PW Consulting: Kraft Paper Bag Market Poised to Expand at a 5.45% CAGR During 2026–2032, New Report Finds

Kraft Paper Bag Market: Strategic Imperatives for 2026 — PW Consulting Report Preview

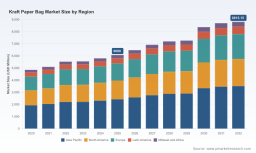

PW Consulting’s new market intelligence on the global kraft paper bag sector synthesizes a multi-year demand model, competitive positioning maps, regulatory-risk heatmaps, and executable commercial playbooks designed to inform board-level and business-unit decisions in 2026. The global market reached an estimated USD 6,080 million in 2025 and — driven by structural sustainability shifts, packaging policy changes, and e-commerce demand elasticity — is projected to expand at a compound annual growth rate (CAGR) of 5.45% through our 2026–2032 forecast horizon. By 2032 the market is expected to be approaching the high single-digit billions (detailed datasets and scenario tables are available in the full report).

Kraft Paper Bag Market

Why 2026 Is a Pivotal Year for Strategic Choices

-

Policy inflection points are compressing decision windows. Extended Producer Responsibility (EPR) schemes and updated packaging rules in major jurisdictions are shifting total lifecycle costs toward producers and brand owners. For companies that postpone compliance planning, 2026 will present retrofitting costs and margin pressure that are materially higher than incremental investments taken earlier.

Kraft Paper Bag Market -

Raw material and input cost volatility remain a live risk. Recent commodity signals — including kraft pulp price levels and a tighter U.S. producer-price backdrop for industrial converting papers — are already influencing procurement and pricing strategies. Procurement-led manufacturers who reconfigure sourcing and hedging in early 2026 will enjoy a disproportionate share of margin improvement in the subsequent two-year window.

Kraft Paper Bag Market -

Consolidation and scale investments are accelerating. Capital commitments by integrated global players to increase high-speed converting capacity and specialty formulations are reshaping supply dynamics. Market concentration remains modest (CR3 and CR5 levels indicate opportunity for regional challengers), but targeted capacity additions create new competitive equilibria in certain product and channel niches.

Market Dynamics — What’s Driving Growth and Where Pressure Emerges

The market’s mid-single-digit growth reflects several durable trends: consumer and retail demand for recyclable fiber-based packaging; substitution away from problem plastics in select foodservice and retail channels; and increases in single-bag weights driven by heavier-duty industrial and construction applications. At the same time, manufacturers face cost pressures from pulp and energy, regulatory compliance costs associated with EPR regimes, and the need to finance product innovations such as high-strength, barrier-treated kraft solutions for moisture-sensitive goods.

-

Regulatory environment: European packaging reforms and the expansion of U.S. state-level EPR programs are creating a new baseline for compliance costs and reporting obligations. Companies must now plan for producer registration, packaging data streams, and end-of-life financing — functions that will affect product design, supplier contracts, and total cost-to-serve models.

-

Input cost signals: Commodity and PPI indicators through early 2026 show elevated and variable pricing for unbleached kraft and related converting grades. These signals necessitate more dynamic pricing clauses in commercial contracts and proactive inventory and supplier diversification strategies.

-

Demand composition: Growth is uneven across application categories and bag types. While foodservice and retail channels continue to favor recyclable, printed, and consumer-facing formats, industrial segments require high-strength, multi-wall and heavy-duty solutions, creating parallel needs for innovation and capacity specialization.

Competitive Landscape — Players, Positioning, and Recent Moves

The sector remains fragmented at the top end, with global integrators, regional specialists, and flexible packagers pursuing differentiated plays. Our analysis highlights several strategic archetypes:

-

Global integrated platforms that combine pulp, paper, and converting capabilities, pursuing scale and system-level sustainability claims — examples include established European and North American groups with global production footprints.

-

Regional, growth-oriented players that leverage local raw-material advantages and fast commercial cycles to serve foodservice and retail customers with customized, certification-backed offerings.

-

Flexible converters and specialty suppliers that target innovation-led niches such as tamper-evident, compostable, and high-barrier kraft solutions for premium beverage and pharmaceutical channels.

Notable recent developments that illustrate the competitive momentum: leading global producers are adding converting capacity in key e-commerce and industrial markets, and sustainability-reporting by specialized paper mills is increasingly tying product roadmaps to customer decarbonization targets. PW Consulting’s profiles of the top global participants detail strategic intent, manufacturing footprints, and product portfolios — enabling rapid benchmarking for procurement and M&A teams.

Strategic Imperatives — What 2026 Decision-Makers Should Prioritize

Boards and commercial leaders should orient 2026 planning around three parallel agendas: resilience in supply and cost, commercial differentiation through sustainability and service, and targeted capacity/capability investments. Our advisory recommendations include:

-

Operational resilience: Implement rolling 18–24 month procurement scenarios that stress-test suppliers and logistics for commodity spikes and regional regulatory disruptions. Diversify fiber sources, negotiate index-linked contracts where appropriate, and model buffer inventory strategies by SKU economics rather than across-the-board days-of-supply targets.

-

Commercial and product strategy: Prioritize product variants that balance recyclability claims with margin performance. For brand owners, re-specification exercises that move to standardized, certified kraft formats can reduce SKU complexity and improve compliance reporting under EPR regimes.

-

Capex and partnership plays: Targeted investments in high-speed converting and printed bag capabilities pay back in channels with strong unit economics (e.g., multi-wall industrials, high-volume retail chains). Alternatively, strategic partnerships or toll-converting agreements can deliver capacity without long-cycle capital.

-

M&A and competitive defense: With market concentration modest at the top, bolt-on acquisitions remain an effective route to scale in priority regions or to acquire specialty technologies. PW Consulting’s deal models identify where acquisition multiples align with synergies from procurement, distribution, and product cross-sell.

Report Contents — Practical Tools and Deliverables

This PW Consulting report is built for decision execution, not just trend observation. Key deliverables include:

-

A calibrated demand model spanning 2020–2032 with base-year validation and three demand scenarios (conservative, central, upside), including sensitivity to pulp and energy prices.

-

Competitive-positioning matrices for leading suppliers, mapping capabilities, certification credentials, and channel strengths to support supplier selection and contract negotiation.

-

Regulatory-impact heatmaps that quantify likely cost and operational load from EPR and packaging directives across major markets, with recommended compliance pathways and timelines.

-

Product roadmaps and SKU rationalization templates that enable companies to align sustainability claims with margin objectives and printing/labeling constraints.

-

Commercial playbooks for pricing, indexation clauses, and customer segmentation — designed to protect margin while accelerating penetration into retail and e-commerce channels.

-

M&A and capex decision tools, including valuation ranges, synergy levers, and integration checklists aligned to the market’s competitive structure.

How PW Consulting Builds Credible, Actionable Forecasts

We combine proprietary shipment and capacity datasets, verified corporate disclosures, plant-level production intelligence, and primary interviews with procurement and packaging directors across retail, industrial, and foodservice verticals. Our modeling integrates commodity price scenarios, regulatory cost add-ins, and cross-elasticities between competing materials so that users can move directly from insight to a quantified commercial plan. The report’s central forecast reflects this multi-source triangulation; the dataset is accompanied by a workbook that allows users to run “what-if” scenarios across price, demand, and policy variables.

Next Steps for Executives

-

Procurement leaders should request the report’s supplier risk matrix and the 18–month sourcing playbook to begin trader-level negotiations before mid-2026 budgeting cycles close.

-

Product and sustainability teams should prioritize the report’s compliance roadmaps and SKU rationalization templates to align with incoming EPR requirements and brand-level net-zero commitments.

-

Corporate development and strategy teams should use our valuation primers and consolidation scenarios to evaluate bolt-on targets and capacity-acquisition opportunities where regional scale is a strategic priority.

PW Consulting’s market concentration analysis indicates that although a handful of global players exert notable influence, meaningful opportunity exists for agile regional champions and specialized converters to capture value. To see the full quantitative breakdowns by product type, application, and geography — including the detailed forecast tables, company profiles, and regulatory impact quantifications that underpin the strategic recommendations above — access the complete report and downloadable datasets on our website.

For decision-makers who need to convert insight into action in 2026, our report provides the analytical backbone, operational playbooks, and prioritized investment options to navigate input volatility, regulatory change, and evolving customer expectations. Contact PW Consulting to request a briefing and sample dataset tailored to your organization’s position in the kraft paper bag value chain.

For detailed analysis of this topic, please visit the official page: Kraft Paper Bag Market

Lacy Lee

Senior Marketing Manager

sales@pmarketresearch.com

00852-95632430

PW Consulting: www.pmarketresearch.com

Tags

PW Consulting

The Best-reviewed Subdivided Market Risk Analysis Firm in the US and East Asia.