growing specialised entrants. Market concentration is meaningful: the top three firms account for roughly 45% of the market while the five largest players approach about 60% — a structure that shapes pricing dynamics, formulary access and channel partnerships.

Strategically, the market is being defined by three company archetypes:

- Large integrated majors who compete on scale, diverse inhaler portfolios and access to primary care channels; these firms invest heavily in device ecosystems and life‑cycle management to defend share.

- Specialist innovators commercialising first‑in‑class inhaled mechanisms and niche biologic indications; these players drive clinical differentiation and can disrupt category economics through new reimbursement pathways.

- Generic/replica suppliers and contract manufacturers who pressure price and expand volume channels, particularly in markets where payer sensitivity and tendering dominate.

Representative strategic moves to watch (covered in the report):

- AstraZeneca continues to fortify its inhaled portfolio and is investing in low‑GWP propellants and triple‑therapy combinations — an integrated product + sustainability story that influences procurement conversations.

- Boehringer Ingelheim’s focus on alternative inhaler platforms and long‑acting maintenance therapies keeps it central to hospital and chronic care protocols.

- GSK’s single‑inhaler triple therapies and recent pricing agreements in large markets alter competitive reference pricing and can materially affect launch economics for late entrants.

- Novartis and Chiesi remain important bronchodilator and device players, while Teva’s scale in generics keeps margin pressure on branded assets.

- Verona Pharma’s Ohtuvayre (ensifentrine) represents a rare novel inhaled mechanism entering the market in recent years and demonstrates how rapid reimbursement coding (e.g., J‑code) can materially accelerate access and uptake.

- Sanofi (with Regeneron) introduced a new biologic pathway for COPD patients with eosinophilic phenotype, expanding the treatment paradigm beyond traditional inhaled agents and introducing new payer evidence demands.

Regulatory and reimbursement dynamics shaping near‑term strategy

Regulatory guidance and payer pathways are central to 2026 strategy. Notable context that the report converts into action plans includes:

- Updates in the 2025–2026 GOLD Reports which recast COPD assessment and pharmacologic recommendations — changing the threshold for symptomatic escalation and influencing which products benefit from guideline‑driven formularies;

- FDA and HTA implications from the first biologic approvals for COPD subpopulations, requiring manufacturers to plan for biomarker‑driven labels, companion diagnostics strategy and payer health‑economic dossiers;

- Reimbursement enablers such as product‑specific codes and national procurement agreements (observed pricing arrangements in 2025) that materially impact early launch revenue and contracting tactics;

- The industry‑wide transition to next‑generation low‑GWP pMDI propellants, commencing in 2025, which requires manufacturers to manage reformulation timelines, technology transfer and capital expenditure scheduling to avoid supply disruptions and maintain market eligibility.

Implications for R&D, commercial and M&A decisions in 2026

Our analysis crystallises seven operational imperatives for 2026 decision‑makers:

- Prioritise payer evidence early: build health‑economic models and real‑world evidence protocols during Phase III to shorten time‑to‑contract post‑approval.

- Design device + drug value propositions: sustainability credentials, ease of use and digital adherence features are now as important as molecule efficacy in formulary conversations.

- Stress‑test launch scenarios against coding outcomes: secure coding pathways (e.g., J‑codes) and engage payers proactively to avoid reimbursement cliffs.

- Plan manufacturing transitions with lead time: propellant and inhaler format changes need multi‑year planning and contingency capacity to prevent shortages.

- Segment investments by predictable returns: in a moderate growth market, prioritize assets and partnerships that de‑risk commercial uptake through differentiated clinical profiles or entrenched distribution channels.

- Use M&A selectively to buy capabilities: device co‑development, specialty inhalation platforms and biologic pipelines are common targets to accelerate access to new commercial adjacencies.

- Prepare payer‑centric launch bundles: outcomes‑based contracts, adherence support services and bundled delivery solutions increase payer willingness to adopt premium price points.

How PW Consulting supports execution

Beyond numbers and narratives, the report equips clients with execution templates: payer evidence blueprints, sample contracting language for launch agreements, a prioritized M&A shortlist with modeled synergies, and a supply‑chain mitigation playbook aligned to product life‑cycle stages. For boardrooms and business‑unit leadership, we provide scenario slide decks and financial models that map strategic choices to near‑term P&L and long‑term enterprise value.

Next steps and how to access complete intelligence

This preview outlines the strategic contours that will shape Anti‑Asthmatics and COPD planning in 2026. PW Consulting’s full report contains the complete dataset, detailed segmentation, product‑level forecasts, company profiles, and the operational appendices required to convert insight into action. The report intentionally keeps granular regional and indication splits, and actionable segment tables behind the full publication to ensure clients obtain the complete, up‑to‑date intelligence necessary for precise planning.

For teams preparing 2026 budgets, preparing a launch sequence, or evaluating acquisition targets, our research provides the evidence base and execution playbooks to fast‑track decisions and reduce commercial risk. Contact PW Consulting to obtain the full report and bespoke advisory support to translate these insights into measurable outcomes.

For detailed analysis of this topic, please visit the official page: Anti Asthmatics And Copd Drugs Market

Lacy Lee

Senior Marketing Manager

sales@pmarketresearch.com

00852-95632430

PW Consulting: www.pmarketresearch.com

Tags

PW Consulting

The Best-reviewed Subdivided Market Risk Analysis Firm in the US and East Asia.