PW Consulting: Building Dedicated Outdoor Air System Market to Reach USD 8.86 Billion by 2032, Driven by a 7.85% CAGR

Building Dedicated Outdoor Air System Market: Strategic Insights for 2026 Decisions

Executive summary

As organizations finalize capital plans for 2026, Dedicated Outdoor Air Systems (DOAS) have moved from niche specifications to central elements of building decarbonization, indoor air quality (IAQ) strategies, and compliance programs. PW Consulting’s latest market study—anchored on a 2025 base year and forecasting through 2032—finds the global DOAS market to be a multi-billion-dollar opportunity. After steady expansion during 2020–2025, the market recorded a measured increase to USD 5,214.5 million in 2025 and is projected to grow at a compound annual growth rate (CAGR) of 7.85% through our 2026–2032 forecast window, reaching roughly USD 8.9 billion by 2032.

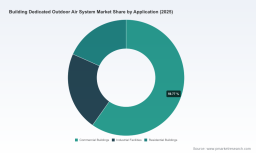

Building Dedicated Outdoor Air System Market

Why this matters for 2026 decision-makers

Three concurrent dynamics make 2026 a pivotal year for commercial real estate owners, HVAC OEMs, utilities, and large contractors:

Building Dedicated Outdoor Air System Market

- Regulatory pressure is increasing around system-level energy performance and moisture removal metrics, elevating DOAS from optional ventilation devices to compliance-driving equipment.

- Electrification and heat-pump integration are reshaping product roadmaps and procurement specifications, creating winners and laggards among manufacturers.

- Market structure remains moderately consolidated—while leading suppliers command meaningful scale, a large long tail of specialists sustains intense innovation and price competition.

For executives planning capital allocations, product roadmaps, or M&A activity in 2026, timely, sector-specific intelligence on these fronts is essential. PW Consulting’s report is designed to convert that intelligence into executable priorities over the coming 12–18 months.

Building Dedicated Outdoor Air System Market

Market outlook: what the headline numbers hide and reveal

The headline trajectory—mid-single-digit to high-single-digit growth culminating in a near-doubling of revenue by 2032—highlights a market driven by retrofit demand, new construction ventilation codes, and technology upgrades (dehumidification, energy recovery, and integrated heat pumps). However, beneath that top-line expansion are differentiated pockets of margin improvement, supply-chain vulnerability, and specification-led procurement dynamics. Our analysis explains where to deploy capital to capture the higher-margin segments, how to hedge material inputs, and which go-to-market models accelerate adoption without eroding ASPs.

Competitive dynamics: players, positioning, and recent moves

The competitive landscape mixes large multinational OEMs with specialized manufacturers. Our report profiles the capabilities, strategic priorities, and product architectures of the market’s most influential participants—evaluating not only product portfolios but also service models and channel strategies.

- Greenheck Fan Corporation: Known for a broad line of pre-engineered rooftop DOAS units, Greenheck expanded capacity and electrified offerings in 2025–2026—most notably by increasing large-capacity rooftop models and adding air-source heat pump options to selected product lines. This dual move accelerates their appeal for both compliance-driven projects and clients seeking electrification-ready solutions.

- Trane Technologies: With DOAS offerings that emphasize humidity control and energy efficiency, Trane is aligning product development with DOE efficiency expectations and large-portfolio building owners seeking harmonized energy strategies.

- AAON, Carrier, Johnson Controls (YORK): These large OEMs combine scale manufacturing with configurable architectures to serve institutional and large commercial clients. Their investments are concentrated on performance, integrated controls, and meeting emerging energy standards.

- Specialists—Addison HVAC, Desert Aire, United CoolAir, XeteX, and others: These firms focus on niche applications (precision dehumidification, retrofit packages, fully-custom DOAS) and provide the innovation and customization that many projects require.

Our competitive chapter maps product breadth, channel reach, typical deal sizes, and aftermarket revenue potential for each named player, and identifies strategic adjacencies for partnership or bolt-on acquisition.

Regulation, standards, and supply-chain dynamics shaping 2026

Regulatory shifts in 2025–2026 tightened minimum efficiency expectations and standardized performance metrics for DX-DOAS units—changes that directly affect product eligibility in publicly-funded projects and many corporate procurement frameworks. Standards such as AHRI 920 have become de facto performance baselines, and recent rulemaking enforces them in procurement and code compliance contexts. Our analysis covers:

- How new DOE efficiency requirements change total cost of ownership (TCO) calculations for DX-DOAS versus heat-pump-based DOAS.

- Spec-writing strategies to ensure competitive bidding while preserving long-term energy savings.

- Supply risk from raw material exposure—particularly copper—and strategies to mitigate input-cost volatility through design, hedging, and supplier diversification.

What the report delivers: operational modules for 2026 execution

Rather than just describing market direction, the report is structured as a practical playbook for teams executing in 2026. Core deliverables include:

- Commercial playbooks: standard spec templates, bid evaluation matrices, and retrofit priority checklists calibrated to different asset classes.

- Financial tools: TCO and NPV models adjusted for energy price scenarios, tax incentives, and anticipated maintenance costs—ready to be adapted to client portfolios.

- Procurement and sourcing frameworks: supplier scorecards, total delivered-cost assumptions, and sourcing timelines that reflect lead-time inflation and material risk.

- Product roadmaps: feature-prioritization matrices juxtaposing DOE compliance, electrification pathways (heat pumps), and energy-recovery integration to inform R&D and partnership choices.

- M&A and partnership playbook: acquisition target profiling, synergy quantification, and integration checklists for strategic buyers seeking scale or technical gaps.

Strategic recommendations for 2026 (actionable priorities)

Our advisory guidance is purpose-built for near-term decision windows. Recommendations are prioritized and sequenced for organizations with different objectives—OEMs, building owners/operators, EPCs, and investors:

- For OEMs: accelerate modular electrified DOAS variants that comply with current efficiency metrics; bundle controls and commissioning services to protect margins as unit prices compress.

- For building owners/operators: adopt a staged retrofit approach—prioritize spaces with high latent loads and occupant density for early DOAS deployment to maximize IAQ benefits and near-term energy savings.

- For EPCs and integrators: develop fixed-scope retrofit packages with clear performance guarantees and a streamlined commissioning protocol to reduce deployment risk and shorten payback timelines.

- For investors and private equity: target niche specialists with strong aftermarket service streams or OEMs with scalable modular platforms—these offer asymmetric value creation through consolidation and cross-selling.

Risk matrix and KPIs to monitor in 2026

The report includes a prioritized risk matrix and recommended KPIs to track throughout 2026 to inform course corrections:

- Regulatory compliance risk: certification timelines and product requalification status under current performance standards.

- Supply-chain cost pressure: copper and refrigerant availability and cost trajectories, and their impact on BOM.

- Market adoption risk: retrofit uptake velocity, driven by capital availability and competing decarbonization priorities.

- Operational KPIs: installed cost per cfm, commissioning time per installation, warranty claim rate, and aftermarket revenue per unit.

How PW Consulting’s report supports immediate 2026 actions

PW Consulting’s Building DOAS Market report is intentionally tactical: it translates macro forecasts (including the market’s 2025 baseline and the 7.85% CAGR outlook) into concrete steps for procurement, product development, and M&A prioritization. The report’s templates, models, and vendor evaluations are set up to be used directly in RFPs, board-level investment memos, and engineering specifications—helping teams move from strategic intent to implemented projects within months.

Conclusion and next steps

DOAS is now central to the narrative on indoor air quality, energy efficiency, and building electrification. As the marketplace expands—from the multi-billion-dollar baseline in 2025 into a nearly USD 9 billion market by the early 2030s—organizations that adopt a disciplined, data-driven approach in 2026 will capture outsized returns.

PW Consulting’s full report contains the granular regional, application, and product splits, detailed competitor benchmarking, and downloadable operational tools referenced above. For teams preparing 2026 budgets, product roadmaps, or acquisition pipelines, the full intelligence set provides the validated inputs necessary for confident execution.

For detailed analysis of this topic, please visit the official page: Building Dedicated Outdoor Air System Market

Lacy Lee

Senior Marketing Manager

sales@pmarketresearch.com

00852-95632430

PW Consulting: www.pmarketresearch.com

Tags

PW Consulting

The Best-reviewed Subdivided Market Risk Analysis Firm in the US and East Asia.