PW Consulting: Intelligent Fire Emergency Lighting & Evacuation System Market Hits USD 3,450 Million in 2025, Set for 8.5% CAGR to USD 6,107 Million by 2032

Intelligent Fire Emergency Lighting And Evacuation Indication System Market — Strategic Outlook for 2026 Decision‑Makers

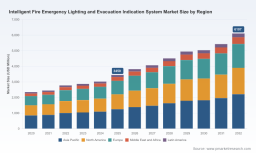

PW Consulting’s new market research brief on the Intelligent Fire Emergency Lighting and Evacuation Indication System market synthesizes five years of historical evidence (2020–2025) and a 2026–2032 forecast horizon to equip executives, procurement leaders, and investors with the actionable intelligence required to make high‑stakes decisions in 2026. The market grew from the low billions in 2020 to an estimated USD 3,450 million in 2025 and is projected to expand at a compound annual growth rate (CAGR) of 8.5% over the 2026–2032 period, reaching over USD 6.1 billion by 2032. This rapid trajectory is being shaped by regulatory tightening, technological convergence with smart building platforms, and evolving expectations for adaptive, data‑driven life‑safety systems.

Intelligent Fire Emergency Lighting And Evacuation Indication System Market

What the report delivers — practical, decision‑grade insights

- Market sizing & forecast model: a transparent, auditable framework that traces the market to 2025 and projects through 2032, with scenario variants for conservative, base, and accelerated adoption paths.

- Regulatory and standards map: a practitioner’s digest of recent and pending rules (global and market‑specific), compliance deadlines, and their procurement and engineering implications.

- Vendor benchmarking and competitive scorecards: capability matrices evaluating product breadth (controllers, luminaires, exit indicators), systems integration, compliance posture, and service models.

- Technology roadmap and product evaluation templates: how to assess adaptive evacuation, personnel‑positioning, Bluetooth‑enabled devices, remote testing, and cybersecurity for life‑safety assets.

- Procurement playbooks and retrofit vs. new‑build decision trees: procurement KPIs, TCO modelling templates, and migration strategies for legacy installations.

- Investment and M&A lens: value levers, target archetypes, and integration risks for strategic buyers and PE investors seeking to enter or consolidate the space.

Why this matters for 2026 — forces that will determine winners and losers

Three structural dynamics make 2026 a pivotal year:

Intelligent Fire Emergency Lighting And Evacuation Indication System Market

- Standards and certification acceleration. Recent regulatory updates materially change product and testing requirements. Notable changes include new provisions under several national and regional standards that expand luminous requirements, mandate adaptive escape lighting considerations, and tighten documentation and periodic test obligations. These changes create compliance cliffs and procurement windows that facility owners, integrators, and manufacturers must navigate in 2026 to avoid supply disruptions and non‑compliance risks.

- Smart building integration and data sophistication. Emergency lighting and evacuation systems are shifting from isolated, hardwired products to networked subsystems that share occupancy data, alarm states, and routing decisions with building management and fire alarm systems. Buyers in 2026 will prioritize interoperability, firmware update policies, and analytics capability as much as luminaire performance.

- Operational resilience and lifecycle economics. Facility managers are evaluating systems not only on capex but on lifecycle metrics: remote testability, preventive maintenance intervals, battery and central‑system replacement cycles, and insurance/occupancy cost implications. The aggregate market growth and the speed of technology replacement make lifecycle planning an executive priority for 2026 procurement cycles.

Regulatory timeline that shapes 2026 decisions

- Several national certification regimes updated product scopes and test requirements in 2024–2025, with explicit conversion or compliance deadlines that fall in the 2025–2027 window. These deadlines create a near‑term urgency for manufacturers and installers to validate product lines and for end‑users to confirm vendor compliance as part of tendering processes.

- Regional standards addressing luminous criteria, adaptive escape lighting, and periodic measurement intervals have been published or revised recently and will drive specification changes in public infrastructure and commercial projects through 2026 and beyond.

- Regulatory change is not uniform: divergent timelines and technical requirements across markets mean multinational rollouts will require tailored certification and testing roadmaps rather than one‑size‑fits‑all procurement contracts.

Competitive landscape — positioning the principal players

The market exhibits moderate concentration: the top three vendors control roughly one‑third of the market while the top five account for under half—indicating room for both global platform leaders and specialist challengers. Against that backdrop, strategic posture and go‑to‑market choices determine share gains.

Intelligent Fire Emergency Lighting And Evacuation Indication System Market

- Global systems integrators and platform leaders (e.g., Siemens, Honeywell, Eaton). These incumbents leverage broad building‑systems portfolios and established channel relationships to deliver integrated emergency lighting tied to fire alarms, voice evacuation, and building management systems. Their advantages include global certification footprints, deep integration capabilities, and attractive total‑solution offers for large commercial and critical infrastructure projects.

- Specialists and innovators (e.g., Evaclite, Advanced, Mircom). Vendors focused on dynamic signage, adaptive exit indications, and addressable automatic testing are competing on product innovation, niche compliance expertise, and agility in standards adoption. They are frequently prime targets for partnerships or acquisition by larger integrators seeking to add adaptive capabilities quickly.

- Regional suppliers and Chinese manufacturers (e.g., TYEE, Orena, Sanjiang, Beijing Mingri). These companies play a crucial role in local markets where certification and government procurement preferences favour domestic suppliers. Their strengths include price competitiveness, localized support, and rapid design cycles to meet specific national regulation changes.

Recent certification events and standard updates have already begun to shift competitive dynamics—certifications aligned to new standards have conferred short‑term advantage in certain tenders, while non‑compliant legacy portfolios are being phased out in procurement specifications.

Technology and product trends shaping supplier selection

- Adaptive evacuation and real‑time guidance. Systems that dynamically reconfigure exit signage and lighting based on alarm inputs, smoke modelling, and occupant location are becoming a procurement differentiator for complex public buildings and critical infrastructure.

- Positioning and connectivity. Bluetooth and personnel‑positioning functions are moving from optional extras to required features in some jurisdictions, enabling routing optimisation and post‑incident accounting.

- Remote testability and predictive maintenance. Automated testing and analytics reduce inspection cost and can materially alter lifecycle estimates used in capital planning.

- Cybersecurity and safety assurance. As systems become networked, firmware update controls, authenticated communications, and audit trails are no longer IT niceties but safety requirements that must be evaluated during procurement.

Actionable recommendations for 2026 leaders

- Implement a regulatory‑first procurement checklist: require vendor certification evidence mapped to the latest standard versions and include contractual remedies for non‑compliance discovered post‑delivery.

- Prioritize interoperability in RFPs: demand published APIs, standardized alarm integration, and third‑party test evidence of system interactions with BMS and fire panels.

- Run risk‑weighted retrofit vs. replacement analyses: combine site‑level hazard models with lifecycle cost to determine whether modular upgrades (controllers, signage) or full system replacement deliver better risk reduction per dollar.

- Pilot adaptive evacuation in high‑value sites: run a tightly scoped pilot that tests positioning, dynamic signage, analytics, and operator workflows to validate vendor claims before portfolio‑wide rollouts.

- Embed lifecycle clauses in supplier contracts: performance SLAs for battery health, remote test pass rates, and software maintenance should be contractually enforceable and linked to payment milestones.

- Assess M&A and partnership targets through a compliance lens: niche providers with strong adaptive signage or positioning IP can be high‑value acquisitions—but only if their certification footprint can be rationalized cost‑effectively.

For investors — where to look in 2026

Investment upside is most visible in software and analytics providers that enable adaptive evacuation logic, and in firms offering modular retrofit solutions that reduce installation complexity. Battery and central‑system innovations that extend maintenance intervals and lower TCO are attractive technical bets. However, regulatory uncertainty and heterogeneous certification regimes introduce execution risk; investors should prioritise targets with clear pathways to multi‑market certification or with strong local procurement moats.

Conclusion — the report’s strategic value for 2026

For executives preparing capital programs, procurement teams redesigning specifications, and investors evaluating acquisition targets in 2026, the PW Consulting report provides a uniquely practical blend of market sizing (with transparent forecasts and scenario analysis), compliance timelines, vendor benchmarking, and tangible procurement tools. It shows where regulatory deadlines will compress procurement windows, how technological advances are reshaping vendor selection, and which strategic moves reduce execution risk.

To preserve the integrity of strategic decision‑making we have intentionally kept granular regional splits and detailed segment revenue lines out of this press summary — these finer‑grained data and the full vendor scorecards are available in the full report. For executives who need to align 2026 capital plans with the evolving standards and vendor capabilities, the detailed models, RFP templates, and vendor matrices in the full PW Consulting report are essential.

Visit PW Consulting’s report page to access the complete dataset, methodology, and procurement toolkits that underpin this executive briefing and to download your copy of the full Intelligent Fire Emergency Lighting And Evacuation Indication System Market report.

For detailed analysis of this topic, please visit the official page: Intelligent Fire Emergency Lighting And Evacuation Indication System Market

Lacy Lee

Senior Marketing Manager

sales@pmarketresearch.com

00852-95632430

PW Consulting: www.pmarketresearch.com

Tags

PW Consulting

The Best-reviewed Subdivided Market Risk Analysis Firm in the US and East Asia.