PW Consulting: Networked Pulse Oximeter Market Poised to Reach USD 2,070.16 Million by 2032, Growing at an 8.75% CAGR (2026–2032)

Networked Pulse Oximeter Market — Strategic Briefing for 2026 Decision-Makers

Executive snapshot

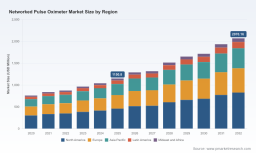

The networked pulse oximeter market has evolved from a niche connectivity play into a core infrastructure component for acute care and remote monitoring. Our analysis shows the global market expanding from approximately USD 760.5 Million in 2020 to USD 1,150.8 Million in 2025, with a forecasted compound annual growth rate (CAGR) of 8.75% through the 2026–2032 horizon. By 2026 the market is modeled to surpass USD 1.29 Billion (USD Million basis), and our scenario workplaces toward just over USD 2.07 Billion by 2032 under a central connectivity adoption pathway.

Networked Pulse Oximeter Market

Why PW Consulting’s 2026 perspective matters

- Timing: 2026 is a pivot year — reimbursement updates, draft regulatory guidance matured into clearer expectations, and product innovation cycles are converging. Decisions made this year determine participation in the next wave of hospital procurements and RPM (remote patient monitoring) deployments.

- Risk vs. opportunity: The market’s moderate concentration (a CR3 of ~48.5% and CR5 of ~62.3%) indicates leading incumbents remain influential, yet there is clear room for disruptive entrants that combine robust clinical accuracy, wireless reliability, and seamless systems integration.

- Execution focus: Winning in 2026 is less about single-product performance and more about validated clinical claims, regulatory-proof design (EMC, cybersecurity), reimbursement-ready data flows, and scalable data ops for health systems.

What the report delivers — practical modules for immediate action

Our Networked Pulse Oximeter Market report is structured as an operational playbook for commercial and clinical leadership. It synthesizes market sizing, dynamic drivers, and tactical workstreams into reproducible deliverables you can deploy this quarter:

Networked Pulse Oximeter Market

- Market sizing and scenario modeling (base year 2025, historical 2020–2025; forecast 2026–2032 with multiple adoption curves) that allow CFOs to stress-test revenue and margin plans under conservative, baseline, and accelerated-networking scenarios.

- Go-to-market playbooks tailored to OEMs, device integrators, and software platforms — including channel strategies for acute care, ambulatory surgery, and home-monitoring bundles.

- Regulatory readiness checklists translating the January 2025 FDA draft guidance into concrete product design and clinical test protocols, with recommended sample sizes, skin-pigmentation verification steps, and labeling templates.

- Reimbursement roadmaps that align device telemetry features with CMS RPM CPT codes (including the new 2026 code additions), specifying telemetry configurations and data upload patterns that enable billing compliance.

- Interoperability and cybersecurity blueprints mapped to IEC 60601-1-2 compliance expectations and FDA premarket submission pathways for radiofrequency-enabled devices.

- Vendor benchmarking frameworks and negotiation playbooks that weigh clinical accuracy, integration APIs, total cost of ownership, and post-market surveillance obligations.

- Use-case ROI calculators and deployment pilots: acute continuous monitoring, perioperative pulse oximetry integration, and home-based chronic disease management — each with operational KPIs and sample P&L impact.

Competitive landscape — who to watch and what they signal

The competitive environment blends long-established patient monitoring OEMs with agile telehealth device specialists. Leading entrants are pursuing three strategic vectors: clinical-grade accuracy claims, connectivity-first productization, and system-level partnerships.

Networked Pulse Oximeter Market

- Masimo Corporation (Irvine, CA) continues to push tetherless and wearable platforms, with Bluetooth-enabled PPG solutions and partnerships that drive multi-parameter integration into larger monitoring ecosystems.

- Medtronic (Nellcor legacy) remains a key integrator for bedside and central monitoring systems, focusing on reliability and hospital workflows.

- Koninklijke Philips offers connected modules and emphasizes data integration into HIS and remote monitoring platforms, leveraging cross-portfolio hospital relationships.

- GE HealthCare is advancing wearable and Bluetooth strategies that emphasize EHR connectivity and scalable hospital deployments.

- Nonin Medical, Nihon Kohden, Contec, and leading Chinese and US telehealth specialists (including Viatom and Prevounce) are concentrating on cost-performance balance and regulatory clearances for remote use.

- Smaller innovators such as OxiWear are differentiating on form factor (ear-worn continuous monitoring) and FDA-cleared continuous solutions optimized for ambulatory and home use.

Recent market moves signal two important trends: (1) regulatory clarity is accelerating productization — several firms secured or announced FDA 510(k) clearances through 2024–2025; (2) new cellular and Bluetooth-enabled devices are shifting the cost-benefit calculus for RPM programs by reducing dependency on patient Wi‑Fi and improving data continuity.

Regulatory, reimbursement, and technical headwinds

- Regulation: The FDA’s January 2025 draft guidance has reframed expectations for clinical performance validation — recommending controlled desaturation studies with significant participant diversity and calling for transparent labeling regarding potential performance differences by skin pigmentation. This raises the bar for clinical evidence and labeling, especially for devices intended for broad populations.

- Standards & safety: Radiofrequency-enabled pulse oximeters must demonstrate electromagnetic compatibility and cybersecurity robustness consistent with IEC 60601‑1‑2 and FDA cybersecurity guidance — a non-trivial engineering and QA effort for smaller vendors.

- Reimbursement: CMS updates to RPM CPT codes (and the 2026 code additions) open clear billing pathways for physiologic data derived from connected pulse oximeters, but reimbursement depends on automatic data upload and clinically actionable workflows — not merely device ownership.

- Market fragmentation risks: While the top manufacturers command a substantial share of market dollar value, interoperability gaps and differing clinical validation standards create fragmentation opportunities for vendors that can deliver turnkey clinical evidence and integration services.

Strategic imperatives for 2026 decision-makers

To convert market growth into sustainable advantage, organizations should adopt a dual approach: shore up compliance and evidence, and accelerate systemic integration that lowers adoption friction.

- Manufacturers: Prioritize clinical validation programs that follow rigorous, diverse-population protocols. Invest early in IEC and cybersecurity testing and align labeling to emerging FDA expectations. Packaging connectivity as a clinical workflow (not a commodity feature) will unlock premium placements.

- Health systems and IDNs: Shift procurement KPIs from unit price to data fidelity and operational throughput. Require vendors to demonstrate end-to-end data flows into EHRs and RPM platforms, and insist on post-deployment performance monitoring tied to clinical outcomes.

- Payers & government agencies: Design reimbursement that rewards continuous, clinically validated monitoring with demonstrable reductions in avoidable admissions. Pilot risk-sharing contracts linked to validated oxygenation management pathways.

- Investors & acquirers: Look for companies with defensible clinical evidence, cleared regulatory status, and partnership traction with major monitoring platforms or EHR integrators. Cellular-first solutions and validated wearables that reduce patient technology burden are prime targets.

Operational playbook — four near-term moves

- Test for clinical robustness now: Begin controlled desaturation verification studies that emulate the FDA-recommended diversity mix — outsourcing to CROs can compress timeline and spread cost.

- Embed interoperability as a product requirement: Ship devices with production-grade APIs, HL7/FHIR-ready data models, and clear integration reference implementations for central monitoring stations and RPM platforms.

- Align reimbursement and telemetry behavior: Ensure devices can provide continuous, automatic uploads in the cadence required by CPT rules; build clinical decision-support to demonstrate treatment management value.

- Design post-market surveillance into launch: Collect real-world performance data by skin pigmentation and use-case, and publish findings to build trust with health systems and regulators.

What we intentionally withheld — and why you should download the full report

This briefing highlights the structural story, regulatory inflection points, and competitive vectors you must act on in 2026. To preserve the “trailer” principle — providing strategic conviction without displacing the proprietary value in our modelling — we have omitted full granular segment breakdowns, regional shares, and the vendor-by-vendor revenue comparatives that underpin our market concentration analysis. The full report contains:

- Detailed segment performance matrices and regional adoption curves (by product family and end-user) that power our revenue scenarios;

- Vendor scorecards with weighted criteria on accuracy, connectivity, regulatory readiness, and go-to-market strength;

- Deployment playbooks with sample RFP language and contract terms targeted at health systems and RPM integrators;

- Interactive financial models and sensitivity analyses to stress-test unit economics under multiple reimbursement and regulatory timelines.

Final word — readiness beats timing

The networked pulse oximeter market is no longer a peripheral device category; it is a strategic lever for patient monitoring modernization and remote care expansion. With a compound annual growth trajectory near 8.75% for the coming forecasting window, 2026 is the moment to convert technical roadmaps into regulatory-grade evidence and clinical-grade integrations. Organizations that align product design, regulatory strategy, and reimbursement-aware workflows in 2026 will establish durable advantage as the market scales toward the early 2030s.

Contact PW Consulting to access the full Networked Pulse Oximeter Market report, proprietary models, and tailored advisory engagements to operationalize these findings in your 2026 planning cycle.

For detailed analysis of this topic, please visit the official page: Networked Pulse Oximeter Market

Lacy Lee

Senior Marketing Manager

sales@pmarketresearch.com

00852-95632430

PW Consulting: www.pmarketresearch.com

Tags

PW Consulting

The Best-reviewed Subdivided Market Risk Analysis Firm in the US and East Asia.