PW Consulting: Commercial Aircraft In-Seat Power Market to Grow from USD 164.78 Million in 2025 to USD 229.62 Million by 2032, Tracking a 4.85% CAGR

Commercial Aircraft In-Seat Power System Market: Strategic Signals for 2026 Decision-Makers

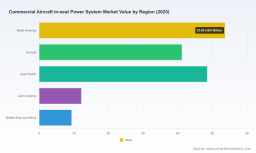

PW Consulting’s latest market study on the Commercial Aircraft In-Seat Power System Market delivers a tactical intelligence package for aviation executives entering 2026. Grounded in historical observation (2020–2025) and forward-looking forecasting (2026–2032), this report translates market dynamics into immediate actions for airlines, OEMs, Tier‑1 suppliers, and investors. The headline: after a pandemic-era trough, the in‑seat power market has recovered to roughly USD 164.8 Million in 2025 and is forecast to reach approximately USD 173.4 Million in 2026, growing at a compound annual growth rate (CAGR) of 4.85% through 2032 (targeting about USD 229.6 Million by 2032). This trajectory reframes in‑seat power from a passenger amenity to an operational baseline and a strategic battleground for cabin systems differentiation.

Why 2026 Is a Strategic Inflection Point

-

Normalization of passenger travel demand combined with an acceleration in BYOD (bring-your-own-device) behavior has elevated seat-level power from a premium feature to a network expectation. Carriers that treat power provisioning as a capacity and service KPI will gain immediate loyalty and ancillary revenue advantages.

-

Regulatory and materials pressures are converging to reshape product architectures: regulators are coalescing around more universal USB‑C standards, and supply‑chain constraints (notably on high‑grade copper) are accelerating higher‑voltage distribution strategies and lighter power electronics. These technical constraints create a narrow window in 2026 for suppliers to set design wins that persist for the next decade.

-

Commercial pressures on aircraft weight and cabin space — driven by fuel‑efficiency mandates — make compact, high‑efficiency power converters and slimline mounting solutions a procurement priority. Early adopters of optimized power architectures in 2026 will realize fuel and maintenance benefits beyond the device charging value proposition.

What the Report Delivers: Practical Tools, Not Just Projections

This study is intentionally operational. Beyond headline sizing and CAGR, the report contains a suite of practitioner-focused deliverables designed to inform procurement cycles, product roadmaps, and M&A evaluation in 2026:

-

Validated market-sizing methodology and a transparent reconciliation of historical data (2020–2025) with our 2026–2032 base-case and two alternate scenarios — upside (accelerated USB‑C adoption and retrofit cycles) and downside (supply‑chain shocks and slower airline capex).

-

Decision-grade supplier scorecards covering product breadth, linefit/retrofit capabilities, certification timelines, service networks, and integration readiness with IFE and cabin electronics — calibrated for procurement teams to shortlist finalists in a 90‑day vendor selection process.

-

Total Cost of Ownership (TCO) models and payback simulations that capture energy consumption, weight penalties, wiring strategy, maintenance roadmap, and ancillary revenue potential from seat-level charging services.

-

Integration playbooks for OEMs and seat vendors that map mechanical, electrical, and software integration checkpoints; certification risk matrices; and testing timelines to shorten time-to-service for new linefit programs.

-

A retrofit vs. linefit adoption curve and fleet prioritization matrix to help airlines allocate capital across fleet classes, route profiles, and customer segments — enabling staged rollouts that maximize short‑term ROI while preserving long‑term compatibility.

-

M&A and partnership blueprints illustrating value-creation levers (software-enabled services, aftermarket support contracts, regional aftermarket penetration), with sensitivity analyses tied to supply‑chain elasticity and regulation-driven technical requirements.

Competitive Landscape: Who Matters and Why

The market is moderately concentrated: the top three suppliers capture roughly half of current market value, while the leading five control approximately two‑thirds. That structure produces a dual landscape of established integrators and specialized innovators — a dynamic that favors strategic partnerships and selective vertical integration.

-

Astronics Corporation (East Aurora, NY) continues to set product benchmarks with its EmPower product line — most recently introducing the EmPower 1327‑27 Dual USB‑Type‑C outlet in April 2026. Astronics’ focus on high‑power USB‑C and proven linefit and retrofit installs positions it as the default choice for carriers seeking low‑risk rollouts and rapid certification pathways.

-

Collins Aerospace (Charlotte, NC) remains a systems integrator with strength in cabin electrics and data ports, offering integrated solutions where power is bundled with IFE and seating systems — a compelling value proposition for OEMs seeking single‑vendor integration and simplified aircraft contracts.

-

IFPL Group (Isle of Wight) and specialist OEMs such as Burrana (Cannon Hill, QLD) and KID‑Systeme (Buxtehude, Germany) are driving innovation at the module and UX level. Burrana’s RISE platform positioning and IFPL’s 30th anniversary showcase at AIX underline the focus on modular cabin ecosystems and long-term service footprints.

-

Panasonic Avionics (Lake Forest, CA) has demonstrated system-level differentiation by coupling high‑power USB‑C delivery with its Astrova IFE — a deployment that entered service with Air Canada in April 2026 and signals the commercial viability of integrated IFE‑power offerings for premium cabins and transcontinental widebody operations.

-

Component specialists such as Mid‑Continent Instrument Co. (True Blue Power) and Astrodyne TDI supply critical electrical subsystems — from TSO‑certified chargers to custom power modules — and therefore act as attractive acquisition targets for integrators seeking tighter control of supply chains and performance tuning.

Recent Developments and Strategic Implications

-

Astronics’ product launch of a dual USB‑C outlet (April 2026) accelerates the industry’s shift to high‑power, universal charging and raises the bar for retrofit packages — signifying that cargo‑weight tradeoffs must now include device power economics.

-

Burrana’s visible positioning at AIX 2026 and IFPL’s showcase activity underline trade show channels as primary deal‑making venues for 2026 — procurement calendars should align RFP cycles with major industry events to capture first‑mover integration advantages.

-

Panasonic’s Astrova deployment with high‑power USB‑C demonstrates the commercial momentum for tightly coupled IFE‑power propositions in airline product differentiation — a signal for carriers to revisit content‑plus‑power bundling strategies.

-

Regulatory momentum toward USB‑C standardization and aircraft efficiency mandates (including pressure to reduce cavity and weight by approximately a quarter for certain power components) make 2026 a critical year to adopt designs that will remain compliant and efficient for the next retrofit horizon.

Risks, Supply Constraints, and Mitigations

Our scenario analysis surfaces three primary risk vectors for 2026 decision-makers:

-

Supply-chain tightness for high‑grade copper and specialty semiconductors, which can delay certification and inflate retrofit costs. Mitigation: lock multi‑year supply agreements with alternative material strategies (higher‑voltage architectures) and dual‑sourcing clauses.

-

Standardization uncertainty around USB‑C power‑delivery profiles and airline policies for power management. Mitigation: deploy configurable power modules with field‑upgradeable firmware and negotiate standards‑aligned warranties.

-

Competitive displacement from bundled IFE‑and‑power offers. Mitigation: pursue commercial partnerships to bundle power with content and ancillary monetization platforms or focus on aftermarket service contracts that lock in long‑tail revenues.

Actionable 90‑Day Plan for 2026

-

Carriers: Audit fleet retrofit potential using our fleet prioritization matrix; pilot high‑power USB‑C on targeted narrowbody transcon and long‑haul aircraft to measure customer behavior and ancillary monetization.

-

OEMs and Seat Vendors: Finalize modular power integration standards and lock seat‑level mechanical interfaces to accelerate linefit time to service. Use the report’s integration checklist to reduce certification surprises.

-

Suppliers: Reassess BOMs for copper intensity and reprice offerings with higher‑voltage variants; prepare product line options that trade a small increase in initial unit cost for long‑term weight and maintenance savings.

-

Investors: Use the supplier scorecards and TCO scenarios to identify high‑margin retrofit specialists or vertically integrative candidates for selective M&A — targets that can deliver aftermarket service revenue and have clear paths to recurring software updates.

Why PW Consulting’s Study Is Decision-Critical

For 2026 planning cycles, the report offers more than market numbers: it synthesizes regulatory trends, supplier positioning, and engineering constraints into transaction‑ready guidance. Whether your objective is to accelerate retrofit rollouts, secure linefit design wins, hedge supply risk, or evaluate acquisition targets, the analyses — from TCO models to supplier scorecards and scenario stress tests — turn uncertainty into executable timelines and KPIs.

We intentionally present high‑confidence insights while withholding detailed segmentation tables and full numerical breakdowns in this summary. To access the complete datasets, regional and class-level splits, supplier scorecards, and downloadable financial models that underpin our recommendations, visit the PW Consulting report page or contact our advisory desk to arrange a briefing. For teams with immediate 2026 procurement windows, our analysts are available for short‑term workshops that convert the report’s findings into RFQ specifications and certification roadmaps.

For detailed analysis of this topic, please visit the official page: Commercial Aircraft In Seat Power System Market

Lacy Lee

Senior Marketing Manager

sales@pmarketresearch.com

00852-95632430

PW Consulting: www.pmarketresearch.com

Tags

PW Consulting

The Best-reviewed Subdivided Market Risk Analysis Firm in the US and East Asia.