PW Consulting: Pathogen Detection Market Poised to Grow at a 7.8% CAGR, New Report Reveals

Pathogen Detection Market — Strategic Briefing for 2026 Decisions

Executive summary

As healthcare systems, food producers, and public-health agencies recalibrate after the pandemic era, pathogen detection remains a strategic priority across diagnostics, food safety, pharmaceuticals, and environmental monitoring. PW Consulting’s latest Pathogen Detection Market report (base year 2025; historical 2020–2025; forecast 2026–2032) provides a pragmatic, decision-focused roadmap for executives planning investments, commercial launches, regulatory strategies, and M&A in 2026.

Pathogen Detection Market

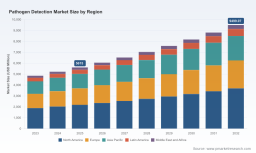

Key macro takeaways that shape near-term strategy: the global market for pathogen detection systems and consumables is forecast to continue expanding at a compound annual growth rate (CAGR) of 7.8% over the 2026–2032 period. Measured on our model, the market expands from a 2025 base of USD 5,615.0 Million to an estimated USD 6,052.97 Million in 2026 and reaches approximately USD 9,499.07 Million by 2032. Concentration metrics indicate a moderately consolidated industry: the top three players account for roughly 38.4% of revenue and the top five for about 52.1%—a structure that favors both platform incumbents and specialist challengers with differentiated assays or channel strategies.

Pathogen Detection Market

Market snapshot and what it implies for 2026

-

Sustained growth with pockets of acceleration — The underlying growth trajectory is robust, driven by ongoing clinical demand, expanded point-of-care (POC) use cases, and increased adoption of multiplex molecular panels. This creates a favorable environment for both incremental product upgrades and selective platform investments.

Pathogen Detection Market -

Platform economics matter — Given the market’s concentration and platform-driven buying patterns, decisions that unlock recurring consumable revenue (assays, reagents, disposables) and consumable-compatible instruments yield the strongest long-term returns. Procurement cycles continue to favor integrated solutions that reduce lab headcount and turnaround time.

-

Regulatory and reimbursement are gating factors — CLIA-waived status remains instrumental for POC adoption; regulatory clarity accelerates hospital and outpatient uptake. Meanwhile, updated reimbursement policies (for example, a revised reimbursement rate for certain pathogen molecular codes effective 2025) materially influence unit economics for tests and instruments and should be included in all 2026 financial models.

-

Input-cost volatility — Supply chain friction and raw material inflation are non-trivial; medical-grade PCR reagents and plastic consumables experienced mid-single-digit to mid-teen percentage cost jumps in recent years. Procurement and manufacturing strategies in 2026 must bake in sustained input-cost risk and supplier diversification.

Actionable implications for executive teams

-

Investment and R&D prioritization — Prioritize R&D that shortens time-to-result for high-throughput settings and that addresses POC usability (CLIA-waived workflows, cartridgeized assays). Investments in multiplexing capability and algorithmic interpretation (to reduce false positives/negatives) will create differentiable value. Build financial scenarios that reflect the 7.8% CAGR baseline and stress-test performance under slower and faster adoption curves.

-

Commercial model and channel strategy — Consider hybrid routes: hospital tenders for high-throughput platforms, distributor partnerships for regional rollouts, and direct models for high-value accounts. Recent strategic distribution moves by major firms underscore the ongoing value of channel partnerships in accelerating hospital access.

-

Regulatory roadmap and go-to-market timing — Securing CLIA-waived or equivalent status should be treated as a strategic milestone for any product targeting physician office or decentralized testing. Regulatory wins and CE/IVD approvals materially shorten sales cycles in certain markets and are often prerequisites for payer coverage.

-

Supply-chain and cost management — Establish durable supplier redundancy and consider vertical integration for key consumables where feasible. Pricing strategies should reflect recent reagent and plastics inflation, and contracts should include clauses to manage commodity-driven cost swings.

-

M&A and partnerships — Look for tuck-ins that broaden panel content, add complementary assay chemistries, or provide access to underserved channels (e.g., food safety, low-resource settings). The market’s mid-level concentration suggests both platform players and specialized asset owners are actively seeking strategic exits or alliances.

What our report delivers — practical, transaction-ready intelligence

-

Market sizing and demand scenarios — A transparent model anchored to the 2025 base year (USD 5,615.0 Million), with conservative, base, and aggressive adoption curves through 2032. The model is provided in an editable spreadsheet so users can test pricing, reimbursement, and adoption sensitivities against the 7.8% CAGR baseline.

-

Commercial playbooks — Go-to-market frameworks for high-throughput laboratory instruments vs. point-of-care platforms, including channel KPIs, tender playbooks, and account prioritization templates that can be deployed immediately by commercial teams.

-

Regulatory and reimbursement roadmaps — Practical checklists and timelines for CLIA-waived submissions and CE/IVD strategies, plus an assessment of how recent reimbursement updates reshape test economics in 2026.

-

Supply-chain risk maps — Supplier concentration heatmaps and contingency plans addressing recent raw-material inflation and lead-time risk, plus benchmarking for manufacturing cost structures.

-

Competitive due diligence tools — Scoring matrices, patent landscape snapshots, and commercial diligence templates tailored to potential M&A targets or partnership candidates.

-

Primary intelligence — Summaries of interviews with laboratory directors, procurement officers, and frontline clinicians that validate assumptions about turnaround-time preferences, POC adoption barriers, and unmet assay needs.

Competitive landscape — how incumbents and challengers are shaping 2026 choices

The market is shaped by a set of well-capitalized instrument-platform incumbents and nimble specialist firms. Our analysis profiles manufacturers that represent the strategic archetypes buyers and investors must consider:

-

Platform incumbents focused on integrated systems and assay ecosystems — Examples include firms that combine throughput-oriented instruments with broad assay menus, positioning them to capture recurring consumable spend and service contracts. Recent product approvals and CE markings from leading platform vendors emphasize continued emphasis on point-of-care iterations and multiplex respiratory/sexually-transmitted infection panels.

-

Rapid POC suppliers and molecular disruptors — Several companies have reinforced their position through distribution deals and assay expansions that improve hospital and outpatient access. These firms demonstrate rapid commercialization playbooks that rely on distribution partnerships and targeted clinical evidence to accelerate uptake.

-

Specialist assay developers — Niche companies delivering isothermal amplification panels, sequencing-based pathogen ID, or mass-spectrometry adjuncts are attractive targets for platform partnerships or acquisition by larger players seeking assay differentiation.

Recent, material vendor moves captured in our intelligence set are instructive for 2026 planning:

- Regulatory approvals and clearances continue to reshape addressable markets—FDA clearances for targeted assays and CE/IVD markings for POC tests shorten time-to-revenue windows for successful applicants.

- Product launches expand multiplexing and syndromic testing options, creating opportunities for cross-selling into existing installed bases.

- Distributor agreements are accelerating hospital deployment and enabling faster scale for innovative platforms.

These developments underscore the importance of aligning regulatory timelines, clinical evidence generation, and commercial partnerships when planning product launches or acquisition integration.

Policy, reimbursement, and supply drivers to monitor in 2026

-

Regulatory policy — CLIA-waived pathways materially affect where and how POC tests can be used; firms targeting primary care and decentralized testing must incorporate this into product design and regulatory spend.

-

Reimbursement shifts — Changes to molecular test fee schedules alter test profitability; recent updates to certain molecular CPT codes and their reimbursement rates should be included in unit-economics models for 2026.

-

Input-cost inflation — Expect continued pressure on reagent and consumable margins; recent reports document a mid-teens increase in some upstream costs. Manufacturers should model cost pass-through strategies and pursue design-for-manufacturability initiatives.

-

Global access initiatives — Expansion of WHO prequalification programs for rapid pathogen tests opens channels into low-resource markets, but requires dedicated evidence packages and pricing strategies that preserve margin in commercial markets.

How to use this report to win in 2026

-

For investors: Use the editable forecast and sensitivity scenarios to stress-test valuation assumptions for target companies and to identify which subsegments warrant premium multiples based on recurring-revenue potential.

-

For product leaders: Leverage the go-to-market playbooks and regulatory timelines to optimize launch sequencing, evidence generation, and pricing strategies to meet 2026 uptake assumptions.

-

For commercial teams: Deploy our account prioritization templates and channel KPIs to shorten sales cycles and accelerate adoption in the most receptive clinical and non-clinical segments.

-

For procurement and operations: Implement the supply-risk maps and cost-scenario templates to stabilize margins and ensure continuity of critical consumables in 2026.

Next steps and how to access full intelligence

This briefing is designed as a strategic “preview” that highlights the most consequential trends and decision levers for 2026. PW Consulting’s full Pathogen Detection Market report contains the granular segmentation, primary-source datasets, and downloadable financial models that underpin the insights summarized here. For teams preparing 2026 budgets, M&A diligence, or product launches, the complete dataset and playbooks will materially shorten time-to-decision and reduce execution risk.

Contact PW Consulting or visit our report landing page to obtain the full report package, model files, and proprietary vendor scorecards required to operationalize a winning strategy in the pathogen detection market.

For detailed analysis of this topic, please visit the official page: Pathogen Detection Market

Lacy Lee

Senior Marketing Manager

sales@pmarketresearch.com

00852-95632430

PW Consulting: www.pmarketresearch.com

Tags

PW Consulting

The Best-reviewed Subdivided Market Risk Analysis Firm in the US and East Asia.