PW Consulting Forecast: Cell Culture Media for Research Market to Surge to USD 5,373.6 Million by 2032

Cell Culture Media for Research Market — Strategic Imperatives for 2026: A PW Consulting Report Preview

PW Consulting’s newest market research preview on the Cell Culture Media for Research market synthesizes quantitative forecasting, supplier benchmarking and pragmatic playbooks to support executive decision-making in 2026. This article highlights the strategic value of the full report for product leaders, supply chain chiefs, BD/M&A teams and institutional purchasers, while intentionally withholding granular segment tables and regional splits to preserve the “trailer” experience: show the insight, not every number. For full datasets, interactive models and supplier scorecards, access the complete report.

Cell Culture Media For Research Market

Executive snapshot: scale, growth and market structure

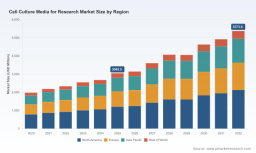

The market for cell culture media used in research reached approximately USD 3.05 billion in 2025 and is forecast to expand at an 8.45% compound annual growth rate through our 2026–2032 horizon, reaching roughly USD 5.37 billion by 2032. Market concentration is meaningful: the top three players account for just under three-fifths of the market, while the top five together approach three-quarters — a structure that combines sizable incumbent power with clear whitespace for focused challengers.

Cell Culture Media For Research Market

Why 2026 is a turning point

-

Translational scaling and reproducibility have moved from laboratory talking points to procurement imperatives. As preclinical workflows increasingly feed cell- and gene-therapy pipelines and biologics research, reproducibility across batches and sites is a primary buying criterion for institutional end users.

Cell Culture Media For Research Market -

Cultures of choice are shifting. Chemically defined and serum-free formulations are accelerating their adoption because they materially reduce batch-to-batch variability and diminish contamination risk associated with animal-sourced components. This trend reshapes product roadmaps, raw material strategies and quality systems.

-

Raw material traceability is now both a scientific and commercial differentiator. Complex global sourcing of amino acids, vitamins and growth factors creates traceability and qualification burdens for media manufacturers and their customers. These upstream pressures are pushing firms to re-think supplier consolidation, vertical integration and transparency tools.

-

Regulatory positioning matters earlier. A large share of commercially available research media are sold as Research Use Only (RUO), requiring additional qualification before therapeutics or diagnostics use. Firms that can demonstrate robust documentation and accelerated qualification pathways gain negotiating leverage with translational customers.

-

Supply-side constraints persist. Fetal bovine serum (FBS) supply is geopolitically and operationally constrained; industry data indicates fewer than 10% of global slaughterhouses participate in certified collection programs. That scarcity accelerates demand for serum-free and chemically defined alternatives and has downstream cost and sourcing implications.

Strategic implications for 2026 corporate planning

-

Portfolio prioritization: Companies should accelerate development and commercialization of chemically defined and serum-free media offerings targeted to high-value translational segments, while retaining classical media for cost-sensitive research contexts.

-

Supply-chain defensibility: Invest in supplier qualification, multi-sourcing for critical raw materials and digital traceability platforms. Firms that can demonstrate end-to-end traceability will capture premium mindshare among translational customers.

-

Manufacturing and scale path: Design R&D-to-manufacturing continuity programs (e.g., media optimization labs, pilot-scale validation) to fast-track research formulations into GMP-adjacent production profiles — a clear value proposition for cell therapy and biologics customers.

-

Commercial model refinement: Reassess pricing and bundling strategies. Value-based pricing for reproducibility, documentation and support services will win in complex procurements; subscription or managed-service models for media plus process support are emerging as durable monetization paths.

-

M&A and partnership playbook: Use focused M&A to acquire niche media expertise (e.g., stem cell or primary cell media) and to shore up raw material or analytical capabilities. Partnerships with instrument and consumable players can also create defensible integrated workflows.

Competitive landscape — what leaders and challengers are doing

The market combines global life-science titans and specialized niche players. Leading incumbents maintain breadth across basal, serum-free and defined media portfolios and pair product depth with global manufacturing footprints, technical support and robust quality systems. Emerging and specialized firms differentiate via vertical focus, application-specific optimization and rapid product iteration.

-

Thermo Fisher Scientific leverages its Gibco franchise to cover classical, serum-free and chemically defined media for a wide array of mammalian and stem-cell workflows; recent kit launches aimed at CHO line development and next-generation chemically defined formulations underscore a dual strategy of broad market coverage plus productivity-enhancing novelties.

-

Merck KGaA (MilliporeSigma) combines a wide reagent and supplement catalog with media offerings that aim to balance consistency and breadth, serving primary cell research through to bioprocessing pilot work, with a strong emphasis on quality and reproducibility.

-

Corning Incorporated ties media formulations to proprietary cultureware strategies, offering integrated lab-level solutions for mammalian cell growth that appeal to core research labs where workflow convenience is valued.

-

Cytiva (Danaher) markets HyClone media and feeds with explicit scalability narratives, positioning products as research-to-production-friendly options — a message that resonates with bioprocess teams planning technology transfer.

-

Lonza Group is expanding capability beyond off-the-shelf media via media development services and lab assets, as evidenced by recent launches of media optimization facilities aimed at enabling custom, scalable formulations for therapeutics development.

-

Sartorius, FUJIFILM Irvine Scientific, STEMCELL Technologies and several specialized vendors differentiate on factors such as animal-free components, stem-cell optimization, and organoid support media — positioning that attracts translational and academic niches.

-

Regional and cost-focused players (e.g., certain firms serving emerging markets) compete on price and accessibility, serving a large base of cost-sensitive research labs — an important demand pool for classical media offerings.

Recent market activity underlines these dynamics: new product launches targeting CHO productivity and E. coli biomanufacturing research, the introduction of integrated cell expansion systems with in-line monitoring, and the opening of media development laboratories in strategic geographies are all tangible signs of providers aligning R&D and operations to translational demand.

What PW Consulting’s full report delivers (practical, operational content)

The full report is structured to turn market data into executable plans. It contains:

-

A robust, transparent market model with scenario capabilities (baseline, adoption-acceleration and downside supply-disruption scenarios) so teams can stress-test investment cases;

-

A supplier scorecard that evaluates manufacturing footprint, raw-material governance, documentation strength, product breadth and route-to-scale capabilities — suitable for procurement and BD prioritization;

-

Actionable go-to-market playbooks tailored to incumbents, mid-tier specialists and regional challengers, including suggested product roadmaps, commercial bundles and channel strategies;

-

M&A and partnership screening tools that identify candidate targets by capability gaps and cultural fit, supported by a prioritized 12–18 month integration checklist;

-

A risk-heatmap focusing on raw-material volatility, FBS scarcity risk, regulatory qualification needs and single-source vulnerabilities, accompanied by mitigations and procurement scorecards;

-

Appendices with modeled elasticity curves, unit-cost sensitivity analyses and the full dataset of time-series market size estimates by year and high-level segment — available only in the full report to preserve commercial sensitivity.

Note: this preview omits detailed regional and sub-segment tables; the full report provides these granular breakdowns, downloadable datasets, and an interactive model for client customization.

How to use the intelligence in your 2026 planning cycle

-

Re-allocate R&D spend toward chemically defined and serum-free formulations in markets where translational demand intersects with reproducibility requirements; prioritize quick-win verticals where clinical translation timelines shorten payback periods.

-

Formalize a raw-material strategy that blends long-term supplier agreements, qualified second sources and inventory policies for critical components. Build chain-of-custody documentation into product packaging and technical files.

-

Develop qualification accelerators — standardized protocols and documentation templates — to shorten customer qualification cycles for RUO products moving toward therapeutic or diagnostic use.

-

Pilot integrated offerings (media + analytics + process support) with select customers to test subscription and managed-service pricing models. Capture learnings on willingness-to-pay for traceability and documentation.

-

Use the report’s M&A screens to identify bolt-on acquisitions that bring niche expertise (e.g., stem-cell media, primary cell formulations) or analytical capabilities (e.g., traceability software, low-volume GMP manufacturing).

Final note — the strategic value proposition

For 2026, the strategic advantage will belong to organizations that convert product science into procurement defensibility. Companies that can assure reproducibility, document lineage, and deliver scalable media solutions stand to capture premium share in translational research and early bioprocessing. PW Consulting’s full Cell Culture Media for Research report is built to help teams make those choices with confidence — offering the modeling, supplier intelligence and operational playbooks needed to translate market signals into prioritized actions. To review the complete datasets, supplier scorecards and scenario model, consult the full report on our website or contact PW Consulting for a tailored briefing.

For detailed analysis of this topic, please visit the official page: Cell Culture Media For Research Market

Lacy Lee

Senior Marketing Manager

sales@pmarketresearch.com

00852-95632430

PW Consulting: www.pmarketresearch.com

Tags

PW Consulting

The Best-reviewed Subdivided Market Risk Analysis Firm in the US and East Asia.