PW Consulting: Microbes Protein Hydrolysates Market Set to Expand at a Strong 6.45% CAGR, Signaling Major Growth Ahead

Microbial Protein Hydrolysates: Strategic Imperatives for 2026 — PW Consulting Market Intelligence Brief

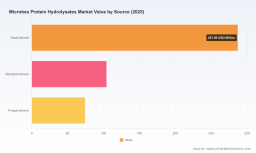

PW Consulting’s latest market study on Microbial Protein Hydrolysates (base year 2025) delivers an actionable strategic lens for executive teams planning near‑term investments, partnerships, and product roadmaps. The global market reached approximately USD 465.5 Million in 2025 and is projected to grow at a compound annual growth rate (CAGR) of 6.45% over the 2026–2032 forecasting window, unfolding into a market north of USD 700 Million by the end of the period. This growth trajectory — coupled with a mid‑tier concentration profile among incumbents — creates both consolidation opportunities and niche openings for differentiated players.

Microbes Protein Hydrolysates Market

Why this report matters for 2026 decisions

-

Timing of commercialization: 2026 is a pivotal inflection point. Several technology platforms have moved from pilots to commercial output and regulatory approvals — turning previously theoretical applications into bankable revenue streams. The report synthesizes implications for capex timing, pricing models, and scale economics.

Microbes Protein Hydrolysates Market -

Capital allocation under uncertainty: With steady mid-single‑digit CAGR and visible pathway to maturity, boards must weigh continued R&D versus accelerating commercialization. PW Consulting maps the capital intensity and payback profiles by technology family to inform portfolio-level choices.

Microbes Protein Hydrolysates Market -

Regulatory arbitrage and first‑mover advantage: Recent approvals for microbial single‑cell proteins in targeted feed sectors have materially altered market entry dynamics. Our analysis highlights the jurisdictions where regulatory momentum lowers go‑to‑market friction and where strategic regulatory investment yields outsized returns.

What the study delivers — practical, decision‑grade intelligence

-

Full market sizing and trajectory: annualized market values across the historical window (2020–2025), validated 2025 baseline, and the 2026–2032 forecast built on bottom‑up and top‑down triangulation. These inputs are designed for CFOs and strategy teams to stress‑test revenue scenarios and valuation models.

-

Technology and feedstock cost models: detailed unit economics for methanotrophic gas fermentation, autotrophic (CO2+H2+electricity) production, and conventional yeast fermentation. The models quantify sensitivity to primary inputs (natural gas / methane, electricity, sugar feedstocks) and downstream hydrolysis and drying costs — enabling scenario analysis for near‑term margin improvement.

-

Commercial readiness assessment: a pragmatic taxonomy of pilot, scale‑up and commercial stages across leading firms and technology routes, with the operational constraints and regulatory gating factors that typically extend timelines.

-

Go‑to‑market playbooks: product positioning matrices for animal feed, pet nutrition, human food ingredients, and high‑value biotech/pharma applications — each with suggested channel strategies, pricing frameworks, and contract structures.

-

Competitive and M&A playbook: strategic options for entrants, incumbent ingredient suppliers, and potential acquirers, including bolt‑on criteria, valuation multipliers we observed in recent deals, and typical integration risks.

-

Regulatory heatmap and stakeholder map: jurisdictional pathways, expected timelines for approvals by application class, and recommended advocacy investments to accelerate acceptance across feed and food regulators.

Competitive landscape: actionable takeaways

The market displays moderate concentration — with the top three players accounting for a meaningful but non‑dominant share and the top five approaching half of the market by revenue. This structure supports both consolidation and specialist niches. Our qualitative and quantitative review of leading companies highlights several archetypes and strategic behaviors worth noting:

-

Industrial scale first movers (production‑led): Companies that have transitioned to commercial production and scaled off‑take arrangements are capturing early volume and learning‑curve advantages. Examples include firms that have completed regulatory milestones and moved to JV or contract manufacturing in regions with cost advantages or strategic feedstock access.

-

Technology innovators (platform play): Firms focused on novel carbon capture or gas fermentation routes that reduce land footprint and decouple production from agricultural inputs position themselves for premium applications in human food and specialty nutrition.

-

Ingredient incumbent adapters: Established ingredient and fermentation players are leveraging existing fermentation, drying, and distribution capability to offer microbial hydrolysates as adjacent product lines — accelerating market reach via existing customer relationships.

Company spotlight: strategic moves to watch

-

Unibio — regulatory traction to commercial growth: Securing feed approval in targeted jurisdictions for aquaculture feed has not only validated product safety and use cases but also unlocked practical commercial distribution routes into regional feed chains. For potential partners and acquirers, regulatory validation significantly de‑risks volume contracts.

-

Calysta — operational consolidation and focus: The company’s decision to wind down non‑core pilot facilities and shift to concentrated commercial production via joint ventures reflects a pragmatic industrial strategy: funnel R&D learnings into repeatable, high‑utilization manufacturing in cost‑efficient geographies. This model underscores the strategic value of offsite JV manufacturing for scale and cost competitiveness.

-

Solar Foods — product diversification into human nutrition: Demonstrations of variable protein density offerings in beverage formats illustrate how technology that decouples production from agricultural land can rapidly target premium food applications. This trajectory is informative for firms considering premiumization strategies versus bulk volume plays.

-

Angel Yeast, Kerry, DSM‑Firmenich, Corbion, Lallemand, and Alltech — incumbents shaping demand and supply: These companies underscore two salient strategic options for legacy ingredient suppliers: (1) integrate microbial hydrolysates into existing portfolios to retain share, or (2) pursue selective partnerships or acquisitions to accelerate capability build‑out without diluting core margins.

Sector dynamics and investment implications

-

Feedstock and energy economics are primary cost levers: The choice of upstream input — methane, CO2+H2/electricity, or sugars — defines both cost volatility exposure and sustainability credentials. Executive teams should model scenarios that incorporate decarbonization incentives and potential carbon pricing to understand competitive positioning four to seven years out.

-

Regulatory milestones unlock pathways to scale: Demonstrable approvals in feed segments have historically led to rapid contract growth in aquaculture and livestock. Capturing early off‑take in jurisdictions with favorable regulation can materially accelerate revenue ramp and shorten payback horizons.

-

Downstream application mix drives margin dispersion: Hydrolysates targeted at animal feed and pet nutrition show different margin and route‑to‑market characteristics versus hydrolysates formulated for food or pharmaceutical use. Companies should align R&D and commercial teams to the margin profile and channel complexity of their chosen application bucket.

-

Manufacturing strategy matters: Outsourced JV production can offer speed to market and capital efficiency, but risks include loss of process control and IP leakage. Conversely, vertically integrated assets increase control and long‑term margin capture but require higher upfront capital and longer scale timelines.

How to use the report in 2026 planning cycles

-

Investment committees: Use the report’s sensitivity models to stress‑test capex proposals against feedstock price shocks and regulatory delay scenarios. Our work provides discrete inputs for discounted cash flow and break‑even analyses.

-

Corporate development: Leverage the competitive map and M&A playbook to prioritize targets — whether to buy capability, secure supply, or eliminate a potential disrupter. We identify the practical integration risks and realistic synergies by archetype.

-

Commercial teams: Adopt the go‑to‑market playbooks for channel selection and pricing architecture based on application‑level complexity and customer procurement behavior.

-

R&D and operations: Align process optimization priorities with the cost drivers identified in our tech and feedstock models to maximize ROI on incremental improvement projects.

Concluding perspective — a strategic trailer

Microbial protein hydrolysates are moving from niche science to commercially viable industrial pathways. The PW Consulting study quantifies that transition and frames the strategic choices facing CEOs and boards in 2026: where to allocate capital, which partnerships to pursue, and how to position products across feed, food, and high‑value biotech segments. This briefing has outlined the macro trajectory — including a baseline market of some hundreds of millions in 2025 and a forecasted multi‑hundred‑million expansion through 2032 at a CAGR of ~6.45% — and highlighted the competitive and regulatory inflection points shaping near‑term outcomes.

For practitioners ready to translate these insights into executable plans, the full PW Consulting report contains the granular segment matrices, jurisdictional regulatory timelines, detailed unit economics by process route, and plug‑and‑play financial models that underpin the recommendations summarized here. Access to that level of detail enables rapid adaptation of corporate budgets, M&A screening, and commercial pilots aligned to 2026 priorities.

For detailed analysis of this topic, please visit the official page: Microbes Protein Hydrolysates Market

Lacy Lee

Senior Marketing Manager

sales@pmarketresearch.com

00852-95632430

PW Consulting: www.pmarketresearch.com

Tags

PW Consulting

The Best-reviewed Subdivided Market Risk Analysis Firm in the US and East Asia.