PW Consulting: Pathogen Detection Market Set to Reach USD 9,499.07 Million by 2032

Pathogen Detection Market — 2026 Strategic Preview

Executive summary

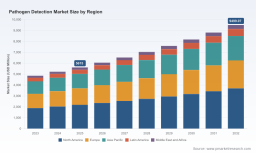

As public health systems, food-supply chains, and pharmaceutical manufacturers continue to prioritize rapid, reliable microbial identification, the global pathogen detection market remains on a robust growth trajectory. Our latest market modelling — based on a 2025 base year and a detailed 2026–2032 forecast horizon — projects sustained expansion at a compound annual growth rate of 7.8%. The market, already measured in multi‑billions of USD (USD Million basis), is positioned to approach a near‑doubling of scale by the end of the forecast window. For enterprise leaders planning capital allocation and commercial strategy in 2026, the implications are clear: act now to secure platform leadership, protect supply chains, and align reimbursement- and regulatory-focused commercialization pathways.

Pathogen Detection Market

Why this preview matters for 2026 decision-makers

-

Clarity on macro momentum: Investors and corporate strategy teams need a defensible view of market growth and structural drivers to justify R&D and M&A commitments. Our forecast provides that top‑line trajectory and the scenario analysis executives require to stress‑test budgets.

Pathogen Detection Market -

Regulatory and reimbursement inflection points: Evolving policies materially change the economic calculus for point‑of‑care (POC) versus centralized laboratory offerings. Understanding these inflection points is a prerequisite for product prioritization and commercial contracting in 2026.

Pathogen Detection Market -

Competitive positioning under consolidation pressure: With a moderately concentrated vendor landscape, selective M&A or partnership activity can be a faster path to scale than organic expansion in many geographies and use cases.

Market dynamics shaping 2026 strategy

The market’s expansion is being driven by persistent infectious-disease surveillance needs, rising adoption of molecular and syndromic panels, and an uptick in routine screening across clinical, food safety, pharmaceutical QC, and environmental applications. Two regulatory and reimbursement signals demand particular attention:

-

Point‑of‑care enablement: Regulatory frameworks that permit CLIA-waived operation materially broaden addressable markets in outpatient and near-patient settings. Companies with POC-capable platforms should prioritize pathways to achieve and advertise such status.

-

Reimbursement updates: Recent adjustments to procedural coding and reimbursement levels for key pathogen assays alter unit economics for rapid molecular tests. Commercial teams must recalibrate pricing, contracting, and value‑dossier content to sustain margins under new fee schedules.

Supply chain risk remains a second‑order but persistent force: medical‑grade reagents and consumables experienced material cost pressure in recent years, necessitating procurement strategies that include long‑term supplier agreements, local buffering, and re‑engineering of consumable formats to reduce dependency on single‑source plastics and reagents.

Technology and use‑case imperatives

Technological differentiation continues to bifurcate along two vectors: speed/portability versus depth and multiplexing. Rapid, near‑patient molecular platforms compete with high-throughput, laboratory‑centric systems and emerging sequencing-based approaches that unlock pathogen discovery and antibiotic resistance profiling. For 2026, leaders must decide where to play along these vectors — and how to sequence investments across platform upgrades, consumable roadmaps, and clinical validation programs.

-

POC and rapid molecular: Prioritize CLIA‑waived pathways, user experience design, and rapid reimbursement capture.

-

Multiplex syndromic assays: Invest in clinical evidence generation for multiplex panels that reduce downstream healthcare costs.

-

Sequencing and bioinformatics: Build partnerships to transition NGS from tertiary labs into actionable surveillance and outbreak response use cases.

Competitive landscape — what to watch in 2026

The vendor ecosystem features a mix of established platform incumbents, instrument-focused OEMs, and niche innovators. The market concentration indicates notable leadership by a few firms, but meaningful room remains for disruptive entrants in specialized segments. Key players demonstrate different routes to growth:

-

Platform incumbents with broad portfolios (examples include well‑known global diagnostics firms): Their strengths are integrated instrument-consumable franchises, established clinical relationships, and scale distribution networks. Their playbook typically emphasizes expanding menu breadth, improving throughput, and cross‑selling into existing installed bases.

-

Rapid POC specialists: Companies focused on single‑analyte or small-panel rapid systems have pursued regulatory clarity and strategic hospital distribution partnerships to penetrate acute-care channels quickly.

-

Multiplex and syndromic vendors: Firms offering comprehensive multiplex panels aim to capture value by simplifying diagnostic algorithms across respiratory, GI, and sexually transmitted infection (STI) indications.

-

Innovators in isothermal amplification, sequencing and mass spectrometry: These players compete on novel assay formats, lower reagent dependencies, or superior analytic breadth, and they are attractive targets for larger diagnostic OEMs seeking technology refresh.

Recent vendor developments reinforce these narratives: platform regulatory clearances and CE marks for point‑of‑care tests accelerated product availability; targeted product launches expanded multiplex capabilities; and selective distribution agreements strengthened hospital adoption pathways. Positive clinical validation data for established assays continue to reduce perceived adoption risk and accelerate procurement cycles.

Strategic plays for 2026

We advise executives to consider the following strategic options, prioritized by expected impact and feasibility over a 12–24 month horizon:

-

Prioritize regulatory investments that unlock new channels: Securing CLIA‑waived status or equivalent local approvals can multiply addressable markets without proportionate CAPEX increases.

-

Hedge consumable risk through supplier diversification and design for supply resilience: Reagent reformulation and alternative consumable suppliers reduce margin volatility from raw‑material shocks.

-

Adopt a layered commercialization strategy: Use channel partners for breadth (e.g., distribution alliances in acute care) while deploying a direct sales model in high‑value markets to retain margin and clinical engagement.

-

Targeted M&A or licensing to fill menu gaps: Given the concentration dynamics, acquiring niche multiplex panels or bioinformatics capabilities may be faster and more cost‑effective than building internally.

-

Embed health‑economic evidence early: Reimbursement leverage grows when companies can demonstrate cost avoidance across patient pathways; invest in prospective health‑economic studies concurrent with pivotal clinical validation.

What our report delivers — practical contents for 2026 execution

This report is designed as an operational toolkit for executives and investment committees. Highlights include:

-

Top‑down and bottoms‑up market forecasts across the 2026–2032 horizon with scenario sensitivity and clearly documented assumptions.

-

Technology adoption curves and a use‑case matrix that maps assay formats to clinical, food safety, pharmaceutical, and environmental workflows.

-

Vendor benchmarking and scorecards covering product portfolios, regulatory status, commercial reach, and innovation pipelines — enabling rapid competitor comparisons without the need for bespoke primary research.

-

Regulatory and reimbursement heatmaps, including action steps to achieve CLIA‑waived status and to capture recent reimbursement updates.

-

Supply‑chain risk matrix and mitigation playbook addressing reagent and consumable cost inflation, alternate sourcing strategies, and inventory policies.

-

M&A and partnership screening criteria, with shortlists of archetypal targets for tuck‑in and capability acquisitions (commercial, assay, or analytics).

-

Commercial deployment templates: pricing calculators, contracting playbooks for hospital networks, distributor scorecards, and value‑dossier outlines tailored for payors and procurement teams.

How to use this intelligence in 2026 planning cycles

Executives should incorporate the report into three core corporate processes:

-

Annual investment committee reviews: Use the forecast scenarios to stress test R&D and production investments under different reimbursement and supply‑chain states.

-

Product roadmapping: Map required clinical trials, regulatory milestones, and consumable‑scale planning to the prioritization framework included in the report.

-

M&A diligence: Apply the vendor scorecards and valuation frameworks to screen and value targets quickly, reducing due‑diligence timelines and transaction execution risk.

Conclusion — the strategic vantage point for 2026

The pathogen detection market offers both scale and strategic depth: it rewards companies that can align regulatory strategy, platform investments, and supply‑chain resilience with payer economics and clinical workflows. With compound growth reinforcing the market’s attractiveness, 2026 represents a pivotal year to convert strategic intent into operational advantage. Our Pathogen Detection Market report provides the analytical scaffolding and executable playbooks that senior leaders need to make those decisions with confidence.

Next steps

This preview surfaces the decision‑critical insights and practical deliverables. For the full, granular intelligence — including detailed segment breakdowns, regional demand models, product‑level revenue estimates, and downloadable financial models — please visit our report page to access the complete study and supporting datasets.

For detailed analysis of this topic, please visit the official page: Pathogen Detection Market

Lacy Lee

Senior Marketing Manager

sales@pmarketresearch.com

00852-95632430

PW Consulting: www.pmarketresearch.com

Tags

PW Consulting

The Best-reviewed Subdivided Market Risk Analysis Firm in the US and East Asia.