PW Consulting: Purpura Treatment Market to Expand at a 5.85% CAGR Through 2032, Unlocking New Opportunities

Purpura Treatment Market: Strategic Imperatives for 2026 — PW Consulting Insights

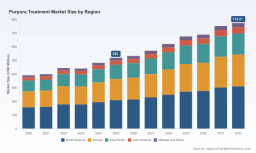

As healthcare leaders prepare strategic plans for 2026, PW Consulting’s latest Purpura Treatment Market report delivers a compact but high-impact evidence base to inform decisions across commercial, clinical development, supply chain, and corporate strategy functions. Built on a 2020–2025 historical foundation (base year 2025) and forward-looking to 2032, our model shows steady expansion at a compound annual growth rate (CAGR) of 5.85%. The market reached roughly USD 520 million in 2025 and our scenario suite points to continued growth through 2032, underscoring that purpura therapeutics remain an attractive, evolving subsegment of hematology.

Purpura Treatment Market

Why this report matters for 2026 decision-makers

-

Timing: The product and regulatory landscape shifted materially in 2025 with several approvals and late-stage readouts that change competitive dynamics and addressable populations — creating both immediate commercialization opportunities and near-term access challenges.

Purpura Treatment Market -

Clarity: PW Consulting translates market momentum into tactical priorities — which molecules will require accelerated launch investments, where payer hurdles will slow uptake, and which supply constraints pose operational risk.

Purpura Treatment Market -

Actionability: Our report is built to be used in boardrooms and commercial planning cycles: it pairs quantitative forecasts with executable playbooks for launch sequencing, pricing strategies, and M&A screening tailored to purpura indications.

What the report contains — practical elements for 2026 planning

-

Bottom‑up market model (2020–2032) with base-year calibration, scenario variants, and sensitivity analysis designed for rapid incorporation into company financial models.

-

Clinical and regulatory map linking mechanism of action, label nuances, and likely line-of-therapy positioning for approved and late‑stage assets.

-

Commercial readiness assessments and launch playbooks: channel strategies, patient journey mapping, hub-and-spoke service design, and field-force prioritization templates.

-

Payer & reimbursement playbook: value dossiers, prior‑authorization triggers to anticipate, and contracting approaches (risk-sharing, outcome-based pilots) tailored to purpura treatment classes.

-

Supply‑chain risk analysis with mitigation options, including plasma-sourced products’ dependency mapping and alternative sourcing pathways.

-

Competitive intelligence and M&A/partnership screening frameworks — matching strategic objectives to target profiles and valuation heuristics.

-

Data annexes for model integration: download-ready spreadsheets, assumptions logs, and event-timeline overlays for scenario replication.

Key market dynamics shaping 2026 strategies

-

Regulatory momentum and label expansion. 2025 saw approvals that materially alter the clinical toolkit — including new mechanistic classes and pediatric label extensions. These approvals expand treatable populations but also invite rapid payer scrutiny on real-world effectiveness versus existing standards.

-

Line‑of‑therapy economics and access gatekeeping. Payers continue to enforce prior‑therapy requirements for many purpura interventions. For manufacturers, this raises the bar for negotiating coverage: evidence generation must demonstrate not only efficacy but measurable reductions in acute care utilization and bleeding events.

-

Supply dependence in biologicals. IVIG and other plasma‑derived therapies remain vulnerable to donor supply and fractionation throughput. Companies exposed to plasma sourcing need active hedging strategies — ranging from multi-supplier contracts to investments in capacity through strategic alliances.

-

Moderate market concentration. The market structure is neither atomized nor fully consolidated. Leading firms command meaningful shares of prescription volume and therapeutic mindshare, but there remains room for differentiation via novel mechanisms, pediatric formulations, and delivery innovations.

-

Clinical innovation converging with commercial differentiation. Advances in FcRn blockers, BTK inhibitors, TPO receptor agonists, and SYK/B cell axis modulators are shifting therapeutic decision trees — creating opportunities for combination strategies and label-expansion sequencing.

Competitive landscape — what incumbents and challengers are doing

-

Amgen Inc. — With an established thrombopoietin receptor agonist, Amgen’s priority is lifecycle management and defending market share through evidence generation and formulary engagement.

-

Novartis AG — Novartis is leveraging combination trial readouts to move therapeutics earlier in the treatment algorithm; success in pivotal trials could reposition established agents into broader treatment pathways.

-

Swedish Orphan Biovitrum (Sobi) — Recent pediatric approvals and formulation innovation highlight Sobi’s playbook: extend labels to expand addressable patients while optimizing delivery for adherence.

-

Sanofi — The entrant of a BTK inhibitor into the landscape signals a strategic shift: mechanism diversification aimed at patients with inadequate response to prior therapies, backed by a prioritization of adult chronic use cases.

-

Rigel Pharmaceuticals — Continued focus on commercialization and IP clarity around an oral SYK inhibitor underscores an execution-first approach in a competitive middle market.

-

Grifols, S.A. — As a major supplier of IVIG, Grifols’ operational footprint in plasma collection and fractionation is a strategic asset — but also a sensitivity point for industry supply security.

-

argenx SE — FcRn-targeted therapy approvals demonstrate the commercial potential of precision immunomodulation and reinforce the importance of long-term real-world safety and efficacy data for label defense.

Strategic plays for 2026 — recommended priorities

-

Prioritize pediatric development and formulation. Payer receptivity to pediatric indications can unlock durable revenue streams if supported by adherence-friendly formulations and real-world safety commitments.

-

Invest early in real‑world evidence (RWE). Capture outcomes that matter to payers (hospitalization avoidance, bleeding episodes, steroid-sparing effects) to shorten contracting cycles and justify premium pricing.

-

De-risk plasma exposure. For companies reliant on plasma-derived inputs, secure tiered supply agreements and consider minority-stake investments in fractionation capacity.

-

Deploy segmentation-first commercial plans. Use narrow patient-flow analytics to identify high-yield treatment centers and specialty pharmacies where targeted field resources will maximize uptake.

-

Evaluate M&A for strategic gaps. Targets that close shortfalls in modality, access to specific patient cohorts, or manufacturing capacity offer asymmetric value creation.

-

Design flexible contracting pilots. Outcome-based agreements tied to objective clinical endpoints can materially reduce payer resistance for novel mechanisms with limited long-term data.

-

Prepare defensive IP and litigation playbooks. With several high-value assets nearing wider adoption, ensuring freedom-to-operate and preparing for patent challenges will preserve commercial timelines.

How PW Consulting’s deliverables accelerate execution

-

Integrated model and dashboard: rapid scenario toggles let commercial leaders test pricing, uptake, and access assumptions for board-level approvals within days, not weeks.

-

Launch readiness checklist: step-by-step tasks framed by weeks-to-launch, resource needs, and measurable KPIs to convert clinical approval into early revenue traction.

-

M&A screening tool: filters targets against capability gaps, time-to-market, and dilution impact — enabling rapid, evidence-based diligence for 2026 transactions.

-

Custom advisory support: our team can simulate payer negotiations, advise on evidence generation sequencing, or co-develop contracting pilots tailored to a client’s portfolio.

What the full report unlocks — and why you should download it

PW Consulting’s Purpura Treatment Market report is intentionally designed as both an executive briefing and an operational toolkit. The public summary you are reading highlights the macro trends, clinical inflection points, and strategic options that merit immediate attention in 2026. The full report provides the granular inputs you need to act — including country- and segment-level forecasts, patient-population models, payer-policy matrices, competitor share breakdowns by therapeutic class, and executable launch calendars. For teams planning budgets, commercial launches, or M&A activity next year, accessing this level of detail is essential to convert strategy into measurable outcomes.

To preserve the value of the proprietary datasets and preserve independence of client analyses, PW Consulting follows a “trailer” approach in our public commentary: we present the directional insights and execution frameworks that accelerate decision-making while reserving the detailed segmentation and numeric cells for subscribers and licensed clients.

For a conversation about how these insights apply to your portfolio or to request a demo of the report tools and forecast model, visit the PW Consulting Purpura Treatment Market page. Our team is available to walk through custom scenarios tailored to your company’s 2026 priorities.

— PW Consulting, Senior Strategy & Industry Analysis Team

For detailed analysis of this topic, please visit the official page: Purpura Treatment Market

Lacy Lee

Senior Marketing Manager

sales@pmarketresearch.com

00852-95632430

PW Consulting: www.pmarketresearch.com

Tags

PW Consulting

The Best-reviewed Subdivided Market Risk Analysis Firm in the US and East Asia.