PW Consulting: Boc L‑Leucine Market Poised for 7.45% CAGR During 2026–2032, Report Finds

Boc-L-Leucine Market — Strategic Briefing (PW Consulting, 2026)

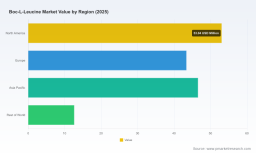

PW Consulting’s new Boc-L-Leucine Market report (base year 2025; historical coverage 2020–2025; forecast period 2026–2032) delivers the commercial intelligence senior executives need to make high‑stakes sourcing, R&D and M&A decisions in 2026. Our bottom‑up market model values the global Boc‑L‑Leucine market at USD 155.6 Million in 2025 and projects growth to approximately USD 257.3 Million by 2032, implying a compound annual growth rate of 7.45% across the forecast window. These topline dynamics, coupled with near‑term input‑cost volatility and structural shifts in peptide chemistry demand, create a decision window for buyers, manufacturers and investors that this report is explicitly designed to inform.

Boc L Leucine Market

What the report contains — practical modules for corporate decision makers

- Market sizing & forecast: Annualized market values from 2020 through 2032 (USD, revenue unit: Million), with transparent methodology, sensitivity checks and scenario variants for policy and trade disruptions.

- Demand drivers and application pathways: Granular discussion of the forces driving uptake in pharmaceutical synthesis, peptide research and broader biotech applications, including adoption cycles for protected intermediates such as Boc‑protected amino acids.

- Supply‑chain mapping: End‑to‑end analysis of raw material flows, including the L‑Leucine upstream chain, contract manufacturing patterns and distribution channels for research vs. commercial scale supply.

- Pricing & cost stack modelling: Forward-looking price scenarios incorporating raw‑material input swings, contract structures (spot vs. long‑term), freight trends and regulatory compliance costs.

- Supplier benchmarking & procurement playbook: Comparative scorecards for manufacturers and distributors, negotiation frameworks, and decision trees for single‑ vs. multi‑sourcing and near‑shoring.

- Quality, regulatory and compliance advisory: Checklist and gap analysis for ISO and pharmacopeial requirements; compliance strategies for customers who require traceable, pharma‑grade intermediates.

- M&A and strategic investment guidance: Valuation heuristics for bolt‑on acquisitions, integration risk matrices and case studies showing value capture pathways.

- Risk and scenario planning: Playbooks for demand shocks, ingredient shortages and logistics disruptions including recommended inventory buffers and contractual mitigants.

Why this report matters for 2026 decisions

The next 18 months will determine which suppliers and end‑users secure advantaged positions in the Boc‑L‑Leucine value chain. Two structural themes dominate:

Boc L Leucine Market

- Upstream raw‑material tightness: Boc‑protection chemistry depends on L‑Leucine as the primary feedstock. The underlying L‑Leucine market was valued in the range of USD 1.20–1.52 billion in 2025, with fermentation‑based supply dominating high‑purity grades used for protected derivatives. Volatility in upstream amino‑acid pricing directly amplifies volatility in Boc‑L‑Leucine economics.

- Quality and regulatory premium: Pharmaceutical‑grade inputs command meaningful price premiums relative to technical or feed grades due to testing and documentation requirements. Buyers trading at the wrong quality level incur downstream rework, regulatory risk and commercial delays.

Overlay these structural themes with near‑term market movements — for example, US amino‑acid pricing spikes observed in early 2026 — and the commercial implications are clear: procurement strategy, supplier qualification and inventory policy are high‑impact levers for 2026 P&Ls.

Boc L Leucine Market

Data‑driven implications (what CFOs and supply‑chain heads should act on)

- Hedge for input spikes: In March 2026, US amino‑acid prices rose sharply due to logistical constraints and cargo tightness. Organizations that aligned purchasing strategies (longer contracts, indexed pricing and strategic inventory) reduced margin erosion; those that remained spot‑exposed faced meaningful cost pressure.

- Assess quality vs. cost tradeoffs: Pharma‑grade L‑Leucine routinely carries a material premium over feed‑grade equivalents. For firms engaged in regulated peptide manufacture, the delta is justified; for preclinical or certain research uses, alternative sourcing or downgraded specifications can be viable — but only with documented risk controls.

- Consider upstream integration: Given fermentation’s dominance in high‑purity amino‑acid supply, selective vertical moves — JV with a fermentation producer, tolling agreements, or strategic offtakes — can insulate producers of Boc‑protected derivatives from raw‑material swings.

- Scenario‑proof commercial plans: Our forecast baseline (CAGR 7.45% to 2032) masks important upside and downside scenarios. Commercial teams should stress‑test product launch and pricing plans across these variants prior to capital commitments.

Competitive landscape — profiles and strategic takeaways

The Boc‑L‑Leucine ecosystem is a mix of large fine‑chemicals manufacturers, specialised peptide‑chemistry suppliers and distribution partners with global reach. The market is best characterised as moderately fragmented: several established suppliers hold entrenched positions in either bulk or research channels, while a wider set of regional manufacturers and distributors serve niche and lab segments. Below we summarise the leading participants and what they imply for counterparties.

- Fengchen Group Co., Ltd. (China) — A large Chinese manufacturer offering Boc‑L‑Leucine BP/EP/USP‑grade as high‑purity powder. Strengths: scale in bulk production, vertical distribution capabilities and established export channels. For buyers: consider long‑term supply contracts and quality audits to secure competitive pricing.

- Hangzhou Leap Chem Co., Ltd. (China) — Specialist producer providing custom and wholesale quantities tailored for peptide applications. Strengths: flexibility and customisation. For users: attractive for development‑stage projects requiring bespoke pack sizes or small‑batch synthesis support.

- Wuhan Fortuna Chemical Co., Ltd. (China) — Focused on wholesale and bulk supply for chemical synthesis and pharmaceutical use. Strengths: commodity‑scale sourcing; suitable for commercial‑scale customers prioritising cost over boutique services.

- Sinochem Nanjing Corporation (China) — Industrial manufacturer supplying Boc‑L‑Leucine with robust quality protocols. Strengths: large infrastructure and compliance capabilities; strategic partner for customers seeking reliable industrial supply.

- BLD Pharmatech (China) — Positioned for high‑purity research channels, with distribution via major scientific platforms. Strengths: brand recognition among lab buyers and distribution networks useful for geographic reach.

- TCI Chemicals (Japan) — Established fine‑chemicals firm offering monohydrate variants for research and synthesis. Strengths: reputation for consistent quality and documentation, attractive for regulated users requiring traceable imports.

- Biosynth (Switzerland/UK) — Supplier of Boc‑Leucine used in peptide hormone intermediates. Strengths: strong European presence and regulatory familiarity for clinical and commercial peptide projects.

- Central Drug House (CDH) (India) — ISO‑certified manufacturer and exporter serving laboratory and fine chemical markets. Strengths: cost competitiveness and export experience, yet buyers should validate certification scope for pharmaceutical supply.

- Chem‑Impex International & Peptide.com (AAPPTec) (USA) — US‑based providers focused on peptide research reagents and smaller lot sizes. Strengths: rapid domestic fulfilment and US regulatory familiarity — useful for time‑sensitive R&D procurement.

Strategic takeaway: select suppliers based on three primary axes — quality & documentation, scale & cost, and agility & customer‑support. The optimal portfolio often combines a bulk, cost‑efficient partner with one or two specialised suppliers for development and regulated production.

Actionable recommendations for 2026

- Rebalance sourcing strategy: Move from purely spot procurement to a blended approach (strategic long‑term contracts + short‑term spot) to capture upside while controlling downside from input volatility.

- Qualify 2–3 tier‑one suppliers: Perform technical audits, request pharmacopeial test data and negotiate tiered pricing linked to volume and quality thresholds.

- Pursue upstream optionality: Evaluate partnerships or offtake agreements with fermentation‑based L‑Leucine producers to reduce exposure to market spikes and secure preferential allocation during tight supply periods.

- Use the report’s supplier scorecards: Leverage our comparative profiles and risk matrices in RFPs and due‑diligence checklists to shorten lead times on supplier selection.

- Embed scenario planning: Incorporate the report’s downside and upside cases into capex reviews, price‑pass‑through clauses and inventory policy reviews.

- Targeted M&A and JV opportunities: For investors and strategic buyers, prioritise targets that either close a capability gap (e.g., quality documentation, regulatory foothold) or provide complementary scale in production.

How PW Consulting’s Boc‑L‑Leucine report supports execution

This report is intended as an operational toolkit rather than a high‑level narrative. Subscribers receive raw model files, supplier scorecards, negotiation templates and an M&A screening matrix that can be adapted for internal diligence and board deliberations. We purposely treat the segmented datapoints and supplier score weights as gated content: the press summary outlines directional findings and executive imperatives, while the full report contains the detailed segment tables and the full benchmarking intelligence necessary for procurement execution and transaction support.

Next steps

If your 2026 plans include capital allocation to peptide chemistry, reworking procurement frameworks, or executing strategic transactions in the amino‑acid derivatives space, PW Consulting’s Boc‑L‑Leucine Market report is designed to shorten decision cycles and mitigate execution risk. Access the full report to retrieve the underlying segment tables, supplier scorecards and downloadable models that operational teams use to execute the playbook summarized here.

For immediate enquiries or to request a sample exhibit and purchasing details, visit PW Consulting’s report portal or contact our market team for a briefing tailored to your business needs.

For detailed analysis of this topic, please visit the official page: Boc L Leucine Market

Lacy Lee

Senior Marketing Manager

sales@pmarketresearch.com

00852-95632430

PW Consulting: www.pmarketresearch.com

Tags

PW Consulting

The Best-reviewed Subdivided Market Risk Analysis Firm in the US and East Asia.