PW Consulting Predicts Lacrimal Stent Tube Market to Expand at a 5.48% CAGR

Lacrimal Stent Tube Market: Strategic Imperatives for 2026 — PW Consulting Official Release

PW Consulting today releases an executive briefing derived from our forthcoming comprehensive market study on the global lacrimal stent tube market. This briefing outlines why 2026 is a pivotal year for companies operating in this niche of ophthalmic and ENT surgery, highlights headline market trajectories, and summarizes the practical, decision-ready content contained in the full report. The release follows a “trailer” principle: we demonstrate depth and actionable orientation while reserving granular segmentation and proprietary models for the full report.

Lacrimal Stent Tube Market

Executive snapshot: Where the market stands

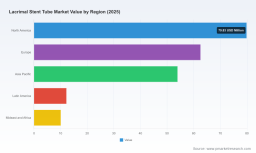

The lacrimal stent tube market is a stable growth niche within ophthalmic surgical devices. PW Consulting’s base-year assessment (2025) places the global market at approximately USD 218.5 Million, with a forecast compound annual growth rate (CAGR) of roughly 5.48% over the 2026–2032 horizon. Our modeled trajectory anticipates continued expansion through practical adoption of established silicone technologies, incremental uptake of specialty material tubes, and sustained procedural volumes driven by both congenital and acquired indications.

Lacrimal Stent Tube Market

Why 2026 is a strategic inflection point

- Regulatory momentum and reimbursement clarity — Most lacrimal stents and intubation sets qualify as FDA Class II devices with 510(k) pathways. CPT coding (notably codes covering probing with insertion of a tube or stent) provides an established reimbursement framework that reduces commercialization friction for iterative device improvements.

- Product maturity, not disruption — Silicone remains the dominant material due to proven biocompatibility and manufacturing familiarity. That maturity creates predictable adoption patterns but also compresses margins unless manufacturers differentiate through clinical evidence, workflow efficiency, or cost leadership.

- Consolidation potential — Market concentration metrics show a market where top-three and top-five firms command material shares, creating an environment where mid-size players face strategic choices: specialize and defend, seek partnership, or pursue M&A to scale distribution and R&D capabilities.

Headline competitive dynamics

The competitive landscape blends specialist manufacturers with larger ophthalmic device players. Leading and active participants include companies such as FCI Ophthalmics, Kaneka Medical’s eye division, bess medizintechnik gmbh, Aurolab, Gunther Weiss Scientific Glassblowing, and Beaver-Visitec International (BVI Medical). Collectively, incumbents have developed portfolios that span self-retaining bicanalicular systems, monocanalicular solutions, and specialty bypass tubes for CDCR procedures.

Lacrimal Stent Tube Market

- FCI Ophthalmics continues to emphasize product breadth across self-retaining and monocanalicular systems, leveraging clinical visibility through society presentations and product theater engagements.

- Kaneka’s LACRIFLOW and LACRIFAST product lines reflect an emphasis on hydrophilic coatings and user ergonomics tuned to congenital and acquired obstruction use cases.

- Regional specialists and manufacturers (including European and Indian producers) sustain supply diversity while leveraging cost and access advantages in specific markets.

- Glass-based specialty tubes for lacrimal bypass remain a distinct sub-niche served by highly specialized manufacturers with long-established craftsmanship.

PW Consulting’s market concentration analysis highlights that the market is not perfectly atomized: the leading three firms capture a meaningful portion of market value, and the top five extend that share further. For strategists, this underscores the importance of clear differentiation or alliance strategies to avoid margin compression.

What the full report contains — practical modules for 2026 decision-making

The PW Consulting report is built to be operationally useful for commercial leaders, business development teams, and corporate strategists. Key modules include:

- Market sizing and forecast model — Rolling historical series and scenario-based projections through 2032, with sensitivity analysis for procedure volumes, device mix, and pricing pressure.

- Commercial playbooks — Go-to-market pathways for hospitals, ambulatory surgery centers, and outpatient clinics, including tender tactics, KOL engagement templates, and value messaging for payers.

- Regulatory and reimbursement roadmap — Practical checklists for 510(k) submissions, sterility validation expectations, and reimbursement coding strategies to optimize product launches.

- Manufacturing & supply chain guidance — Sterilization strategy options (radiation and alternative validated approaches), cost benchmarking, and quality system considerations for single-use, sterile-labeled devices.

- Clinical evidence and trial design playbook — Recommended endpoints, comparative study frameworks, and real-world evidence strategies to support adoption and premium positioning.

- Competitive intelligence dossiers — Strategic profiles and capability maps of the main participants, synthesis of recent portfolio moves, and play-by-play coverage of product launches and clinical presentations.

- M&A and partnership decision framework — Valuation heuristics, integration risk checklists, and prioritization matrices for acquiring distribution, manufacturing, or technology capabilities.

Regulatory, reimbursement and materials — what matters for 2026

- 510(k) as the default route: The majority of lacrimal stent products use the 510(k) pathway; early engagement with regulatory bodies can streamline clearances for incremental improvements.

- Reimbursement is established but local: CPT coding for probing with tube insertion reduces uncertainty, yet reimbursement levels and payer behavior vary by market — active payer engagement yields better commercial outcomes.

- Material selection remains strategic: Silicone’s dominance is both an enabler and a constraint — it reduces technical risk but raises the bar for differentiation. Manufacturers should weigh coating technologies, delivery mechanisms, and instrument ergonomics as primary differentiators rather than raw substrate alone.

- Sterility and single-use expectations: Market practice favors sterile, single-use devices with validated sterilization processes; investment in robust sterilization validation is non-negotiable for market access.

Actionable strategic priorities for 2026

For companies planning resource allocation in 2026, PW Consulting recommends a focused set of initiatives that balance near-term commercialization with medium-term differentiation:

- Prioritize evidence generation: Sponsor pragmatic clinical studies that align with payer and clinician decision criteria (e.g., time-to-patency, complication rates, patient-reported outcomes). Real-world registry data can accelerate adoption where randomized trials are infeasible.

- Refine product hierarchy: Segment portfolios into core commodity-stent offerings and premium differentiated systems (coatings, deployment tooling, integrated consumables) to avoid margin compression across the board.

- Strengthen sterilization and manufacturing economics: Consolidate suppliers and validate cost-effective sterilization pathways to protect margins while meeting single-use sterility expectations.

- Invest in targeted commercial channels: Map high-return submarkets (by care setting and clinical pathways) and allocate sales resources to centers of excellence and high-volume ASCs rather than a broad, undifferentiated field force.

- Explore selective partnerships: Where scale is limiting, consider distribution alliances or co-marketing with regional manufacturers to accelerate penetration without full acquisition risk.

- M&A with integration discipline: If pursuing inorganic growth, prioritize targets that offer either distribution breadth, manufacturing capability, or unique clinical IP. Use valuation discipline and integration scorecards to preserve margins.

Scenarios & risks — what could change the story

- Downside pressure: Accelerated commoditization or aggressive price competition could erode near-term revenue growth, compressing the otherwise steady CAGR trajectory.

- Upside levers: Demonstration of superior clinical outcomes or the introduction of workflow-saving delivery systems could justify premium pricing and faster market capture.

- Regulatory shocks: Changes to device classification or new sterilization requirements in key markets would materially affect time-to-market and unit economics.

- Supply chain concentration: Single-source sterilization or raw-material constraints could create temporary shortages; diversified sourcing mitigates this risk.

Competitive moves to watch (short list)

Recent market activity signals priorities among incumbents: portfolio strengthening by full-service ophthalmic surgery suppliers, persistent clinical presentations from product-focused specialists, and ongoing efforts to improve procedural ergonomics and patient comfort. PW Consulting’s monitoring shows several mid-size competitors accentuating lacrimal portfolios as a route to broader ophthalmic relevance — a trend that affects partnership and acquisition targets in 2026.

How PW Consulting’s report supports 2026 corporate decisions

Our full report equips executives with the models, playbooks, and evidence templates required to make informed 2026 investments. It translates market sizing into prioritization matrices, links regulatory steps to launch timelines, and maps competitive moves to recommended defensive and offensive actions. The report’s scenario-based financial model allows management teams to stress-test product launches, pricing strategies, and M&A options under multiple plausible futures.

Next steps and where to get the full intelligence

This briefing intentionally highlights strategic insight while withholding proprietary segment detail and the full forecast model to preserve the value of the comprehensive report. Companies seeking the complete dataset, granular segmentation, downloadable forecast models, and the full suite of commercial playbooks are invited to access the full Lacrimal Stent Tube Market report via PW Consulting’s research portal. The full package is designed for immediate operational use by commercial, regulatory, and corporate development teams preparing 2026 budgets and roadmaps.

For media inquiries, licensing of the full report, or to schedule a brief with PW Consulting’s lacrimal market practice, please contact our client services team via the PW Consulting website.

For detailed analysis of this topic, please visit the official page: Lacrimal Stent Tube Market

Lacy Lee

Senior Marketing Manager

sales@pmarketresearch.com

00852-95632430

PW Consulting: www.pmarketresearch.com

Tags

PW Consulting

The Best-reviewed Subdivided Market Risk Analysis Firm in the US and East Asia.