PW Consulting Forecast: Wireless WAN Solutions Market to Expand at a Robust 14.48% CAGR During 2026–2032

Wireless WAN Solutions Market 2026: Strategic Signals for Enterprise Leaders

As organizations prepare capital and technology roadmaps for 2026, Wireless WAN strategies are moving from tactical connectivity projects to mission-critical infrastructure programs. PW Consulting’s latest market study, Wireless WAN Solutions Market (base year 2025), synthesizes multi-year market dynamics, vendor behaviors, regulatory inflection points, and deployment economics into a practical playbook for enterprise decision-makers. The headline: the market is entering a sustained, high-growth phase—driven by broad 5G maturation, SD-WAN convergence, and new edge-oriented use cases—creating both opportunity and complexity for CIOs, infrastructure leaders, and procurement teams.

Wireless Wan Solutions Market

Market trajectory: what the macro numbers tell you (and what they don't)

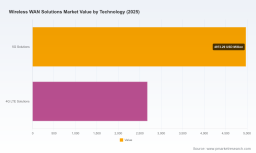

Our analysis shows a marked acceleration in the Wireless WAN market over the past half decade, with global revenues growing materially between 2020 and 2025, and an expected compound annual growth rate (CAGR) of 14.48% through our forecast window. On a topline basis, the market expands from a mid‑single‑digit billion‑dollar industry in 2025 to a near‑twenty billion dollar scale by the end of the forecast horizon. These macro figures confirm two strategic realities for 2026 planning: (1) wireless WAN is no longer a niche failover capability but an architectural pillar for distributed enterprises; and (2) timing and vendor choices will materially affect total cost of ownership (TCO) and service differentiation over the next three years.

Wireless Wan Solutions Market

We intentionally refrain from disclosing granular regional or application-level allocations in this release; the full report contains the segment-level intelligence that procurement teams will find indispensable when selecting partners or sizing pilots for specific geographies and verticals.

Wireless Wan Solutions Market

Why 2026 is a decisive year for enterprise wireless WAN strategies

- 5G transitions from experimental to operational: Network operators and equipment vendors are accelerating standalone 5G deployments, expanding low-latency and reliability capabilities that matter for real-time edge applications (private wireless, industrial IoT, and mission-critical comms).

- SD-WAN and cellular convergence: Mature SD-WAN offerings now embed multi‑cellular uplink, active/active bonding, and edge orchestration—shifting purchasing decisions from separate network and cellular silos to integrated solutions and managed service models.

- Regulatory and spectrum dynamics: Policy outcomes—such as C-band allocations and digital markets rules—are reshaping go-to-market options for operators and vendors. Enterprises must incorporate regulatory risk and spectrum availability into site-level design and vendor engagements.

- Capital and operational trade-offs: The economics of 5G small cell deployment, varied backhaul options, and evolving device cost curves mean transport decisions must be evaluated at the application and lifecycle level rather than by simple per‑site capex comparison.

Report deliverables: practical tools for 2026 decision-making

PW Consulting’s study was designed as an enterprise-ready toolkit—not just a market read. The full report includes:

- Validated market sizing and growth scenarios (base, upside, downside) to stress-test your investment cases;

- Vendor scorecards that assess product fit across enterprise requirements (security posture, manageability, latency SLAs, and hybrid orchestration);

- Deployment playbooks for common enterprise topologies (retail edge, branch consolidation, industrial campuses, and temporary/POP‑up sites) with recommended technology and procurement pathways;

- TCO and risk models factoring capital, recurring access costs, multi‑carrier strategies, and regulatory compliance overheads;

- Procurement checklists and RFP templates tailored to evaluate integrated hardware/software/service offers; and

- Scenario planning modules that quantify the operational impact of spectrum policy shifts, equipment export controls, and standards evolution.

These outputs are purpose-built for CIOs and network architects who must translate high-level growth trends into defensible budgets and vendor selections in 2026.

Competitive landscape: who matters, and why

The market shows a moderate concentration with a few major network and infrastructure suppliers commanding a substantial share—creating a competitive environment where both incumbent strength and focused specialist offerings matter. Our competitive assessment examines operator-led offerings, systems vendors, and specialized edge-router suppliers. Key players include solutions and strategy makers such as Cisco Systems, Ericsson, Huawei Technologies, Nokia, Verizon, T‑Mobile (post-merger operator scale), VMware (Broadcom), and niche hardware specialists like Pepwave. Each brings a distinct value proposition:

- Cisco Systems: Leveraging integrated Meraki and Catalyst portfolios, Cisco is positioning ruggedized cellular edge routers and SD‑WAN orchestration as an enterprise control point—appealing to organizations prioritizing centralized management and security policy consistency.

- Ericsson and Nokia: Focused on carrier-grade 5G RAN and core solutions, these vendors are expanding capabilities that enable operators to offer higher-capacity, low-latency wireless WAN services—especially where private/neutral-host deployments are required.

- Huawei Technologies: Remains influential in many markets with comprehensive radio and edge routing products; enterprises should assess geopolitical and export considerations as part of procurement due diligence.

- Verizon and T‑Mobile: Operators are commercializing differentiated 5G tiers—including dedicated and private 5G options—that can be bundled into managed WAN propositions for distributed enterprises.

- VMware (Broadcom): Positioned as an SD‑WAN and virtualization layer integrator, VMware’s solutions are central to hybrid WAN strategies that blend wired and cellular transports.

- Pepwave: Specialist multi‑WAN routers and cellular bonding solutions remain important for customers focused on high-availability branch connectivity with simplified deployment footprints.

Our vendor analysis includes strengths/weaknesses mapping, strategic fit for verticals, and recommended negotiation levers—material inputs for enterprise shortlists ahead of 2026 procurement cycles.

Recent industry movements that will influence next‑year choices

- Ericsson’s 5G Advanced offerings (Oct 2025) expand support for reduced-capability IoT devices—this broadens addressable wireless WAN use cases where ultra‑low cost, low‑complexity endpoints are required.

- Nokia’s wide deployment of standalone 5G cores (Sept 2025) improves operator capacity and creates a better foundation for managed private 5G services.

- Cisco’s release of ruggedized routers with sub‑6GHz 5G support (June 2025) tightens the integration between industrial OT use cases and enterprise WAN policies.

- Verizon’s mmWave expansion (March 2025) and earlier T‑Mobile standalone URLLC activations (Dec 2024) demonstrate operator moves to differentiate through coverage and latency capabilities—factors that enterprise architects should explicitly model in SLA negotiations.

These developments, combined with regulatory signals such as mid-band spectrum auctions and network neutrality provisions in major jurisdictions, mean 2026 procurement must account for a rapidly shifting service and compliance landscape.

Regulatory and infrastructure considerations that change the playbook

- Mid‑band spectrum allocations and auction outcomes directly influence carrier capacity planning and private network feasibility—enterprises procuring national footprints should include spectrum availability scenarios in vendor selection.

- Export control regimes and cryptographic origin rules affect supplier eligibility for certain deployments; our report provides a practical compliance checklist for global rollouts.

- Small‑cell deployment economics (site installation, power, and backhaul) remain a non-trivial component of edge-enabled use cases; we provide benchmark cost drivers and alternative designs to reduce capital intensity.

- Standards evolution (notably recent 3GPP releases enhancing public safety and mission-critical services) creates new functional requirements—our recommendation is to require forward‑compatibility and upgrade paths in procurement contracts.

Actionable recommendations for 2026 planning cycles

- Adopt a three‑track investment posture: foundational (connectivity resilience), selective (high‑value edge pilots), and optionality (managed private wireless trials). This balances near‑term reliability with long‑term strategic options.

- Require vendor roadmaps and interoperability commitments in all RFPs to safeguard planned upgrades and cross‑vendor orchestration.

- Use multi‑carrier strategies at critical sites to de‑risk coverage and regulatory exposure, while negotiating pooled pricing and unified SLAs to control complexity.

- Embed compliance and export-control reviews early in the procurement process to avoid late-stage vendor disqualification and schedule slippage.

- Model lifecycle TCO that incorporates small cell capital, operational site costs, and software/subscription escalators—our report supplies a templated model to accelerate this analysis.

Where this release fits in your decision framework

This article is a strategic brief. The complete Wireless WAN Solutions Market report from PW Consulting provides the segmental depth, vendor scorecards, and downloadable tools required to finalize budgets and vendor selections in 2026. We deliberately withhold granular split data from this summary to ensure enterprise teams engage with the full suite of analysis and templates that underpin prudent purchasing decisions.

To executive sponsors and procurement leads: treat 2026 as the year to convert organizational experiments with wireless WAN into repeatable, documented programs. Use the market growth trajectory, vendor behavior signals, and regulatory context highlighted here to prioritize pilots that deliver measurable business outcomes—revenue enablement, resilience, or cost reduction—and insist on contract provisions that protect you as the market and standards evolve.

Next steps

- Request the full PW Consulting Wireless WAN Solutions Market report to access regional and application segmentation, vendor scorecards, and scenario models.

- Engage our advisory team for a tailored briefing and hands‑on support to convert the findings into a 2026 rollout plan and RFP.

PW Consulting remains committed to translating nuanced market signals into clear, executable strategies. The wireless WAN transition is underway—enterprises that combine rigorous market intelligence with disciplined procurement execution will secure the connectivity advantage in 2026 and beyond.

For detailed analysis of this topic, please visit the official page: Wireless Wan Solutions Market

Lacy Lee

Senior Marketing Manager

sales@pmarketresearch.com

00852-95632430

PW Consulting: www.pmarketresearch.com

Tags

PW Consulting

The Best-reviewed Subdivided Market Risk Analysis Firm in the US and East Asia.