PW Consulting: Polymer Reinforcing Filler Market to Grow at 5.5% CAGR from USD 14,250.6 Million in 2025 to USD 20,730.05 Million by 2032 — Asia Pacific Leads with USD 6,394.04 Million

PW Consulting: Strategic Brief — Polymer Reinforcing Filler Market Outlook and 2026 Playbook

Executive summary

The global polymer reinforcing filler market reached USD 14,250.6 Million in our base year (2025) and is set to expand at a compound annual growth rate (CAGR) of 5.5% over the 2026–2032 forecast window, reaching an estimated USD 20,730.05 Million by 2032. This trajectory reflects a blend of steady end‑market demand (automotive, construction, packaging, industrial goods), incremental substitution toward engineered and specialty fillers, and an accelerating shift to lower‑carbon and circular feedstocks.

Polymer Reinforcing Filler Market

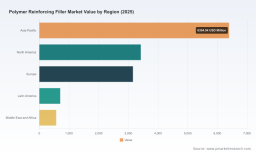

As PW Consulting’s senior strategic and industry analysis team, we prepared this release to outline the practical strategic value our full report delivers to C‑suite and business unit leaders planning for 2026. The synopsis below highlights the actionable implications of macro trends, competitive moves, and regulatory signals — deliberately omitting the granular regional and application splits available in the full report to preserve the “trailer” experience and compel direct access to the comprehensive dataset.

Polymer Reinforcing Filler Market

Why 2026 is a pivotal year for corporate decisions

- Commercialization of circular alternatives: 2025–2026 marks an inflection point where chemically recycled and post‑consumer derived reinforcing fillers have moved from pilot to commercial stages. Select suppliers now offer REACH‑registered recycled reinforcing filler products and partnerships with OEMs and rubber manufacturers are forming.

- Balance of scale and specialization: The market is moderately concentrated (CR3 ≈ 38.5%; CR5 ≈ 52.4%), creating opportunity for both global incumbents to pursue scale‑based moves and nimble specialists to win by differentiation in high‑performance niches.

- Input cost and supply topology: Raw material economics and regional capacity adjustments are reshaping procurement and sourcing strategies. Tactical decisions in 2026 around hedging, localized sourcing, and contract structures will materially affect margins across the planning cycle.

Market dynamics that should guide 2026 planning

- Sustainability as a commercial requirement: New low‑carbon fillers and circular carbons are being adopted by leading polymer compounders and OEMs. Independent lifecycle claims (e.g., significant percentage reductions in cradle‑to‑gate emissions) and regulatory acceptance (REACH registration for chemical recycling outputs) are accelerating customer uptake.

- Premiumization of performance grades: Demand for specialty reinforcing fillers — those engineered for dispersion, thermal stability, flame retardancy, or targeted mechanical enhancement — is growing faster than commodity grades. Investment in surface treatment, nano‑scale morphology control, and coupling agent compatibility is becoming core IP.

- Regional capacity and logistics considerations: Suppliers are expanding capacity in response to regional demand shifts and reshoring of polymer value chains. These capacity moves have direct implications for lead times, freight exposure, and inventory strategies for polymer compounders and converters.

- Cost pressure vs. value capture: While commodity raw material pricing remains an input risk (e.g., recent calcium carbonate pricing signals in North America), suppliers that can demonstrate performance uplift and downstream processing efficiencies can achieve price resiliency.

Competitive landscape — strategic takeaways

Our competitive mapping covers global mineral suppliers, carbon black leaders, specialty engineered‑materials firms, glass fiber producers, and emerging circular technology providers. Recent strategic moves illustrate two parallel playbooks: scale and sustainability.

Polymer Reinforcing Filler Market

- Scale and global footprint (examples): Established players with legacy carbon portfolios and global distribution are expanding both capacity and downstream treatment capabilities to offer higher‑value, specialty grades. They prioritize securing feedstock supply and leveraging long‑term contracts with tire and rubber OEMs.

- Specialty and functional differentiation (examples): Mineral specialists, engineered clay producers, and silica innovators compete on tailored surface chemistries and performance claims — targeting automotive structural polymers, high‑temperature applications, and flame‑retardant compounds.

- Circular entrants and technology integrators (examples): New entrants commercializing recycled reinforcing fillers are positioning on sustainability credentials and carbon intensity advantages, while building validation through partnerships with compounders and OEMs.

Representative corporate signals we analyzed (full sources and chronology in the report): recent acquisitions and capacity announcements from major carbon suppliers; commissioning of post‑treatment and specialty processing lines in Asia; launches of bio‑compatible and recyclable mineral fillers; and REACH registration for chemically recycled filler products. Each of these developments sends a clear strategic message about where customers, regulators, and capital are focusing.

Implications for corporate strategy — seven priorities for 2026

- Embed circularity in product roadmaps: Treat low‑carbon and recycled filler variants as core SKUs for 2026 product launches. Early qualification and co‑development with key customers provide differentiation and protect sales as procurement specifications evolve.

- Invest selectively in specialty chemistries: Prioritize R&D and pilot investments that improve dispersion, reduce processing energy, or enable higher loading without loss of properties. These enable premium pricing and longer customer tenure.

- Reshape procurement and sourcing governance: Move from spot buying to strategic supply agreements that include flexibility clauses, sustainability KPIs, and capacity reservation options — especially in regions where capacity bottlenecks are emerging.

- Evaluate M&A and partnership levers: Target acquisitions that provide surface‑modification capability, recycled feedstock access, or regional processing hubs. Alternatively, structure JVs with chemical recyclers and specialty compounding firms to accelerate market entry with lower capital intensity.

- Reconfigure go‑to‑market and value selling: Train commercial teams to sell total cost of ownership (processing savings, weight reduction, lifecycle advantages) rather than only $/kg commodity metrics. Case studies and validated LCA data will be decisive in negotiations.

- Strengthen regulatory and LCA evidence: Build rigorous life‑cycle analyses, secure relevant registrations/certifications, and pre‑empt increasingly granular ESG procurement requirements.

- Scenario planning for feedstock volatility: Develop playbooks for rapid cost pass‑through, short‑term substitution, and prioritized allocation for high‑margin accounts under constrained supply scenarios.

Practical content in the full PW Consulting report

Our full market research report is structured to be immediately actionable for business planning and contains:

- Detailed market sizing (historical 2020–2025 and forecast 2026–2032) and model assumptions to stress‑test growth scenarios;

- Segmented demand analyses with unit economics across product types and applications, with sensitivity tables that show margin impact under different raw‑material and pricing scenarios;

- Granular competitive profiles, capability maps, and a proprietary consolidation score to evaluate acquisition targets and partnership fit;

- Supply chain and capacity tracker with production investments and announced expansions, plus our assessment of regional risk factors;

- Commercial playbook templates for procurement, product development, and sustainability positioning — including templated contract language and KPI frameworks;

- Case studies illustrating successful commercialization of circular fillers and high‑value specialty products, with measurable outcomes (processing, weight, TCO, emissions).

Note: To preserve the strategic utility of the report as a purchasable deliverable, this press brief intentionally excludes the granular regional and application breakdowns and the detailed financial tables that appear in the full document.

How to use these insights in 2026 business planning

- Board and investor communications: Integrate the market’s growth trajectory and competitive consolidation indicators into capital allocation narratives to justify R&D investment or M&A activity.

- Product and technology roadmaps: Prioritize development cycles that align with validated customer trials for circular fillers and high‑performance grades during the next 12–18 months.

- Supply and procurement planning: Reassess supplier scorecards to include sustainability credentials, capacity commitment terms, and lead‑time responsiveness as non‑price criteria.

- Sales and commercial enablement: Deploy TCO calculators and LCA summaries to substantiate premium positioning during contract renewals and new account acquisition.

Conclusion — the strategic window for decisive action

The polymer reinforcing filler market presents a classical strategy inflection: steady macro expansion (5.5% CAGR through 2032) combined with disruptive supply‑side developments in circular technologies and specialty materials. Companies that move in 2026 to align commercial strategy, product engineering, and procurement with these structural shifts will secure differentiated margin pools and stronger customer lock‑in.

PW Consulting’s full report provides the empirical backbone, scenario tools, and executable playbooks required to convert these high‑level findings into board‑level decisions and operational action plans. For companies crafting their 2026 investment and go‑to‑market priorities, our analysis translates market momentum into concrete next steps — from partner selection and M&A screening to product qualification roadmaps and contractual safeguards.

Access and next steps

For the complete dataset, regional and application breakdowns, company‑by‑company capability matrices, and the downloadable scenario model, please visit the PW Consulting report page. The full report contains the granular tables and operational checklists executives and functional leaders will need to finalize 2026 budgets and strategic initiatives.

For detailed analysis of this topic, please visit the official page: Polymer Reinforcing Filler Market

Lacy Lee

Senior Marketing Manager

sales@pmarketresearch.com

00852-95632430

PW Consulting: www.pmarketresearch.com

Tags

PW Consulting

The Best-reviewed Subdivided Market Risk Analysis Firm in the US and East Asia.