PW Consulting: Wireless WAN Solutions Market Set to Surge at a 14.48% CAGR, Signaling Major Growth Opportunity

Wireless WAN Solutions Market: Strategic Intelligence Briefing for 2026 Decision-Makers

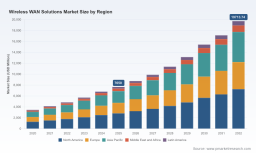

PW Consulting is pleased to release an executive briefing extracted from our comprehensive Wireless WAN Solutions Market report. As enterprises plan budgets, partner strategies, and network roadmaps for 2026, they face rapid technology shifts, tighter regulatory guardrails, and a vendor landscape consolidating around a handful of global players. Our analysis projects the global wireless WAN market to grow from USD 7,650.0 Million in 2025 to USD 8,727.0 Million in 2026, tracking a compound annual growth rate (CAGR) of 14.48% over the forecast window — and further accelerating toward a multi-billion-dollar market by 2032. This briefing highlights the practical, decision-ready insights the full report delivers while intentionally withholding certain proprietary subsegment figures to preserve the value of the source report.

Wireless Wan Solutions Market

Why this report matters for 2026 planning

- Actionability: We translate macro growth signals into concrete vendor selection criteria, procurement levers, and deployment phasing suitable for enterprise and service-provider buyers.

- Timing: 2026 is a hinge year—transitioning from early 5G rollouts and SD-WAN maturity to production-grade private networks, edge integration, and new low-latency use cases. The report maps when specific capabilities become commercially and operationally viable.

- Risk-aware guidance: We integrate regulatory shifts and export controls into sourcing strategies, helping CIOs avoid costly compliance surprises and supplier de-risking missteps.

Market trajectory and underlying drivers

The wireless WAN market is in a sustained growth phase driven by three converging forces: broad 5G network maturity, systemic adoption of hybrid WAN architectures, and the rising business case for distributed compute and private wireless in industries such as logistics, manufacturing, retail, and public safety. Our top-line projection—USD 7.65 billion in 2025 growing to USD 8.727 billion in 2026 at a 14.48% CAGR—reflects steady enterprise migrations from single-access LTE to multi-access strategies that combine public 5G, private 5G, and SD-WAN overlays.

Wireless Wan Solutions Market

Market concentration indicates that incumbents and scale vendors still command significant share: the three largest vendors represent nearly half the market (CR3 = 48.5%), while the five-largest capture more than three-fifths (CR5 = 62.3%). That concentration shapes procurement dynamics—buyers can choose from well-established global stacks or pursue specialized niche suppliers for differentiated needs.

Wireless Wan Solutions Market

Practical contents of the full PW Consulting report

- Executive decision frameworks: Ready-to-use checklists for network owners and procurement teams to evaluate vendors across security, performance SLAs, manageability, and total cost of ownership (TCO) models.

- Technology roadmaps: Comparative timelines for 5G standalone (SA), 5G Advanced capabilities, LTE fallback strategies, and SD-WAN integration patterns, including recommended pilot-to-scale pathways.

- Operational playbooks: Templates for site surveys, spectrum assessment, small cell and backhaul planning, and end-to-end testing procedures designed to shorten time-to-benefit and reduce rollout rework.

- Commercial models: Guidance on capex vs. opex sizing, multi-year service contracts, and pricing negotiation levers for blended public/private connectivity and managed service alternatives.

- Regulatory and supply-chain annexes: Impact assessments and mitigation strategies covering mid-band spectrum changes, export controls, and regional network-neutrality obligations.

- Vendor evaluation matrix: A structured scoring model that balances technical capability, ecosystem reach, operational maturity, and regulatory hygiene—used to produce bespoke shortlists for buyers.

Note: The complete report includes detailed subsegment data and supplier benchmarking tables. This briefing intentionally omits those proprietary splits to preserve the strategic value of the full findings.

Competitive landscape: how vendors are positioning for enterprise adoption

The vendor ecosystem spans network infrastructure incumbents, specialist routing appliance makers, mobile network operators (MNOs), and software-centric SD-WAN/virtualization players. Below we summarize how leading firms are shaping solutions relevant to enterprise wireless WAN programs.

- Cisco Systems (San Jose, CA) — Cisco rounds hardware (including ruggedized industrial routers) with SD-WAN orchestration and a strong services practice. Recent product refreshes emphasize 5G sub-6GHz support for industrial edge deployments, strengthening Cisco’s play for distributed enterprise sites requiring hardened connectivity and integrated management.

- Ericsson (Stockholm, Sweden) — Ericsson remains focused on radio and core capabilities, with recent launches targeting connectivity for reduced-capability IoT devices and expanded RAN options. Their emphasis on scalable RAN and core services positions them as a key infrastructure partner for large private and hybrid public-private wireless WAN projects.

- Huawei Technologies (Shenzhen, China) — Huawei continues to supply end-to-end 5G base stations, routers, and SD-WAN appliances globally where regulatory conditions permit. Enterprises should weigh vendor benefits against regional export and procurement constraints when considering Huawei-based solutions.

- Nokia (Espoo, Finland) — Nokia’s portfolio spans AirScale RAN and carrier-grade routing for backhaul and edge. Network deployments of 5G standalone cores enhance Nokia’s ability to support capacity-intensive wireless WAN use cases and managed network offerings.

- Verizon Communications & T-Mobile US (U.S. MNOs) — Carrier players are extending public 5G capabilities with private networking options, low-latency URLLC support, and dedicated slices for enterprise applications. Recent protocol activations and mmWave expansions materially change the calculus for urban and industrial deployments.

- Pepwave (Hong Kong) — As a specialist in multi-WAN bonding routers, Pepwave is favored for resilient site-level connectivity and rapid failover. Their appliances are practical choices for retail, branch, and mobile sites where continuous connectivity is mission-critical.

- VMware (Broadcom) (Palo Alto, CA) — VMware’s SD-WAN controls and cloud-native orchestration enable hybrid WAN architectures with cellular uplinks. Their strength is in overlay management and policy-driven orchestration, making them a frequent partner in multi-vendor deployments.

- Other MNOs and regional specialists — Post-merger entities and regional operators are layering enterprise-focused services onto nationwide 5G footprints; sourcing decisions should consider local coverage, SLAs, and integration ease.

Recent vendor moves underscore the pace of change: major vendors launched 5G Advanced features and expanded 5G SA deployments through 2024–2025, and several carriers broadened mmWave and URLLC support. Buyers should treat vendor roadmaps as a dynamic input to contract terms and pilot scopes.

Regulatory, cost and operational considerations that will shape procurement

- Spectrum and market rules: Mid-band allocations and national spectrum auctions materially affect capacity planning. Mandates such as network neutrality in certain jurisdictions require contract language and traffic-management transparency.

- Export and supply restrictions: Controls on cryptographic components and export licensing can impede deployment timelines for some suppliers—procurement teams must include compliance clauses and alternative-sourcing contingencies.

- Infrastructure cost drivers: Small-cell densification and backhaul add non-trivial per-site costs; our field models and site cost sensitivity analysis help forecast deployment budgets and prioritization.

- Standards evolution: 3GPP releases continue to add mission-critical and IoT features. Procurement timelines should align with both vendor roadmap maturity and target use-case readiness (e.g., URLLC for remote control or robotics).

Actionable playbook for 2026

- Prioritize pilots by business value, not technology. Select 2–3 high-value sites for private or hybrid 5G proof-of-value aligned to measurable KPIs (throughput, latency, availability, and operational cost).

- Adopt a layered sourcing strategy: combine at least one global infrastructure partner, a specialist appliance vendor for site resilience, and an orchestration/SASE/SD-WAN provider for policy control and security.

- Embed compliance and exit clauses up front. Require hardware/software escrow, alternative firmware compatibility, and clear export/ITAR controls to mitigate geopolitical supply shocks.

- Use staged commercial models: start with managed or consumption-based offerings to lower initial capex, then switch to owned assets once traffic and performance economics are proven.

- Design for interoperability and observability: mandate open APIs, telemetry outputs, and standardized performance benchmarks in RFPs to ease multi-vendor orchestration.

Near-term risks and signposts to monitor

- Regulatory shifts around spectrum allocation and network neutrality that could change competitive dynamics and pricing.

- Supply-chain disruptions tied to export controls or component shortages, which could delay hardware refresh cycles.

- Standards adoption lag—commercial availability of some advanced 5G features may trail initial vendor announcements, impacting timelines for latency-sensitive use cases.

PW Consulting’s full Wireless WAN Solutions Market report provides the quantitative underpinnings, ready-to-use procurement templates, and vendor scorecards that enterprise and service provider teams need to convert these insights into action. This briefing offers a strategic orientation and operational checklist for 2026 planning; the full study contains the detailed subsegment analytics and vendor benchmarks that will inform final vendor shortlists and budget approvals.

Next steps

- Request the full report to access the proprietary subsegment tables, supplier matrices, and the customizable vendor-scoring tool.

- Schedule a PW Consulting strategy session to translate market projections into a bespoke pilot roadmap and commercial negotiation plan for your organization.

PW Consulting — helping you align network strategy with business outcomes in a rapidly evolving wireless WAN landscape.

For detailed analysis of this topic, please visit the official page: Wireless Wan Solutions Market

Lacy Lee

Senior Marketing Manager

sales@pmarketresearch.com

00852-95632430

PW Consulting: www.pmarketresearch.com

Tags

PW Consulting

The Best-reviewed Subdivided Market Risk Analysis Firm in the US and East Asia.