PW Consulting: Speech-to-Text Market to Grow at 16.5% CAGR—From USD 4,850 Million in 2025 to USD 14,126.11 Million by 2032, Led by USD 2,933.47 Million Cloud Segment

Speech To Text Software And Service Market: Strategic Imperatives for 2026 — PW Consulting Market Brief

Executive snapshot

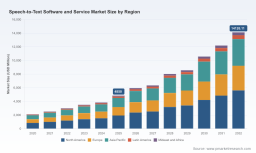

PW Consulting today releases an executive briefing derived from our comprehensive Speech To Text (STT) Software And Service Market report. Between 2020 and 2025 the market more than doubled, rising from roughly USD 2.12 billion to USD 4.85 billion, driven by rapid enterprise adoption across transcription, contact center analytics, healthcare dictation and media workflows. Our analysis projects continued acceleration: the market is expected to exceed USD 5.9 billion in 2026 and grow at a compound annual growth rate (CAGR) of 16.5% through 2032, reaching an estimated USD 14.13 billion by the end of the forecast window.

Speech To Text Software And Service Market

Why this report matters for enterprise decision-makers in 2026

-

Timing procurement and pilots: The turbulence of model innovation and vendor consolidation means procurement windows for optimal pricing and feature sets are narrowing. Organizations that align POC cycles with vendor roadmaps will secure better outcomes.

Speech To Text Software And Service Market -

Architecture choices: Cloud, on-premises and edge/on-device options co-exist — each carries trade-offs for latency, cost, compliance and total cost of ownership (TCO). Choosing the wrong default can lock in multi-year technical debt.

Speech To Text Software And Service Market -

Regulatory readiness: Emerging regulation and data-protection expectations (notably in the EU and healthcare markets) transform STT from a productivity play into a compliance-critical component of enterprise architecture.

-

M&A and partnership signals: The market’s intermediate concentration (CR3 ~45.5%, CR5 ~58.2%) highlights a landscape where strategic acquisitions and deep partnerships will dictate platform leadership for enterprise deals.

Market trajectory — what the macro numbers really signal

The headline growth reflects more than higher transcription volumes. It signals three simultaneous transformations: the move from single-feature speech engines to composable conversational AI stacks; the embedding of STT into end-to-end analytics and automation workflows; and the increasing role of specialized vertical models (e.g., clinical, legal, financial) that demand industry-grade accuracy and compliance.

From an economics perspective, two cost dynamics are especially important for 2026 planning. First, cloud compute economics shifted in 2023 as demand from large generative AI workloads increased GPU inference costs. Second, API pricing for core STT services stabilized in recent years under competitive pressure. Both forces imply that TCO modeling must now account for burst GPU pricing, model complexity and post-processing (e.g., punctuation, diarization, semantic enrichment) that materially affect per-minute processing costs.

Competitive landscape — who to watch and why

The STT market is shaped by a mix of hyperscalers, long-established vendors and nimble specialists. Our vendor mapping distinguishes three archetypes:

-

Hyperscalers extending platform ecosystems: Leaders here provide high-scale cloud STT with deep integration into broader cloud services and enterprise accounts. Their strengths are global reach, model training scale and enterprise SLAs; their challenges include complexity and bargaining leverage for large customers.

-

Specialist transcription and analytics vendors: These firms focus on accuracy, language coverage, and domain-specific customization for customers that need performance in noisy or multi-speaker environments.

-

Edge and privacy-first providers: On-device STT vendors enable local processing for latency-sensitive and privacy-constrained applications, appealing to IoT, automotive and regulated industries.

Representative players we profile in depth include cloud platforms with mature STT APIs and enterprise integrations; vendors with clinical or contact center specializations; developer-first companies offering rapid integration and advanced post-processing (summarization, entity extraction); and edge vendors that remove cloud dependence for privacy or latency reasons. Recent notable moves underline market dynamics: hyperscaler model releases and acquisitions that fold specialized technology into broader enterprise suites, specialist product launches that push accuracy and latency frontiers, and framework releases that enable LLM-based post-processing of STT outputs.

Recent product and industry milestones shaping buyer choices

-

Hyperscaler and specialist model investments have materially raised baseline accuracy and multilingual coverage, changing the economics of global deployments.

-

LLM-driven post-processing features — such as automatic summarization, entity extraction and intent mapping — are increasingly available as bundled services or partner integrations and are becoming differentiators for higher-priced tiers.

-

Mergers and strategic acquisitions continue to re-orient enterprise go-to-market motions, especially where speech vendors are integrated into sector-specific platforms (healthcare, legal, contact center orchestration).

Regulatory and operational headwinds you cannot ignore

-

Regulation: Jurisdictions are moving to classify certain voice-based biometric and profiling systems as “high-risk,” requiring documented risk assessments and transparency. Enterprises deploying real-time or inferential speech systems must bake regulatory compliance into design from day one.

-

Data privacy: In regions where voice is treated as sensitive biometric data, explicit consent processes and data minimization strategies are mandatory. For healthcare use cases, HIPAA-level controls remain non-negotiable.

-

Cost pressure from compute: The uptick in GPU demand for generative workloads introduced volatility in inference costs; buyers should plan for variable-runway compute expenses and consider commitments, reserved capacity or hybrid edge architectures.

-

Operational complexity: Production-grade STT requires systems for model drift monitoring, error-rate benchmarking in target acoustic environments, and continuous post-deployment tuning — capabilities many organizations underestimate.

What PW Consulting’s full report delivers (practical, action-oriented content)

The full market report is designed as a decision-support toolkit for 2026 planning cycles. Highlights include:

-

A transparent market-sizing and forecasting methodology (historical 2020–2025, forecast 2026–2032) that lets clients run sensitivity analyses.

-

Vendor scorecards and a quadrant-style competitive map that evaluate technology maturity, vertical readiness, integration kit quality, and commercial models.

-

Operational playbooks: POC templates, acceptance criteria for transcription quality, speaker diarization and semantic enrichment; and a procurement checklist that addresses licensing traps and IP ownership.

-

Cost and TCO models: configurable worksheets that let procurement teams compare cloud, hybrid and on-device architectures under realistic workload profiles.

-

Compliance matrix: mapped regulatory obligations across jurisdictions and verticals, plus recommended data governance controls and encryption standards.

-

Go-to-market and M&A intelligence: target lists, partnership playbooks and signals to watch for vendors likely to be acquisition candidates.

To maintain the briefing’s role as an actionable teaser, detailed segment splits by region, type and application — along with full numerical vendor rankings and downloadable modeling templates — are reserved for the full report and subscriber portal.

Strategic recommendations for 2026 (what action to take now)

-

Adopt a hybrid deployment posture. Combine cloud STT for scale with on-device or private inference for latency-critical and privacy-sensitive flows. This reduces cost exposure to volatile cloud GPU markets while meeting regulatory constraints.

-

Prioritize verticalized accuracy. For high-value use cases (clinical documentation, financial transcription, legal discovery), invest in domain adaptation and vocabulary customization early in pilots.

-

Build compliance into procurement. Require documented data retention, consent mechanisms and model explainability guarantees in vendor contracts. Make compliance SLAs part of procurement scorecards.

-

Instrument production voice systems. Implement continuous evaluation (WER and downstream task impact) and model monitoring pipelines to detect drift across accents, acoustic conditions and evolving content.

-

Negotiate commercial flexibility. Seek API pricing floors, commitment-based discounts and clauses that account for model upgrades or portability to avoid lock-in penalties.

-

Consider strategic M&A or partnerships selectively. For enterprises building differentiated voice capabilities, acquiring or partnering with specialist vendors can accelerate roadmap delivery and lock in expertise.

Conclusion — positioning for advantage in 2026

The Speech To Text market is maturing from a feature market into an infrastructure and compliance-critical layer of enterprise AI stacks. For 2026 planning cycles, the imperative is clear: combine rigorous vendor evaluation and TCO modeling with operational readiness for regulatory and cost volatility. The next 12–18 months will determine which platforms become integral to enterprise workflows and which remain point solutions.

PW Consulting’s full Speech To Text Software And Service Market report provides the quantitative backplane, vendor analytics and implementation tools enterprise leaders need to make defensible 2026 decisions. Access to our vendor scorecards, downloadable cost models and the full dataset is available in the complete report and subscriber portal.

For detailed analysis of this topic, please visit the official page: Speech To Text Software And Service Market

Lacy Lee

Senior Marketing Manager

sales@pmarketresearch.com

00852-95632430

PW Consulting: www.pmarketresearch.com

Tags

PW Consulting

The Best-reviewed Subdivided Market Risk Analysis Firm in the US and East Asia.