PW Consulting Predicts Solid State Cooling Market to Expand at a Robust 12.48% CAGR Through 2032

Solid State Cooling Market 2026: Strategic Imperatives from PW Consulting’s Latest Industry Brief

As enterprises recalibrate capital allocation and technology roadmaps for 2026, PW Consulting’s new Solid State Cooling Market report delivers a tightly focused evidence base for decisions that will determine competitive positioning in a fast-evolving thermal management landscape. Our analysis synthesizes a six‑year historical series (2020–2025) with forward-looking scenarios for 2026–2032. At the macro level, the market expanded from roughly USD 510 million in 2020 to approximately USD 887 million in 2025 and is projected to exceed USD 2.0 billion by 2032, reflecting a compound annual growth rate of 12.48% across the forecast window. These topline dynamics underscore a transition from niche adoption to broad, commercially meaningful deployment — but the path forward is heterogeneous and strategically nuanced.

Solid State Cooling Market

Why this matters for 2026 decisions

-

Timing of investments: The mid‑2020s represent a pivotal inflection point. Growth momentum and improving device economics mean that green‑field product launches, capacity expansions, and targeted R&D bets made in 2026 will determine whether an organization captures early mover advantages or is relegated to a fast‑followers’ role.

Solid State Cooling Market -

Technology-risk calibration: Breakthroughs in materials science and device architecture are accelerating performance improvements. Corporates that integrate technology scouting and adaptive IP strategies into 2026 planning will be better positioned to capture disruptive efficiency gains without overcommitting to legacy designs.

Solid State Cooling Market -

Regulatory arbitrage and sustainability narratives: Intensifying regulatory pressure on HFC refrigerants and the rising cost of compliance for traditional vapor‑compression systems create a window for solid‑state solutions to gain preference in regulated or sustainability‑sensitive procurements. Procurement teams should embed regulatory scenarios into supplier selection models starting in 2026.

Report contents — practical deliverables for boards and operating teams

-

Topline market sizing and validated forecast model: Year‑by‑year market projections (2020–2032) with scenario overlays and sensitivity testing tailored to macroeconomic and materials‑price shocks.

-

Value chain and cost‑curve analysis: End‑to‑end maps showing component cost dynamics, critical suppliers of thermoelectric semiconductors, and downstream integration points for consumer, industrial, healthcare, and automotive OEMs.

-

Competitive intelligence and capability matrix: Strategic profiles of incumbent and challenger vendors, mapped against technology stack, go‑to‑market reach, and partnership openness.

-

Commercial playbooks: Tailored GTM approaches for system integrators, OEMs, and Tier‑1 suppliers, including channel strategies, bundling options, and pricing levers to manage adoption friction in 2026 procurement cycles.

-

M&A and partnership targets: A curated list of potential acquisition or investment targets aligned with three corporate archetypes — scale players seeking vertical integration, platform players seeking IP uplift, and nimble innovators pursuing niche domination.

-

Regulatory and standards impact analysis: Practical checklists for compliance (including reference to established HVAC and laboratory safety frameworks) and a timeline of potential regulation‑driven procurement opportunities.

Market structure and concentration — what the numbers imply

The market exhibits intermediate concentration: the three‑player and five‑player concentration metrics indicate a meaningful presence of established, capable vendors while leaving room for specialist entrants and regional champions. This structure favors strategic plays that combine focused R&D with targeted partnerships rather than broad‑based, capital‑intensive rollouts. For 2026 planning, organizations should prioritize identifying the particular competitive configuration in their target segments (e.g., cold chain, high‑density electronics, medical devices) and design alliance strategies accordingly.

Competitive landscape: strategy implications for leading players and challengers

-

Ferrotec Holdings Corporation (Japan) — A major global manufacturer of thermoelectric modules and assemblies. Ferrotec’s strength in component scale and cross‑sector sales channels positions it as a preferred supplier for OEMs seeking supply security. Strategy implication: pursue collaboration on module customization and long‑term supply contracts with indexation to raw material inputs.

-

Coherent Corp. (United States) — With capabilities inherited from precision thermal management portfolios, Coherent is well‑placed to serve high‑precision applications. Strategy implication: emphasize co‑development agreements that embed cooling solutions into higher‑value instrumentation, capture system margins, and defend against component commoditization.

-

Laird Thermal Systems (United States) — Specialist in medical and electronics cooling systems. Strategy implication: accelerate compliance and certification roadmaps to convert increasing regulatory and procurement preference into share gains.

-

Phononic, Inc. (United States) — Focused on refrigeration and data‑center scale solutions. Strategy implication: validate system economics against incumbent vapor‑compression benchmarks in pilot deployments and use performance guarantees to overcome procurement inertia.

-

Delta Electronics (Taiwan) — Integrates solid‑state cooling with broader power and thermal management portfolios. Strategy implication: leverage system bundling to present holistic propositions to OEMs and cloud operators where thermal and power management are jointly optimized.

-

Specialists and regional players — Several niche manufacturers and suppliers provide modular and custom solutions for laboratories, instrumentation, and industrial enclosures. Strategy implication: large players should consider bolt‑on acquisitions or preferred supplier agreements to quickly access specialized know‑how without building it in house.

Technology inflection: the CHESS breakthrough and its strategic signal

In 2025, Johns Hopkins Applied Physics Laboratory announced a nano‑engineered thin‑film thermoelectric material (CHESS) demonstrating near‑doubling of device efficiency in laboratory refrigeration tests and later receiving recognition through a major R&D award. For corporate strategists, this development is a classical high‑impact, medium‑to‑long‑term technology risk: if CHESS or comparable materials are commercialized at scale, they could materially alter device performance envelopes, unit economics, and addressable applications.

Recommended 2026 actions:

-

Initiate contingent R&D pathways: Fund small, rapid prototyping efforts to validate second‑generation material performance in your product architectures.

-

Engage with IP holders: Explore licensing, sponsored research, or preferred supplier arrangements to secure early access to next‑gen materials without gambling on in‑house breakthroughs.

-

Stress‑test supply chains: Model scenarios where advanced materials shift BOM composition and analyze implications for sourcing, concentration, and geopolitical exposure.

Dynamics that will shape 2026 procurement and product strategies

-

Standards and safety: Established guidelines for data‑processing environments and laboratory equipment remain relevant touchpoints for product certification. Investors and procurement teams should insist on documented compliance pathways (including IEC‑level safety standards) before scaling purchases.

-

Raw material dependence: Thermoelectric modules continue to rely heavily on bismuth telluride and related semiconductors. Volatility in speciality semiconductor supply can rapidly affect margins and lead times; 2026 sourcing strategies must include hedging, dual‑sourcing, and forward contracts where appropriate.

-

Regulatory tailwinds: Escalating restrictions on HFC refrigerants and environmental procurement criteria create near‑term demand pockets for refrigerant‑free solutions. Capture these opportunities by positioning solid‑state offerings with validated lifecycle and end‑of‑life narratives.

-

Scaling limits: Despite gains, solid‑state cooling faces an efficiency and cost competitiveness gap relative to vapor compression for large HVAC systems. Expect adoption to continue first in precision cooling niches (electronics, cold chain micro‑refrigeration, laboratory equipment) before broader HVAC displacement occurs.

Actionable steps for executives in 2026

-

Portfolio triage: Classify your product and customer segments by adoption readiness — invest in integrations for near‑term, high‑value niches while piloting advanced materials for medium‑term expansion.

-

Supplier and IP playbook: Develop layered contractual relationships — strategic partnerships with module manufacturers, licensing options with research labs, and contingent supply agreements for critical raw materials.

-

Pilot commercialization: Run focused pilots that quantify total cost of ownership against incumbent solutions and build procurement‑grade case studies for 2027 rollouts.

-

M&A screening: Use the report’s neutral scoring framework to identify targets that accelerate time‑to‑market (component scale, thermal systems integration, or proprietary IP) without disproportionate integration risk.

What the full report delivers — and what you’ll find behind the paywall

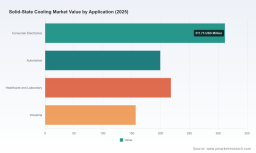

PW Consulting’s full Solid State Cooling Market report packages the quantitative models, granular competitor profiles, supplier maps, and executable playbooks referenced here. To preserve strategic value for subscribers and partners, core subsegment breakdowns and detailed regional/application shares are reserved for the full deliverable. If your 2026 planning relies on precise TAM by application, supplier‑level revenue streams, or a ranked list of M&A targets with financial models, the complete report is the operational tool you will need.

Closing perspective

Solid‑state cooling is moving from the fringes of thermal management into a phase of practical commercial scaling. For companies making 2026 resource allocation choices, the decision is not binary: it is about sequencing — where to invest now, what to pilot, and which partnerships to form to preserve optionality as materials and architectures evolve. PW Consulting’s analysis turns market momentum into executable intelligence: not by promising certainty, but by clarifying scenarios, quantifying sensitivities, and laying out the tactical playbook that companies must use to translate 12.48% CAGR growth and a doubling‑scale market into durable competitive advantage.

To access the full dataset, company dossiers, and strategic playbooks that underpin these insights, refer to the PW Consulting Solid State Cooling Market report page.

For detailed analysis of this topic, please visit the official page: Solid State Cooling Market

Lacy Lee

Senior Marketing Manager

sales@pmarketresearch.com

00852-95632430

PW Consulting: www.pmarketresearch.com

Tags

PW Consulting

The Best-reviewed Subdivided Market Risk Analysis Firm in the US and East Asia.