PW Consulting Forecast: Ion Chromatography Column Market to Climb from USD 512.5 Million in 2025 to USD 833.8 Million by 2032 at a 7.24% CAGR

Ion Chromatography Column Market — Strategic Outlook for 2026 Decision-Makers

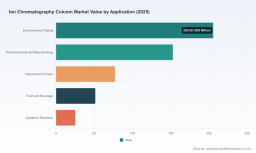

PW Consulting’s latest market study on the Ion Chromatography (IC) Column market furnishes actionable intelligence for senior leaders planning capital allocation, product strategy, and commercial tactics in 2026. Built on a 2020–2025 historical baseline and a 2026–2032 forecast horizon, the study synthesizes primary interviews, proprietary shipment data, and supplier financials to produce a rigorous market view: the global IC column market expands from a 2025 base of USD 512.5 Million to an anticipated USD 833.8 Million by 2032, reflecting a compounded annual growth rate (CAGR) of 7.24% over the forecast period.

Ion Chromatography Column Market

Why this report matters for 2026 decisions

2026 will be a pivot year for equipment manufacturers, consumables providers, laboratory networks, and investors in analytical technologies. The IC column market is not only growing steadily; it is being reshaped by regulatory validation, automation of routine workflows, and a shift toward consumables-as-a-service models. Our report translates these macro trends into decision-ready insights — enabling procurement leads to rationalize supplier portfolios, R&D heads to prioritize platform investments, and corporate strategy teams to size acquisition targets with confidence.

Ion Chromatography Column Market

Core findings you can act on

- Growth trajectory and investment horizon: The market’s projected scale through 2032 underpins multi-year investment cases for automated IC platforms, column innovations (chemistries and lifetime improvements), and aftermarket services. A clear decadal revenue runway combined with predictable consumables replacement rates creates compelling annuity opportunities for incumbents and new entrants alike.

- Market structure: The market displays high concentration among a few global vendors, indicating structural advantages for scale, distribution, and after-sales networks. This concentration informs competitive moves — premium pricing and bundled services are sustainable in many segments, while niche product differentiation remains an entry path for focused players.

- Regulatory momentum: Recent compendial and regulatory developments — including broader acceptance of IC in pharmaceutical compendia and well-documented compliance pathways for environmental methods — are increasing buyer comfort and expanding procurement mandates across regulated industries.

- Product and workflow innovation: Compact automated IC systems and integrated software platforms are accelerating adoption outside core analytical labs (e.g., water utilities, decentralized QC). These innovations are shortening validation cycles and reducing operator skill requirements.

Practical contents of the report

Rather than abstract forecasts alone, the report provides operational tools that finance, product and commercial teams can apply immediately:

Ion Chromatography Column Market

- Market-sizing methodology and sensitivity analysis that highlight upside/downside scenarios for supply shocks, regulatory change, and faster-than-expected adoption of automation.

- Vendor scorecards and positioning matrices that assess technical breadth, service footprint, IP strength, and go-to-market models for leading suppliers.

- Buy-side decision frameworks (vendor selection, TCO modeling, and consumables procurement playbooks) tailored to common purchaser archetypes: environmental labs, pharmaceutical QC, food & beverage testing, industrial process control, and academic research.

- Product roadmaps and R&D prioritization checklists focusing on column chemistries, lifetime extension, and compatibility with low-maintenance automated IC systems.

- Regulatory matrix mapping methods to compendial acceptance, environmental standards, and data-integrity requirements (including electronic record compliance for regulated labs).

- Commercial tactics — subscription pricing pilots, spare-parts logistics, and a modular service offering blueprint to increase Customer Lifetime Value (CLV).

Competitive landscape — what leading players are doing

The markets’ top vendors demonstrate distinct strategic postures which inform competitor response and partnership strategies:

- Thermo Fisher Scientific — leverages a broad chromatography portfolio and strong OEM relationships. Its established IonPac and CarboPac brands remain reference standards for many regulated buyers. Strategy implication: competitors should emphasize specialized value-adds (faster validation kits, local support) to counter Thermo Fisher’s scale.

- Metrohm AG — entrenched in regulatory workflows and environmental testing, with documented compliance to key EPA methods and ISO standards. Strategy implication: partnership or co-marketing with Metrohm can accelerate acceptance in regulated verticals; alternatively, competing vendors must demonstrate method equivalency and local validation support.

- Shimadzu Corporation — advancing compact, automated platforms designed for streamlined water-quality testing; a March 2026 product launch underscores the push toward turnkey, low-footprint solutions. Strategy implication: incumbents and system integrators must either match the automation ease or pivot to differentiated high-throughput offerings.

- Agilent Technologies — benefits from an integrated LC/HPLC portfolio that simplifies multi-modal labs’ procurement. Strategy implication: small and medium suppliers can exploit gaps in price/performance or faster order-to-delivery cycles.

- Regional and specialist players (SHINE, Shodex, Tosoh, Bio‑Rad, GL Sciences) — combine niche IP, localized manufacturing, and cost-competitive offerings. Strategy implication: these firms are the primary source of disruptive pricing and targeted application innovation; strategic buyers should evaluate them for local sourcing and co-development partnerships.

Regulatory and standards landscape: implications for suppliers and buyers

Regulatory clarity has been a catalyst. Key developments include compendial acceptance of ion chromatography methods for pharmaceutical assays, environmental method compliance by major system vendors, and the persistent requirement for data integrity and 21 CFR Part 11–compliant software in regulated environments. These forces create a two-speed market: vendors that can provide validated methods, compliant software, and clear change-control packages will secure larger, risk-averse customers; others will compete on cost and speed-to-qualification.

Strategic imperatives for 2026

- Prioritize automation and software compliance: Investing in compact, automated platforms and validated software stacks reduces buyer friction and shortens procurement cycles. For OEMs, embedding validated workflows and offering validation documentation as part of the product reduces adoption barriers.

- Monetize consumables: The recurring-revenue nature of columns, guard columns, and replacement parts supports subscription or managed-consumables models. Build logistics and replenishment capabilities to convert installed base into predictable revenue.

- Focus M&A and partnership activity on capability gaps: Given market concentration, acquisitions that extend service footprint, local manufacturing, or software capability are high-impact. Mid-tier players can use targeted M&A to leapfrog into regulated verticals.

- Segmentation-led go-to-market: Tailor offers to buyer archetypes: turnkey systems and training for municipal water customers; validated kits and change-control documentation for pharmaceutical QC; and cost-competitive consumables for industrial providers.

- Defend against low-cost disruption with differentiated service: Manufacturers in regions with higher cost bases should emphasize faster lead times, method support, and warranty/service SLAs rather than competing purely on price.

- Build supply-chain resilience: Secure critical chemistries, diversify suppliers for key components, and maintain strategic safety stock for consumables to avoid revenue volatility during raw-material or logistics disruptions.

Risks and near-term shock scenarios

Our scenario modeling flags several downside risks that should influence 2026 contingency plans: accelerated entry of low-cost manufacturers reducing margins in commoditized column types; sudden regulatory shifts requiring method requalification; and component supply constraints that lengthen lead times. Conversely, upside scenarios include faster adoption of decentralized testing and expanded regulatory mandates for routine monitoring that would expand market volumes materially.

How to use this intelligence in boardroom debates

- Use the report’s validated top-line projections and sensitivity cases to stress-test capital allocation for new product platforms and factory expansions.

- Leverage vendor scorecards to prioritize partnership targets and to inform supplier consolidation or diversification decisions.

- Apply the TCO and procurement playbooks during vendor RFPs to capture hidden lifecycle costs and service revenue potential.

- Integrate regulatory mapping into product development timelines to minimize time-to-market for regulated buyers.

Next steps

PW Consulting’s Ion Chromatography Column Market report is designed as a practical toolkit for 2026 strategy: it provides the quantitative backbone (historical and forecast market sizing, concentration metrics), qualitative competitive analysis, and hands-on operational frameworks needed to convert market growth into profitable action. To preserve the strategic value of granular segmentation and supplier benchmarking, the report intentionally reserves detailed split tables and supplier scorecards for the full study. Interested executives should request the complete report to access the segmented intelligence, vendor scorecards, and downloadable tools that support board-level investment decisions.

For detailed analysis of this topic, please visit the official page: Ion Chromatography Column Market

Lacy Lee

Senior Marketing Manager

sales@pmarketresearch.com

00852-95632430

PW Consulting: www.pmarketresearch.com

Tags

PW Consulting

The Best-reviewed Subdivided Market Risk Analysis Firm in the US and East Asia.