PW Consulting Forecasts Chromatography Columns Market to Rise from USD 3,200 Million in 2025 to USD 4,655 Million by 2032 at 5.5% CAGR (2026–2032)

Chromatography Columns Market 2026: Strategic Imperatives from PW Consulting’s New Industry Brief

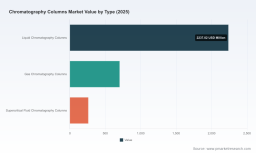

As the chromatography columns market enters the 2026 planning cycle, life‑science procurement leads, product strategy teams, and private‑equity investors face a narrow window to lock in competitive advantage. PW Consulting’s latest market brief—anchored on an expansive historical dataset (2020–2025) and a scenario‑based forecast (2026–2032)—translates market dynamics into actionable choices. Our base‑year valuation for 2025 stands at USD 3.2 billion, with a compound annual growth rate (CAGR) of 5.5% applied across the forecast horizon. Under PW Consulting’s modeling, the addressable market is projected to expand materially through 2032—delivering a compelling growth runway for differentiated technology and supply‑chain plays.

Chromatography Columns Market

Why this brief matters for 2026 decision cycles

-

Macroeconomic clarity at the right cadence: The brief converts historical trends into rigorously stress‑tested forecasts for 2026–2032, enabling teams to move from reactive to prescriptive planning.

Chromatography Columns Market -

Execution‑oriented intelligence: Beyond headline sizing, the study surfaces concrete execution levers—procurement hedges, pricing uplifts, SKU rationalization, and capacity utilization strategies—that deliver near‑term ROI.

Chromatography Columns Market -

Regulatory and trade foresight: The report integrates late‑stage regulatory changes and tariff shocks into commercial playbooks, allowing decision makers to validate 2026 budgets and capex with regulatory realism.

Market trajectory in plain terms

From a post‑pandemic trough to a structurally larger industry, the market moved from the mid‑twenty‑hundreds (USD Million) in 2020 to a USD 3.2 billion base in 2025. Our forecast profile—anchored to a 5.5% CAGR—anticipates sustained expansion driven by continued investment in biopharma analytics, growing regulatory testing requirements, and incremental replacement cycles in laboratories worldwide. The 2026 vintage of forecasts refines risk vectors (supply‑side shocks, trade policy, certification costs) to create three actionable scenarios (base, optimistic, downside) that each come with discrete tactical roadmaps for procurement, product, and M&A teams.

What’s inside the report (practical, operational deliverables)

-

Market sizing and methodology appendix — full transparency on modeling assumptions, elasticities, and scenario inputs.

-

Investment deck for the boardroom — a two‑page executive summary and a 12‑month action plan focused on margin protection and growth capture.

-

Procurement playbook — forward buying strategies, hedging templates for silica and polymer feedstocks, and supplier scorecards tailored to chromatography raw materials.

-

Product portfolio optimizer — prioritization matrix that ranks SKUs by margin resilience, regulatory exposure, and renewal cadence.

-

Pricing and commercial levers — elasticities, list‑to‑net guidance, and channel margin benchmarks to defend profit in a rising‑cost environment.

-

Regulatory & trade risk matrix — practical compliance checklists, labeling templates, and tariff mitigation options for market access.

-

M&A and partnership shortlist — diligence frameworks and a prioritized list of capability gaps best closed by acquisition or JV (process chromatography, membrane solutions, regional manufacturing footholds).

-

Manufacturing & footprint playbook — capex phasing guidance, contract‑manufacturing triggers, and outsourcing thresholds to preserve flexibility.

Competitive landscape: who matters and why

The market is neither a pure commodity nor a winner‑takes‑all arena. PW Consulting’s concentration metrics show a balanced oligopoly: the top three players control a material share of the market, while the top five aggregate a clear majority—creating an environment where scale and differentiated IP both pay. The research canvasses incumbent profiles, recent product and capacity moves, and the strategic implications for competitors and customers alike.

-

Agilent Technologies (Santa Clara, CA) — continues to push UHPLC and bioanalysis performance through new Poroshell and EZ‑guard innovations. Their recent launches signal a sustained investment in guard column ecosystems that lock customers into consumable‑led revenue streams.

-

Thermo Fisher Scientific (Waltham, MA) — expanding proteomics‑grade offerings and premium column platforms, which strengthens their high‑margin consumables franchise tied to instrument ecosystems.

-

Waters Corporation (Milford, MA) — certification wins for flagship chemistries enhance trust with regulated labs and create premium pricing opportunity for validated consumables.

-

Merck KGaA / EMD Millipore (Darmstadt) and Shimadzu (Kyoto) — represent scale in preparative and biopharma segments; watch for bundle strategies that combine columns with method‑validation services.

-

PerkinElmer, Restek, Phenomenex (now part of industry consolidations), Sartorius, and Cytiva — each provide targeted capability that can be aggregated via partnerships or carve‑outs to create full‑stack purification and analytics solutions.

Recent industry moves that change the 2026 playbook

-

Product innovations: Multiple vendors introduced next‑generation UHPLC and proteomics columns in late 2024–2025, raising the bar for resolution and method robustness. These releases accelerate replacement cycles for high‑throughput labs and create cross‑sell windows in service agreements.

-

Capacity investments: Notably, process‑scale column producers expanded capacity for mRNA and biologics purification—an acceleration that compresses lead times but increases capital intensity in the short term.

-

Certification & compliance: Several vendors secured expanded pharmacopeial certifications in 2025, which materially affects adoption in regulated labs and supports price premiums for validated SKUs.

Supply chain and regulatory shocks to factor into 2026 plans

Three structural shocks are particularly relevant to 2026 planning:

-

Raw material cost pressure — silica feedstock has seen a notable price step‑up in the recent cycle, increasing input volatility for column manufacturers. Procurement teams must retool sourcing strategies and evaluate forward contracts or vertical integration options.

-

Regulatory constraint — new chemical restrictions and labeling mandates in key jurisdictions (including restrictive particle‑size rules and consumer‑safety labeling requirements) create compliance costs and may necessitate product reformulation for certain geographies.

-

Trade & transport friction — recent tariff reclassifications and freight surcharges materially alter landed cost economics for imports, shifting the calculus for regional manufacturing vs. cross‑border sourcing.

Strategic implications and recommended 2026 actions

For executives building their 2026 playbooks, PW Consulting recommends a three‑track approach:

-

Defensive: Protect margins by instituting a commodity‑risk program for silica and polymers, re‑negotiating long‑term supply agreements with force‑majeure clarity, and updating pricing governance to capture a portion of raw material inflation.

-

Offensive: Prioritize product upgrades that deliver defensible performance differentials (e.g., bioanalysis and preparative purification), accelerate USP/EP certification where feasible, and deploy premium SKUs into regulated segments to expand ASPs.

-

Structural: Assess selective reshoring or regional manufacturing partnerships to mitigate tariff and freight volatility; evaluate tuck‑in acquisitions that close capability gaps in membranes, single‑use purification, or specialty stationary phases.

What we are intentionally not disclosing here (and why)

In keeping with a “trailer” approach to intelligence, this announcement highlights the report’s practical value while withholding granular regional and application‑level splits, detailed company market shares, and raw tables that underpin our scenario runs. These data elements are intentionally reserved for the full PW Consulting report and the associated downloadable datasets—because these are the assets buyers use to operationalize strategy, execute procurement negotiations, and underwrite transactions.

How to use the full report in 90 days

-

Week 1–2: Executive alignment—use the two‑page investment memo to align the C‑suite on scenario selection and capital allocation priorities.

-

Month 1: Procurement reset—implement the procurement scorecard and begin supplier renegotiations informed by the cost curve appendix.

-

Month 2–3: Go‑to‑market adjustments—deploy SKU rationalization and pricing changes in test markets, and fast‑track certifications that unlock regulated segments.

-

Month 3–6: Strategic transactions—use the M&A shortlist and diligence playbook to evaluate tuck‑ins that accelerate capability building.

Next steps and access

PW Consulting’s Chromatography Columns Market brief is designed to be both a decisioning tool and a launchpad for deeper diligence. If your 2026 resource allocation, procurement, or M&A calendar is already in motion, the full report (including the complete datasets, regional and application splits, and company market share tables) provides the precision inputs you will need. Contact PW Consulting to request the full report and to schedule a tailored briefing with our lead analysts.

In an industry where small changes in chemistry, certification, or supplier footprint can cascade into multi‑point margin swings, the right intelligence—timely, actionable, and execution‑ready—will determine who captures the upside as the market scales into the next decade.

For detailed analysis of this topic, please visit the official page: Chromatography Columns Market

Lacy Lee

Senior Marketing Manager

sales@pmarketresearch.com

00852-95632430

PW Consulting: www.pmarketresearch.com

Tags

PW Consulting

The Best-reviewed Subdivided Market Risk Analysis Firm in the US and East Asia.