PW Consulting: Ion Chromatography Column Market to Rise from USD 512.5 Million in 2025 to USD 833.8 Million by 2032 at a 7.24% CAGR — Anion Exchange and North America Lead the Way

Ion Chromatography Column Market: Strategic Briefing for 2026 Decision-Makers

PW Consulting’s latest market study on the Ion Chromatography (IC) Column market provides a focused, operationally actionable intelligence package tailored for executives, corporate strategists, and investors preparing for 2026. The IC column market has moved from niche laboratory consumable to a strategically important component of regulated testing workflows across environmental monitoring, pharmaceuticals, food safety and industrial process control. Our analysis synthesizes historical momentum, regulatory inflection points, supplier economics and competitive positioning into a concise set of decisions that matter this year — while reserving granular segmentation data for subscribers who require executable numbers and supplier-level playbooks.

Ion Chromatography Column Market

Why 2026 is a Strategic Inflection Point

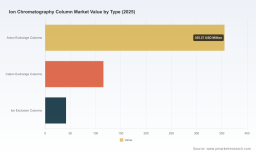

Between 2020 and 2025 the global market expanded steadily (from approximately USD 365 million to USD 512.5 million), reflecting rising demand for regulated testing and the broader adoption of IC techniques in routine laboratories. Our forecast horizon (2026–2032) models continued expansion at a compound annual growth rate (CAGR) of 7.24%, lifting total market value to roughly USD 834 million by 2032. That trajectory — underpinned by regulatory adoption, instrument automation, and growing end‑market complexity — signals a shift from volume-driven competition to value-driven strategies: suppliers that can bundle differentiated columns with compliant software, service programs and workflow automation will capture premium margins.

Ion Chromatography Column Market

What the Report Delivers (Practical, Actionable Content)

- Market sizing and forecast framework: historical baseline (2020–2025) and scenario-based projections (2026–2032) calibrated to demand drivers and macroeconomic sensitivity.

- Regulatory and standards playbook: how EPA, USP/USP-NF modernization and 21 CFR Part 11 expectations reshape buyer requirements for columns, consumables and instrument software.

- Competitive diagnostic: comparative profiles of incumbent leaders and fast followers, channel strategies, service models and R&D positioning.

- Commercial playbooks for manufacturers and distributors: pricing architecture, aftermarket capture, guard-column economics and field service models that preserve long-term margin.

- Technology and product roadmaps: prioritization of polymer-based media, high-capacity exchange chemistries, and compatibility strategies for compact automated IC platforms.

- Supply chain, manufacturing and cost-to-serve analysis: risk maps for raw materials, lead-times, and localization strategies that reduce exposure while protecting IP.

- M&A and partnership screening: value drivers, target archetypes and integration checklists for inorganic growth.

- Buyer behavior and procurement playbook: tender structures, specification clauses, and validation expectations that procurement teams will use in 2026 tenders.

Competitive Landscape: Strategic Implications

The IC column market exhibits a consolidated structure: the top three suppliers collectively command a dominant portion of the market, and the top five further increase concentration. This consolidation reflects both the high value of instrument‑compatible consumable ecosystems and the barriers created by validated methods and regulatory acceptance. For corporate strategists, this means two pathways to scale: (1) build a differentiated platform integrated with instrument and software ecosystems, or (2) pursue cost leadership plus channel intimacy in regional or price-sensitive segments.

Ion Chromatography Column Market

- Thermo Fisher Scientific — With the Dionex IonPac and CarboPac portfolios, Thermo Fisher has the breadth to serve high-value regulated workflows (anion/cation exchange, specialty eluents). Strategy: defend instrument-linked consumable lock-in by deepening application support and expanding validated method libraries.

- Metrohm AG — Metrohm’s long tenure in IC and explicit compliance to standards used for regulatory water analysis makes it a go‑to for laboratories needing validated workflows. Strategy: leverage regulatory pedigree to sell turnkey solutions and managed services for environmental and compliance labs.

- Shimadzu Corporation — Shimadzu’s development of compact, fully automated systems (e.g., the Nexera IC family) targets efficiency-seeking customers. Strategy: couple compact instruments with consumable subscription models and fast‑start validation packages for municipal and industrial water testing customers.

- Agilent Technologies — As part of a broader LC/HPLC consumables portfolio, Agilent can cross-sell into pharmaceutical and food labs. Strategy: exploit cross-platform purchasing to grow share in laboratories standardizing on one vendor for multiple separations techniques.

- SHINE (Qingdao Shenghan) — A mass-manufacturer with a patent portfolio, SHINE is strategically positioned to compete on cost and scale. Strategy: target emerging markets and large-volume customers with local service partnerships and IP-backed product differentiation.

- Shodex, Tosoh, Bio‑Rad, GL Sciences — These suppliers bring specialized media, decades of chromatographic expertise, and niche product differentiation. Strategy: maintain premium positioning through polymer and media innovation, while exploring alliances with instrument OEMs to expand addressable demand.

Recent product and catalog actions reinforce these strategic plays: Shimadzu’s 2026 introduction of a compact Nexera IC instrument accelerates the automation-led segment; Metrohm and Shodex catalog updates in 2025 demonstrate suppliers continuing to expand validated offerings and accessory ecosystems. These moves signal that 2026 procurement decisions will increasingly favor integrated packages that reduce method-transfer risk and validation burden.

Regulatory Dynamics: From Technical Requirement to Commercial Lever

Regulatory acceptance (including USP-NF modernization, EPA methods and 21 CFR Part 11 compliance) has elevated IC from a technical option to a required technique in specific assays and testing regimes. Buyers now evaluate suppliers through a regulatory lens: validated methods, compliant software and auditable traceability are procurement gatekeepers. Suppliers unable to demonstrate regulatory alignment face longer sales cycles and higher validation costs for customers.

Strategic Recommendations for 2026

- For OEMs and Tier‑1 Suppliers: Prioritize integrated solutions that combine columns, consumables, compliant software and remote diagnostics. Premium customers will pay for reduced validation risk and faster time-to-results.

- For Mid‑tier & Regional Players: Double down on channel partnerships and local service capability. Competitive advantage will come from shorter lead times, localized validation packages and flexible commercial terms.

- For New Entrants & Contract Manufacturers: Focus on specific value pockets — e.g., high-throughput environmental testing or price-sensitive reagent exchanges — and secure IP or quality certifications that enable entry into regulated tenders.

- For Distributors & Laboratories: Reassess procurement specifications to include total cost of ownership metrics (consumable yield, guard-cycle economics, validation support) rather than unit price alone.

- For Investors & M&A Teams: Target assets that expand consumable ecosystems or add regulatory-compliant software/IP. Look for acquisition targets that can lock in recurring annuity revenue from consumable replenishment and service contracts.

Operational Playbooks: From Procurement to Field Service

Executives need concrete steps to translate strategic priorities into operational gains. Our report outlines playbooks covering:

- Procurement specifications that accelerate approval in regulated labs and shorten RFQ cycles;

- Service and consumable bundling approaches that increase attach rates and reduce churn;

- Quality and manufacturing controls that mitigate supply interruption risks and protect margin during demand spikes;

- Commercial KPIs for consumables (lifetime yield per column, guard‑column economics, validation time) to align sales and R&D incentives;

- Digital lab enablement — data integrity workflows, remote diagnostics and subscription billing models — that create recurring revenue while improving customer retention.

Risks and Contingencies

Key downside risks for 2026 strategy include raw material cost volatility, accelerated price-based competition from low-cost manufacturers and slower-than-expected regulatory adoption in certain geographies. We model stress scenarios and provide mitigation options — from dual-sourcing strategies to flexible manufacturing and value-added service ramps — so leadership teams can choose calibrated responses rather than reactive cuts.

Call to Action: Where to Find the Full Playbook

This briefing is designed as a strategic “trailer”: it highlights the evidence-based vectors that will determine market winners in 2026, and the operational levers executives must pull. For clients and stakeholders seeking the full intelligence — including detailed segmentation by region, application and product type, company-level revenue estimates, and executable M&A screening tools — PW Consulting’s full Ion Chromatography Column Market report provides the proprietary datasets and supplier-specific playbooks needed to act decisively.

Contact PW Consulting or visit our report page to access the comprehensive dataset, scenario models and tailored advisory packages that will convert this market trend into a competitive advantage in 2026.

For detailed analysis of this topic, please visit the official page: Ion Chromatography Column Market

Lacy Lee

Senior Marketing Manager

sales@pmarketresearch.com

00852-95632430

PW Consulting: www.pmarketresearch.com

Tags

PW Consulting

The Best-reviewed Subdivided Market Risk Analysis Firm in the US and East Asia.