PW Consulting: Lowdk Glass Fiber Cloth Market Poised to Grow at an 8.15% CAGR During 2026–2032

Lowdk Glass Fiber Cloth Market: Strategic Imperatives for 2026

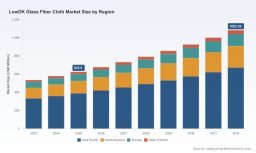

PW Consulting’s new market study on Lowdk Glass Fiber Cloth provides a forward-looking playbook for executives making high-stakes capital, sourcing, and product decisions in 2026. Anchored on 2025 as the base year and spanning historical analysis from 2020–2025 with a forecast through 2032, the report synthesizes macro growth drivers, supplier dynamics, and tactical levers that determine commercial outcomes in a market growing at a compound annual rate of approximately 8.15%.

Lowdk Glass Fiber Cloth Market

Why 2026 is a Pivotal Year

2026 sits at the inflection between immediate capacity shocks and longer-term structural demand led by AI servers, high-performance networking, and next-generation wireless infrastructure. Our models show the total market continuing an uninterrupted expansion from the mid-2020s into the early 2030s, reflecting durable secular demand for ultra low-loss, low-dielectric and low-CTE glass fabrics used in advanced PCBs, IC substrates, and high-frequency interconnects.

Lowdk Glass Fiber Cloth Market

-

Base-year anchoring and scenario-ready outputs: The report uses 2025 as the quantitative anchor and projects through 2032. Readers receive scenario-adjusted revenue curves and sensitivity testing keyed to key inflection points in supply and end-market adoption.

Lowdk Glass Fiber Cloth Market -

Decision horizons mapped to execution windows: We translate the market’s growth trajectory into recommended windows for capex, inventory accumulation, and contractual commitments, aligning procurement and manufacturing timelines with predicted relief in supply constraints.

Market Dynamics: What Is Driving Growth — and What Could Stall It

The structural demand story is clear: the Lowdk glass fiber cloth market is being pulled by higher-performance compute and communications architectures that require progressively lower dielectric constants and tighter thermal-mechanical behavior. This creates a sustained premium tier of materials where average selling prices and margins significantly outpace standard electronic glass products.

-

Demand-side acceleration: AI training clusters, high-speed servers, and next-wave 5G/6G radio and backbone equipment are principal drivers. These end-markets have shifted supplier selection from cost-first to performance-first for critical dielectric and CTE properties.

-

Supply-side constraints: Lead times for advanced low-Dk and low-CTE products have lengthened materially, with capacity tightness expected to persist into mid-2027. Capacity additions will matter less than technology parity: not all new meters of fabric can meet ultra-low-loss specifications.

-

Price dynamics and margin segmentation: Premium glass variants carry a multiple of the ASP of commodity E-glass; the gulf between standard and specialty materials fuels supplier profitability but raises procurement risk for OEMs and CCL makers.

-

Geopolitics and localization: High-end supply remains concentrated among Taiwanese and Japanese producers. Recent southward capacity initiatives and cross-border collaborations are beginning to mitigate geographic concentration, but geopolitical risk and customer preference for supply proximity will continue to influence sourcing strategies.

Competitive Landscape: Who Matters and Why

The competitive map is a mix of integrated glassmakers, specialty fiber producers, and nimble fabricators. Market concentration is meaningful at the top end, with the leading firms collectively controlling a majority share of the advanced product segment — a structural feature that creates both supply-side leverage and opportunities for vertically aligned competitors.

-

Nittobo (Nitto Boseki Co., Ltd.): A Tokyo-based integrated leader that retains dominant positions in advanced NE- and T-glass categories used for high-frequency PCBs and IC substrates. Their product breadth and control over fiber-to-cloth integration make them a bellwether for pricing and availability.

-

AGY: The U.S. specialty glass player is scaling capacity in Aiken, South Carolina, while advancing L-Glass variants targeted at AI-PCB and semiconductor packaging use cases. Recent investments and a partnership to produce North America’s first low-CTE fabric position AGY as a pivotal local source for Western supply chains.

-

Taiwan Glass, Fulltech, and Nan Ya: Taiwanese fabricators are expanding high-end production to capture AI-driven demand. Their proximity to major CCL and PCB clusters and investments in high-performance lines make Taiwan a continued heartland for advanced substrates.

-

Regional fabricators and integrators: Players in China and other Asian markets are expanding scale rapidly. New large electronic glass fiber and fabric lines are coming online, which will increase volume availability but require tight quality governance to meet the top-tier electrical and mechanical tolerances.

Recent industry moves underline the strategic momentum: product launches of next-generation low-dielectric fibers, targeted capacity investments, and cross-company partnerships to localize high-margin fabrics. These developments are creating a bifurcated market where access to validated, high-performance supply chains is a competitive moat.

What the PW Consulting Report Contains: Practical, Executable Tools

Beyond market sizing and forecasts, the report delivers actionable tools that procurement, C-suite, and business development teams can use immediately:

-

Supplier decision matrix: A weighted, validated scorecard covering technical capabilities, capacity timing, geographic resilience, and price elasticity for key suppliers — designed to shorten vendor selection cycles.

-

Capex and inventory timing model: Scenario-driven guidelines for when to commit to brownfield expansions vs. third-party tolling, and recommended buffer inventories by risk profile.

-

Product-roadmap alignment: Mapping of substrate performance thresholds to product architectures — enabling OEMs to prioritize which cloth grades to qualify for near-term designs versus long-range R&D investments.

-

Commercial playbooks: Negotiation levers for buyers, including contractual structures to hedge ASP volatility, joint development arrangements, and tiered pricing linked to verified material performance.

-

M&A and partnership screening: A pragmatic framework for evaluating bolt-on acquisitions or strategic alliances that accelerate route-to-market for specialty fabrics or secure proprietary yarn supply.

-

Regulatory & geopolitical stress tests: Trade-scenario simulations and contingency plans that account for regional concentration of high-end supply and potential export controls.

Strategic Recommendations for 2026

For executives who must act this year, our top-line recommendations are:

-

Prioritize qualification with multiple validated suppliers across geographies: Dual-sourcing reduces execution risk but must be balanced against qualification costs and yield fragmentation.

-

Target selective vertical integration or exclusivity deals for mission-critical cloth grades: Where margin and performance upside are significant, securing priority of supply through equity, JV, or long-term offtake makes commercial sense.

-

De-risk supply by front-loading critical inventory in H1 2026 when justified by end-market backlog and contractual protections — but avoid broad-based stockpiling that locks capital inefficiently.

-

Invest in materials validation capability: Companies that can reduce qualification time from months to weeks gain decisive commercial advantage in a tight market.

-

Monitor ASP dynamics and prepare tiered pricing strategies: Given the steep price dispersion between commodity and specialty glass, price pass-through strategies and product-tier governance are essential.

Implementation Playbooks

PW Consulting provides short-form playbooks tailored by buyer archetype:

-

OEMs & Tier-1s: Fast-track material co-development with a shortlist of high-quality suppliers; condition long-term supply agreements on performance milestones to protect pricing.

-

Material producers: Prioritize capital allocation to lines that materially improve dielectric and CTE performance rather than pure tonnage, and pursue partnerships that provide downstream validation pathways.

-

Private equity & corporate development teams: Use our M&A screening to identify targets that offer unique yarn-to-cloth IP or localized production capability in strategically important geographies.

How This Report Creates Strategic Value

Our study combines granular technical understanding with commercial analytics: it quantifies growth at the total-market level, models capacity cadence, simulates price pathways, and translates these into operationally useful decisions. The report’s strength lies in shaping the tactical choices — timing of investments, supplier prioritization, and contract structures — that materially affect P&L outcomes through 2028 and beyond.

Note: This press article highlights core market architecture, dynamics, and strategic takeaways. Detailed regional and application splits, proprietary price curves, and company-level revenue assumptions are intentionally withheld from this release to preserve the report’s role as a working tool for subscribing clients.

Recent Industry Signals Worth Watching

-

Product innovation and upstream supply: New low-dielectric fiber introductions and yarn-level product launches are shortening the path to higher-performance fabrics for semiconductors and AI servers.

-

Regional capacity & partnerships: Announced investments and strategic partnerships are accelerating local supply options in North America and Asia; these will reshape logistics, qualification lead times, and local sourcing economics.

-

Price and lead-time volatility: Expect ongoing ASP pressure for premium grades and extended lead times through mid-2027, requiring buyers to adopt more sophisticated hedging and contractual protections.

Next Steps

For strategic teams preparing capital plans and procurement strategies in 2026, PW Consulting’s Lowdk Glass Fiber Cloth report is a decision-ready resource. The full report contains the numerical deep-dive, supplier scorecards, and executable templates referenced in this release. To access the complete dataset, model files, and tailored advisory sprints, please visit our official report page.

PW Consulting — turning market complexity into operational advantage for leaders in materials, electronics, and advanced manufacturing.

For detailed analysis of this topic, please visit the official page: Lowdk Glass Fiber Cloth Market

Lacy Lee

Senior Marketing Manager

sales@pmarketresearch.com

00852-95632430

PW Consulting: www.pmarketresearch.com

Tags

PW Consulting

The Best-reviewed Subdivided Market Risk Analysis Firm in the US and East Asia.