PW Consulting Forecast: Phased Array Antenna Module Market to Reach USD 12,769.18 Million by 2032, Growing at a 17.15% CAGR (Base Year 2025)

Phased Array Antenna Module Market: Strategic Imperatives for 2026 — A PW Consulting Preview

As global defense modernization, satellite connectivity expansion, and next-generation wireless infrastructure converge, phased array antenna modules are rapidly evolving from niche defense components into a broad, cross-sector enabling technology. PW Consulting’s forthcoming Phased Array Antenna Module Market report synthesizes five years of historical performance and a seven-year forecast to deliver the strategic intelligence executives need to make high-consequence decisions in 2026. This preview outlines the report’s practical value, synthesizes market drivers and risks, and explains how leading vendors are shaping the competitive terrain — while preserving the granular segmentation that we reserve for report subscribers.

Phased Array Antenna Module Market

Market Trajectory: Scale, Growth and What It Means for Strategy

Our analysis shows the total phased array antenna module market expanding markedly in the early 2020s and accelerating into the second half of the decade. From the base period we studied, the market reached a multi-billion-dollar scale by the report’s base year, and our forecast indicates continuing strong expansion through 2032 at a compound annual growth rate of approximately 17.15%. This growth trajectory reflects simultaneous demand vectors: defense radar upgrades, high-throughput satellite communications, densification of 5G/early 6G infrastructure, and emergent mobility and industrial radar use-cases.

Phased Array Antenna Module Market

For 2026 specifically, the market’s inflection will be strategic: procurement cycles kicked off in prior years are coming online, semiconductor supply-chain adjustments will begin to show impact, and modular, low-cost architectures are moving from pilot to production. For corporate leaders, that combination creates a window in 2026 for decisive moves — capturing share from legacy incumbents, locking in materials and foundry capacity, and establishing partnerships across software and systems integrators to capture higher margin systems-level revenue.

Phased Array Antenna Module Market

What the PW Consulting Report Delivers — Practical, Transaction-Ready Insights

- Robust market sizing and forward-looking revenue forecasts (historical 2020–2025 baseline, with 2026–2032 scenario outputs) that support budgeting, capital allocation, and M&A valuation workstreams.

- Technology roadmap analysis: maturity curves for AESA, passive arrays, GaN T/R modules, beamformer ICs, and metamaterial/flat-panel approaches, with guidance on adoption timing and risk-adjusted ROI.

- Supply chain and component risk assessments — including semiconductor, packaging, and critical material constraints — with tactical supplier prioritization and inventory hedging playbooks.

- Competitive intelligence pack: capability matrices for prime suppliers, OEM integrators, and specialist component vendors to inform procurement, partner selection, and target screens.

- Regulatory and geopolitical scenario planning: ITAR/EAR implications, tariff sensitivities, and mitigation strategies for export/re-shoring requirements.

- Commercial go-to-market frameworks for new entrants and incumbents — channel strategies, certification roadmaps for defense procurement, and operator integration playbooks for satellite and telco customers.

- M&A and investment theses: valuation sensitivities tied to production cost reductions, modularization, and software-defined beamforming monetization.

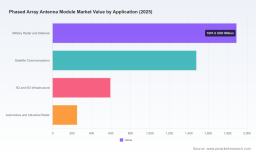

To preserve the “teaser” character of this release, we intentionally withhold the report’s granular regional and application splits in this summary. That level of detail — essential for go/no-go decisions, tender modeling, and target valuation — is available exclusively in the full PW Consulting report and data deliverables.

Competitive Landscape: Who Matters and Why

The phased array module ecosystem combines aerospace primes, RF component specialists, and innovative antenna system startups. Market concentration is meaningful but not prohibitive: the top three players account for a plurality of revenue, and the top five approach a clear majority — a structure that supports both partnerships with large primes and opportunity for differentiated entrants. This blended topology favors firms that can pair system integration scale with fast, low-cost innovations at the module and semiconductor level.

- Prime defense integrators (e.g., Raytheon Technologies, Northrop Grumman, Lockheed Martin, BAE Systems, Leonardo) — These firms bring platform-level contracts, hardened production capability, and established procurement channels. Their modular AESA architectures and digital beamforming investments are shifting unit economics through manufacturing scale and design reuse. For corporate strategy teams, these companies are natural anchors for defense-focused partnerships or targets for tier-2 suppliers seeking volume uplift.

- Systems & communications specialists (e.g., Viasat, Kymeta, C-COM) — These vendors are translating phased array innovations into mobile SATCOM and enterprise broadband products. Their recent product iterations and late-stage developments show clear intent to commercialize flat-panel and metamaterial-based steerable antennas for LEO/GEO multi-orbit support and mobile applications.

- Component and semiconductor enablers (e.g., Analog Devices, Qorvo, Sivers, Kyocera) — Market dynamics at the RFIC and T/R chipset level largely determine cost, power-efficiency, and miniaturization potential. Firms able to deliver GaN-on-Si T/R modules, beamformer ICs, and integrated packaging will capture a disproportionate share of value as phased array modules move from bespoke military builds to higher-volume commercial platforms.

- Specialist innovators (e.g., Requtech, ALCAN Systems, small European startups) — These players advance specific technical vectors — millimeter-wave MCM arrays, liquid-crystal steering, and compact SATCOM modules — that incumbents may license or acquire to accelerate product roadmaps.

Recent industry moves exemplify these dynamics: vendors across the spectrum have either advanced production-modular AESA programs, validated next-gen ground and airborne radar designs, or launched commercially focused flat-panel mobile SATCOM products. These actions accelerate competitive bifurcation: primes compete on platform integration and total-system value, while component specialists and startups compete on size, weight, power, and cost (SWaP-C) innovation.

Risk Environment and Operational Constraints

Strategic planning for 2026 must account for an intertwined set of regulatory, supply-chain and geopolitical risks:

- Export Controls and Certification: ITAR and EAR frameworks materially constrain technology transfer and partner selection for certain high-performance phased array capabilities. Companies operating cross-border must design bifurcated product lines and compliance-first supply chains.

- Semiconductor and Materials Dependence: The sector remains highly sensitive to GaN, GaAs, and specialized silicon RFIC supply. Foundry availability, packaging capacity, and rare-earth exposure are persistent sources of delivery risk and cost volatility.

- Geopolitical Sourcing Pressure: US-China tensions, increased tariffs, and export restrictions raise the cost of doing business and incentivize near-shoring or re-shoring of critical production steps for prime contractors and sovereign procurement customers.

- Technology Transition Risk: Rapid adoption of GaN-on-Si and digitally beamformed architectures offers performance upside but requires capital investment and carries integration risk for legacy product lines.

Actionable Recommendations for 2026 Decision-Makers

Based on our market sizing, concentration analysis, and scenario work, PW Consulting recommends executives consider the following 2026 playbook items:

- Secure semiconductor roadmaps now: Lock multi-year agreements with GaN and RFIC suppliers or invest in captive assembly capacity to stabilize margins and meet ramp schedules.

- Prioritize modular architectures: Shift R&D and product strategy toward modular AESA and software-defined beamforming to shorten time-to-integration across defense and commercial customers.

- Design compliance-first supply chains: Build parallelized product lines and partner structures that comply with ITAR/EAR while enabling exports for commercial SATCOM and telco markets.

- Targeted M&A and JV activity: Acquire or partner with niche innovators that deliver SWaP-C advantages or unique materials science IP — an efficient way to accelerate roadmap delivery without full organic build-out.

- Differentiated go-to-market for commercial segments: For entrants targeting SATCOM or 5G/6G, bundle antenna modules with managed connectivity services or cloud-native beam-management software to expand TAM and capture recurring revenue.

- Regulatory and scenario drills: Run procurement and program scenarios that model tariff impacts, export curbs, and supplier outages to stress-test capital and production plans through 2032.

Why PW Consulting’s Report Matters for 2026

Decisions made in 2026 about factory footprint, partner selection, product modularity, and M&A will lock-in market position for the remainder of the decade. PW Consulting’s report translates high-level market momentum (a sustained CAGR in the mid-teens) into operationally relevant actions: which components to secure, which partnerships to prioritize, where to expect price compression, and how to structure offers that convert platform-level demand into sustainable margins.

Beyond forecasts, our deliverables include a prioritized vendor short-list, a regulatory risk heatmap, and a scenario-based valuation model that corporate development teams can adapt directly to acquisition screens and bidding strategies. For product and commercial leaders, the technology adoption timelines and integration cost curves in the report provide a roadmap for sequencing launches across defense, SATCOM, and telco markets.

Next Steps and How to Access the Full Intelligence

This preview highlights strategic themes and tactical imperatives but intentionally omits the detailed regional, application, and technology split tables that underpin procurement modeling and target valuation. Those critical datasets — along with interactive forecast tools and vendor benchmarking matrices — are included in the full PW Consulting Phased Array Antenna Module Market report and the accompanying Excel data pack.

Contact PW Consulting to request the full report, bespoke briefings for your leadership team, or a tailored deep-dive workshop to translate market forecasts into an actionable 18–36 month roadmap. In an environment where supply constraints, regulatory friction, and rapid technology change intersect, the right intelligence — and the right timing — will determine who leads the phased array era.

For detailed analysis of this topic, please visit the official page: Phased Array Antenna Module Market

Lacy Lee

Senior Marketing Manager

sales@pmarketresearch.com

00852-95632430

PW Consulting: www.pmarketresearch.com

Tags

PW Consulting

The Best-reviewed Subdivided Market Risk Analysis Firm in the US and East Asia.