PW Consulting Predicts 5.48% CAGR for Synthetic-Based Drilling Fluid Market Through 2032 as Offshore Demand Surges

Synthetic-Based Drilling Fluid Market 2026: Strategic Imperatives from PW Consulting’s New Industry Report

Executive summary

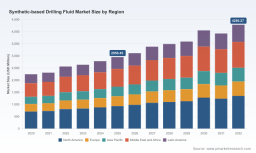

The global synthetic-based drilling fluid market reached an inflection point in 2025, with PW Consulting’s latest proprietary analysis valuing the sector at approximately USD 2.95 billion (base year 2025). Our forecast model projects a steady compound annual growth rate (CAGR) of 5.48% over the 2026–2032 horizon, driven by a mix of environmental regulation, offshore activity recovery, and technology-led product differentiation. For executive teams planning capital allocation, procurement, or M&A activity in 2026, this report translates macro trajectory into actionable choices—highlighting where margin pools will expand, which capabilities will become table stakes, and how regulatory shifts will re-price risk across regions and well types.

Synthetic Based Drilling Fluid Market

Why this report matters for 2026 decision-making

-

Market timing: With a mid-single-digit CAGR and a projected market approaching the mid‑USD 4 billion range by the end of the forecast window, industry participants must prioritize investments that compound value over the next 24–48 months.

Synthetic Based Drilling Fluid Market -

Regulatory inflection: New discharge rules and regional trade measures are already reshaping procurement and product specs—buyers who update specifications and suppliers who invest in compliant chemistries will capture outsized share.

Synthetic Based Drilling Fluid Market -

Supply‑chain pressure points: Feedstock volatility is compressing unit economics for certain synthetic base stocks. Firms that lock in diversified feedstock or localize blending can sustain margins despite cost shocks.

What the PW Consulting report contains (practical deliverables)

-

Granular market model — vetted historic run-rate (2020–2025) and forward-looking scenarios (2026–2032) with sensitivity to oil-price, rig count, and regulatory permutations.

-

Commercial playbooks — procurement levers, cost-to-serve mapping, and supplier scorecards to reduce total cost of ownership for synthetic-based muds (SBMs).

-

Regulatory impact matrix — jurisdictional compliance triggers, discharge thresholds, and a step-by-step compliance checklist for offshore and sensitive onshore operations.

-

Technology and product benchmarking — comparative performance profiles across PAO, ester, ether, linear alpha olefin and hybrid systems, including recommended application windows and OPEX/TCO implications.

-

Competitive intelligence dossiers — strategic profiles and capability maps for market leaders and emerging specialists, including M&A candidate scoring and integration risk diagnostics.

-

Operational scenarios — three playbook scenarios (consolidation, premiumization, and localized supply) with quantified P&L and cash-flow impacts for operators and service providers.

Market trajectory and macro drivers

PW Consulting’s baseline scenario assumes continued recovery in higher‑value offshore activity complemented by selective onshore redirection into complex wells that demand synthetic chemistry for wellbore stability and environmental compliance. The mid‑single‑digit CAGR reflects both upside from higher-specification applications and downside risk from prolonged raw material stress. Importantly, the market is functionally bifurcated: a set of high-performance SBMs that command price premiums in deepwater/HPHT and environmentally constrained environments, and a broader segment serving conventional drilling where cost sensitivity dominates.

Regulation, raw materials and trade — immediate headwinds and strategic responses

-

Regulatory tightening: Recent permit renewals in major producing basins have lowered allowable oil-on-cuttings discharge thresholds, creating a compliance cost for legacy formulations. Firms that can demonstrate low toxicity and rapid biodegradation will gain preferential access to contested contracts.

-

Feedstock volatility: Linear alpha olefin (LAO) feedstock tightened in early 2026 with a double-digit price increase driven by supply constraints, while PAO base‑stock costs saw notable year‑over‑year escalation following regional cracker disruptions. These cost shifts pressure gross margins and elevate the importance of feedstock hedging, alternate chemistries, and localized blending footprints.

-

Trade measures: New cross-border carbon-related tariffs have introduced a cost premium on imported synthetic base oils into certain jurisdictions, forcing buyers to reassess supplier selection and nearshore production options.

Competitive landscape — who matters and why

The sector is characterized by a compact set of large oilfield service firms and a group of specialized formulators. Leading incumbents combine scale, application engineering, and global logistics—advantages that are proving decisive as clients demand both performance and compliance documentation.

-

Schlumberger (M-I SWACO) — Houston: Offers a diverse SBM portfolio, including advanced ester-based systems designed for environmentally sensitive areas. Recent product iterations emphasize biodegradability and North Sea suitability, reinforcing their strength in high-spec offshore work.

-

Halliburton — Houston: Delivers a broad suite of synthetic products optimized for HPHT and deepwater wells; recent approvals under regional discharge regimes enhance their commercial positioning for regulated offshore tenders.

-

Baker Hughes — Houston: Focuses on inhibitive oleaginous systems that improve shale stability and reduce non-productive time (NPT). Strategic capacity builds in the Middle East signal an intent to capture regional deepwater projects.

-

Ecolab (Nalco Champion) — Sugar Land: Known for additive innovation and low-toxicity offerings; their emphasis on lubricity and environmental performance suits offshore operators with tight discharge windows.

-

Newpark Resources — Houston: Specialist in synthetics for challenging directional and extended‑reach wells; their formulations target operational efficiency in high-angle programs.

-

Scomi Oiltools — Petaling Jaya: A rising player with bio-degradable synthetic esters for international markets, offering an alternative to legacy suppliers in select geographies.

Recent strategic moves underscore the competitive framing: product launches focused on biodegradability, regulatory certifications that unlock new contract tiers, and localized capacity expansions to mitigate logistics and tariff exposures. PW Consulting’s report maps these moves against demand pools, surfacing likely winners and vulnerable profiles under each macro scenario.

Strategic plays for 2026 (how to prioritize)

-

For operators: Shortlist suppliers that combine documented environmental performance with local blending options. Negotiate outcome‑based contracting (e.g., cuttings management KPIs) to shift risk and incentivize innovation.

-

For service providers: Invest in certified low‑toxicity chemistries and secure feedstock diversity. Consider brownfield upgrades of blending assets in tariff-exposed regions to preserve margin.

-

For investors: Target mid-size formulators with defensible IP and route-to-market in regulated offshore basins; prioritize businesses with scalable blending capacity and validated biodegradability data.

-

For procurement teams: Implement a hedged purchasing strategy for LAOs and PAOs, and include regulatory compliance milestones in supplier scorecards to avoid stranded exposure.

How PW Consulting’s analytical approach supports decisions

Our methodology combines bottom-up demand modeling with supplier-level cost curves and regulatory overlay. The report’s scenario engine allows clients to stress-test capital and procurement plans across multiple shocks: raw material spikes, tightened discharge limits, and tariff re-pricing. We provide executable templates—contract clauses, supplier audit checklists, and acquisition scorecards—that executives can deploy immediately without reworking internal models.

A word on concentration and competitive dynamics

The market’s dynamics favor players that can pair advanced formulations with logistics and regulatory expertise. While a handful of global firms exert outsized influence in the highest-value segments, pockets of specialization create acquisition and partnership opportunities for fast‑moving challengers. Our competitive cliff‑notes in the report make it clear which combinations of capabilities are most likely to convert regulatory and operational change into revenue growth.

Next steps — how to use the report in 90 days

-

Week 1–2: Run the PW Consulting scenario model against your 2026 budget to quantify sensitivity to feedstock and regulatory shifts.

-

Week 3–6: Use the supplier scorecards and procurement playbook to re-negotiate key contracts and embed compliance KPIs.

-

Month 2–3: Assess M&A or partnership targets identified in the report’s diligence-ready dossiers; prioritize targets that close blending capacity gaps or add certified chemistries.

Conclusion — the value proposition

2026 will be a decisive year for participants in the synthetic-based drilling fluid market. With rising feedstock costs, tightening environmental standards, and trade friction reshaping economics, tactical inertia will result in margin erosion and lost contract opportunities. PW Consulting’s Synthetic-Based Drilling Fluid Market report converts broad market signals into executable decisions—enabling operators, service companies, and investors to protect margin, secure access to compliant chemistries, and capture the next wave of premium drilling activity.

Accessing the full intelligence

This release is a concise extract intended to surface the report’s strategic value. For the complete dataset, regional and application‑level forecasts, supplier scorecards, and the scenario engine that underpins our recommendations, please visit the PW Consulting report page. The full report contains the confidential segment-level analysis, price ladders, and modeled contract language you will need to operationalize a 2026 strategy.

For detailed analysis of this topic, please visit the official page: Synthetic Based Drilling Fluid Market

Lacy Lee

Senior Marketing Manager

sales@pmarketresearch.com

00852-95632430

PW Consulting: www.pmarketresearch.com

Tags

PW Consulting

The Best-reviewed Subdivided Market Risk Analysis Firm in the US and East Asia.