PW Consulting: Refrigeration Packaging Market Set to Expand at 8.42% CAGR Through 2032, Led by Asia‑Pacific Demand

Refrigeration Packaging Market: Strategic Insights for 2026 Decision‑Makers

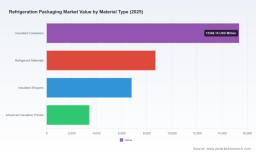

PW Consulting’s latest Refrigeration Packaging Market report equips executives and investors with the foresight needed to make high‑stakes decisions in 2026. The refrigeration packaging market has moved from approximately USD 23,050.4 million in 2020 to USD 34,250.6 million in 2025 and is projected to expand at a compound annual growth rate (CAGR) of 8.42% through our forecast window, reaching an estimated USD 60,316.2 million by 2032. This directional momentum, coupled with evolving regulatory and raw‑material dynamics, creates a narrow time window in which product, sourcing and commercial choices made now will materially affect margin and market position over the remainder of the decade.

Refrigeration Packaging Market

Why this report matters for 2026 strategic planning

- Translate growth vectors into actionable bets: identify product categories and commercial models that will capture outsized share as refrigeration needs scale across pharma, perishables and industrial cold chains.

- Stress‑test supplier and design choices against near‑term raw material volatility and emerging Extended Producer Responsibility (EPR) regimes.

- Prioritize investments in service capabilities (e.g., local service centers, testing labs) that accelerate customer adoption while de‑risking logistics lead times.

- Frame M&A and partnership screens around capability gaps—especially reusable systems, small‑format parcel innovation, and advanced insulation technologies.

- Derive price and contract strategies that preserve margin when input cost cycles or regulatory fees compress profitability.

What you will find in the report (practical, execution‑focused)

- An integrated market model (2020–2032) with scenario outputs you can plug into internal financial planning; the model quantifies topline and demand sensitivity to key drivers.

- Supplier and capability scorecards that evaluate manufacturing scale, service network density, material flexibility and regulatory readiness.

- Cost pass‑through and margin sensitivity analyses for common packaging constructions, with levers you can apply to contract clauses and procurement hedging.

- Playbooks for commercialization in parcel and palletized channels, including go‑to‑market templates for reusable vs. single‑use offerings.

- Operational checklists and test‑protocol summaries (thermal performance, drop and vibration, reusability lifecycle) to accelerate qualification cycles.

- M&A and inorganic growth frameworks that prioritize targets by capability, geography and integration risk—scored for short‑term accretion and long‑term strategic fit.

- A regulatory and sustainability roadmap that maps EPR and recycling incentives to product redesign priorities and cost recovery pathways.

Market dynamics: cost, regulation and innovation pressures

Raw material inputs and packaging regulations are converging to create a tighter, more complex decision environment in 2026. Recent raw material indicators show sustained pressure in foam and polymer segments: the U.S. Producer Price Index for Polystyrene Foam Product Manufacturing was registered at 330.084 in February 2026; North American polyurethane prices averaged roughly USD 3.24 per kilogram in early 2026; and Expandable Polystyrene (EPS) was trading near USD 1.89 per kilogram in March 2026. These inputs underscore the need for active cost management—indexation clauses, multi‑sourcing and material substitution pilots are no longer optional.

Refrigeration Packaging Market

Regulatory change compounds this complexity. As of early 2026, seven U.S. states have enacted packaging EPR laws that shift end‑of‑life obligations to producers, with fee structures and reporting requirements already being implemented in several jurisdictions. Those programs create both cost liabilities and competitive advantages: companies that design for reuse and curbside recyclability can minimize producer fees and capture sustainability‑driven procurement wins.

Refrigeration Packaging Market

At the same time, technological innovation—ranging from phase‑change materials optimized for narrow parcel profiles to advanced insulation panels for long‑haul palletized shipments—is reshaping product economics. The net effect is a market that rewards integrated offerings (product + service + circularity) and penalizes single‑dimension solutions.

Competitive landscape: who is shaping the market

The refrigeration packaging market exhibits a fragmented structure: market concentration metrics indicate top‑three players account for roughly 18.5% of market value and the top‑five near 27.9%, leaving meaningful room for mid‑sized and specialist players to scale. Our competitive review highlights strategic postures and capability differentials among the leading players you should track.

- Sonoco ThermoSafe — A global leader in temperature‑controlled packaging and cold‑chain consulting, with deep expertise in pharmaceutical and biologic logistics. Their combination of engineering services and product breadth positions them as a preferred partner for complex qualification programs.

- Insulated Products Corporation (IPC) — A high‑volume manufacturer focused on cost‑effective insulated liners and curbside‑recyclable paper‑based solutions. IPC is a playbook leader for scale production and low‑cost disposable solutions serving e‑commerce and short‑duration cold chains.

- Cryopak — Differentiates through vertical integration (materials, engineering, testing) and a broad portfolio that spans parcel to pallet applications. Their testing and conversion capabilities accelerate customer qualification timelines.

- Pelton Shepherd Industries — A specialist in gel and ice packs with a growing emphasis on sustainable formulations. Their product depth makes them an attractive partner for refrigerated shippers seeking turnkey cold packs.

- Peli BioThermal — Strength in reusable shippers and global service centers; recent capacity expansions reflect a bet on reusable systems for the pharmaceutical cold chain.

- Cold Chain Technologies (CCT) — Notable for recyclable parcel shippers and reusable pallet solutions targeted at life sciences; strong in compliance‑driven supply chains.

- Nordic Cold Chain Solutions — Smaller, innovation‑led player notable for launching a GLP‑1 & Small‑Format Packaging Innovation Lab in March 2026, a signal of intensive focus on parcel‑scale pharmaceutical demand.

- Sealed Air Corporation & Amcor plc — Large, diversified packaging players applying foam and film technologies to refrigeration applications while pushing sustainability roadmaps at scale.

Recent corporate moves underline the strategic priorities in 2026: Peli BioThermal expanded its Allentown service center in late 2025 to increase throughput for reusable shippers, while Nordic’s lab launch in March 2026 signals investment in small‑format, high‑value pharmaceutical parcel solutions. These investments demonstrate what winning looks like—capability density near customer points of use, combined with R&D that shortens qualification timelines.

Strategic imperatives for manufacturers, logistics providers and investors

- Design with circularity as a default: incorporate reuse, recyclability and end‑of‑life cost modeling into product development to mitigate EPR fees and capture procurement preference.

- Adopt a hybrid supply strategy: combine low‑cost disposable lines with premium reusable offerings to span multiple customer value points and protect against input price swings.

- Invest in local service and testing capacity: service centers and innovation labs materially shorten qualification cycles and increase customer switching costs.

- Negotiate smarter commercial terms: build input‑indexation and lifecycle charges into contracts to preserve margin across raw‑material cycles and regulatory fee introduction.

- Target bolt‑on M&A to accelerate capability in high‑growth microsegments (e.g., small‑format pharma parcel systems, advanced insulation panels, and circular materials conversion).

- Operationalize sustainability as a profit lever: quantify producer fee avoidance and procurement uplift rather than treating sustainability as a cost center.

How to use PW Consulting’s report in 2026 decision cycles

CEOs and boards: use the report’s scenario suite to align capital allocation and M&A priorities with the most probable market trajectories.

Procurement leaders: apply the supplier scorecards and cost pass‑through templates to renegotiate terms that share input risk and accelerate dual‑sourcing where appropriate.

Product and R&D teams: adopt the testing‑protocol appendices and lifecycle calculators to compress time‑to‑market for reusable solutions and recyclable alternatives.

Investors and corporate development: use the M&A scoring frameworks and target shortlists to accelerate inorganic roll‑ups in under‑consolidated niches.

Next steps and how to access the full intelligence

This release is a strategic preview designed to surface key directional insights and the frameworks you can apply in 2026. To preserve the commercial value of the full analysis, we have intentionally withheld the granular sub‑segment tables and regional/application splits that underpin our model. PW Consulting’s full report includes those decompositions, the downloadable market model, company scorecards, and transaction‑ready diligence materials.

Contact PW Consulting or visit our report page to access the complete Refrigeration Packaging Market research package and the accompanying Excel model. For teams prioritizing tactical execution this year, commissioning our rapid‑turn strategy workshop will convert these insights into a 90‑day implementation roadmap tailored to your portfolio.

For detailed analysis of this topic, please visit the official page: Refrigeration Packaging Market

Lacy Lee

Senior Marketing Manager

sales@pmarketresearch.com

00852-95632430

PW Consulting: www.pmarketresearch.com

Tags

PW Consulting

The Best-reviewed Subdivided Market Risk Analysis Firm in the US and East Asia.