PW Consulting: Smoke Evacuation Tubing Market to Reach USD 380.4 Million by 2032, Growing at a 7.12% CAGR

PW Consulting: Strategic Preview — Smoke Evacuation Tubing Market 2026 Playbook

PW Consulting today releases a strategic preview of our forthcoming Smoke Evacuation Tubing Market report — an operational guide designed to inform executive decisions in 2026. Built on a 2020–2025 historical base and a detailed 2026–2032 forecast, the study quantifies a market that stood at USD 235.05 Million in 2025 and is modeled to expand at a 7.12% compound annual growth rate into the forecast window, reaching roughly USD 380.4 Million by 2032. This briefing highlights why those topline dynamics matter, the practical outputs contained in the full study, and the tactical choices healthcare providers, device OEMs, and investors should consider as they plan for 2026. For the full dataset, breakout tables, and downloadable models, please consult the report page referenced at the end of this release.

Smoke Evacuation Tubing Market

Why this market will be strategic in 2026

- Regulatory momentum drives adoption: Emerging statutory requirements and heightened institutional expectations are creating a steady demand floor for smoke-management technologies in operating rooms and procedural suites. Compliance is shifting purchase decisions from discretionary to mandatory in many settings, making smoke evacuation tubing not merely a consumable but a standards-driven procurement category.

- Integration and product innovation are reshaping value: Tubing is no longer a pure commodity. Innovations in materials, tapered corrugated designs for handling and ergonomics, and system-level integration (instrument-level evacuation pathways, integrated pencil adapters, and device-compatible kits) are creating differentiated product families that capture premium pricing and sticky customer relationships.

- Fragmented supplier structure but rising concentration: The market retains a healthy number of specialized suppliers and OEM partners, while the top firms are consolidating share. Our concentration analysis shows meaningful market share at the three- and five-firm levels, indicating both competitive intensity and room for strategic consolidation plays.

What the full report delivers — practical, transaction-ready assets

PW Consulting structured the full report to move from insight to execution. Key deliverables include:

Smoke Evacuation Tubing Market

- Proprietary market-sizing model (2020–2032) with scenario toggles (base, accelerated regulation, cost-constrained adoption) and downloadable Excel workbooks for client customization.

- Interactive decision-support dashboards that map demand drivers against procurement KPIs, enabling hospitals and IDNs to simulate spend and volume under different OR utilization and regulatory enforcement assumptions.

- Segmented go-to-market playbooks for OEMs and contract manufacturers: channel strategies, pricing levers, bundling approaches (tubes + disposables + adapters), and sample contract terms tailored to acute-care systems and ambulatory surgery centers.

- Regulatory and compliance matrix aligned to FDA Class II pathways and state-level mandates, with a checklist for product labeling, biocompatibility documentation, and 510(k) strategy implications for accessory versus system claims.

- M&A & partnership heatmaps identifying attractive target profiles, integration risks, and value-capture levers for buyers seeking to expand product breadth, geography, or distribution reach.

- Supplier scorecards and manufacturing-readiness templates to support insourcing vs. outsourcing decisions, including sterilization logistics, single-use economics, and quality-cost tradeoffs.

- Clinical & OR-acceptance playbook: evidence generation priorities, HCP engagement frameworks, and hospital procurement messaging to accelerate conversion from trial to routine use.

Macro forces shaping 2026 strategy

- Regulatory tailwinds: More than a third of U.S. states have enacted mandates around surgical smoke evacuation, and devices in this class must adhere to FDA Class II requirements under 21 CFR 878.4400. These forces raise the bar for manufacturers on documentation, labeling, and performance claims.

- Product evolution: Market participants are moving beyond single-extrusion tubing to advanced profiles and material formulations that improve flexibility, kink resistance, and user ergonomics. Sterile versus non-sterile positioning and compatibility with high-flow systems are central product-platform decisions.

- Clinical workflow integration: The fastest-adopted offerings are those that minimize friction at the point of care — integrated pencil adapters, valved laparoscopic ports, and pre-configured kits that reduce setup time and leakage risk — creating both clinical and economic value.

- Commercial consolidation: While many specialized suppliers remain active, the top-tier firms account for a meaningful share of the market, making competitive differentiation and scale economies critical to margin retention.

Reading the competitive landscape

The market is occupied by a mix of specialty suppliers, OEM platform players, and system integrators. Our analysis of core participants yields the following archetypes and strategic considerations:

Smoke Evacuation Tubing Market

- Platform integrators (example: Stryker, Medtronic): These firms compete from a systems standpoint, bundling smoke evacuation capability into broader surgical devices and OR platforms. Their advantages include channel access, installed base leverage, and system-level claims. For agile challengers, partnership and interoperability strategies are essential to stay relevant in OR contracts dominated by platform vendors.

- Specialty consumable suppliers (example: CONMED/Buffalo Filter, CLS-Surgimedics, I.C. Medical, DeRoyal, Aspen, CooperSurgical): These companies excel at focused product breadth — a wide range of tubing diameters, sterile options, and procedural accessories. Their competitive strength is product specialization and cost-competitive manufacturing. However, they must continually invest in clinical evidence and supply-chain reliability to defend against platform entrants and private-label threats.

- Value-based suppliers and private-label operators: Organizations with low-cost manufacturing footprints and strong distributor relationships can pressure pricing in commoditizing segments. The defensive play for specialty vendors is to bundle services (training, on-site validation) and to pursue exclusive OR pilots that create switching costs.

Recent regulatory milestones — including an FDA 510(k) clearance for an integrated smoke-evacuation-enabled electrosurgical device in late 2024 — underscore the pace at which devices and tubing are being rationalized into comprehensive surgical solutions. Executives should interpret these signals as both risk and opportunity: risk to standalone tubing margins, opportunity to capture share in bundled procurement agreements.

Strategic scenarios and 2026 playbooks

- Scenario A — Regulatory Acceleration: If legislators and hospital networks increase enforcement, demand shifts quickly toward compliant, documented solutions. Winning playbook: prioritize regulatory completeness, secure hospital system contracts, and accelerate sterile, integrated kit availability.

- Scenario B — Cost-Constrained Providers: In environments with tighter budgets, buyers trade up/down along total-cost-of-ownership lines. Winning playbook: emphasize low-cost, high-availability offerings and flexible contract terms (pay-per-case, volume discounts) to lock in share.

- Scenario C — Technology Convergence: Integrated surgical platforms drive preference for tubing that is certified for compatibility. Winning playbook: pursue OEM partnerships, co-development agreements, and interoperability certification to remain on approved-device lists.

Seven priority actions for executives in 2026

- Develop a bifurcated product strategy: preserve a cost-competitive line for commodity channels while investing in premium, integrated tubing solutions for system-level partnerships.

- Complete a compliance acceleration program: map documentation gaps to FDA Class II requirements now and budget for rapid remediation to avoid procurement disqualifications.

- Pursue targeted OEM collaborations: short-term distribution agreements can accelerate hospital acceptance; longer-term co-development secures design-in on integrated devices.

- Optimize manufacturing & sterilization footprint: run a make-vs.-buy sensitivity on sterilization economics and single-use cost drivers to preserve margins under volume growth scenarios.

- Lock in evidence generation: fund pragmatic clinical studies and hospital pilots that quantify OR time-savings, infection-risk reduction, and staff satisfaction to support premium pricing.

- Explore bolt-on M&A to fill distribution or product gaps: with meaningful top-firm concentration already present, incremental acquisitions that add sterile-capacity or channel access can be value-accretive.

- Design procurement-friendly commercial models: offer bundled kits, sample programs, and contract-level service SLAs to become preferred suppliers in group purchasing organizations and IDNs.

How PW Consulting supports execution

Clients of PW Consulting receive the full market model and tailored workshops that apply the study’s scenarios to their specific business context. Our deliverables are designed to be directly actionable for product roadmap prioritization, legal/regulatory checklists, commercial pilots, and M&A screening. We deliberately structure the package so that strategy teams can move from insight to bid-ready proposals within 8–12 weeks.

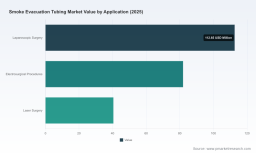

Note on data transparency: This preview highlights top-line market sizing and growth assumptions to frame strategic decision-making. The full report contains the granular segmentation, regional and application breakdowns, supplier market shares, and downloadable Excel models required to operationalize the recommendations contained herein. These detailed breakouts are intentionally reserved for the complete report to ensure clients obtain the full analytical context required for transaction-level decisions.

For access to the complete Smoke Evacuation Tubing Market report, interactive models, and consulting engagement options, please visit the PW Consulting report page or contact your PW Consulting account representative.

For detailed analysis of this topic, please visit the official page: Smoke Evacuation Tubing Market

Lacy Lee

Senior Marketing Manager

sales@pmarketresearch.com

00852-95632430

PW Consulting: www.pmarketresearch.com

Tags

PW Consulting

The Best-reviewed Subdivided Market Risk Analysis Firm in the US and East Asia.