PW Consulting: 4‑Pin XLR Connector Market to Expand from USD 51.2 Million in 2025 to USD 79.3 Million by 2032 at a 6.45% CAGR

4-Pin XLR Connector Market — Strategic Primer for 2026 Decision Makers

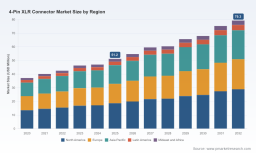

PW Consulting’s latest market study on the 4-pin XLR connector market (Base Year 2025; Historical Period 2020–2025; Forecast Period 2026–2032) reframes the way procurement, product, and corporate strategy teams should interpret connector market signals entering 2026. Compiled in USD (Revenue unit: Million), the addressable market has expanded from a modest industry base in 2020 to USD 51.2 Million in 2025 and, under our central-case outlook, is projected to reach approximately USD 79.3 Million by 2032 — an anticipated compound annual growth rate (CAGR) of 6.45% over the forecast window. This briefing synthesizes the report’s most actionable implications for enterprise-level strategy while preserving the detailed segment-level analytics that are available in the full study.

4 Pin Xlr Connector Market

Why 2026 is a Pivotal Year for Connector Strategy

-

Input cost shock and supply constraints: By early 2026 the commodity environment has materially altered the cost profile for metal-bodied and plated-contact connectors. Copper traded near USD 13,300 per ton on the London Metal Exchange, gold surpassed USD 5,000 per ounce and silver exceeded USD 100 per ounce — each movement directly lifting bill-of-materials (BOM) costs for premium 4‑pin XLR products. Parallel forecasts suggest a copper market deficit in 2026, amplifying short-term availability risks for copper-alloy components.

4 Pin Xlr Connector Market -

Policy and trade friction: New export licensing controls on silver introduced by China at the start of 2026 create potential sourcing friction for silver-plated contacts — a common specification for premium audio and lighting connectors. Combined with supplier price adjustments announced by major connector suppliers in early 2026, the net effect is a structurally higher cost baseline and greater procurement complexity.

4 Pin Xlr Connector Market -

Market structure: Competitive concentration in the 4‑pin XLR market is meaningful but not prohibitive — the three largest players control a material share, and the top five command a clear majority of traded value. This configuration creates differentiated supplier power tiers and influences negotiation levers for OEMs and system integrators.

Strategic Implications for 2026 Decision Makers

-

Rethink procurement paradigms — short-term spot purchasing of metal-intensive connector variants is now a direct margin risk. Organizations should evaluate blended sourcing (fixed-price contracts for standard parts; market-linked contracts for scarce alloys) and build commodity pass-through clauses where appropriate to allocate price risk transparently.

-

Design for materials optionality — product teams should prioritize modular contact designs that enable alternative plating chemistries or reduced precious‑metal content without compromising signal integrity. Where performance allows, tin and nickel alternatives can materially reduce exposure to silver and gold volatility.

-

Supplier segmentation and resilience — differentiate strategies for premium versus value channels. For branded, high-reliability product lines, prioritize established suppliers with validated quality systems and service-level commitments. For cost-sensitive SKUs, leverage qualified OEMs with scalable manufacturing and flexible lead times.

-

Operational hedging and inventory optimization — given the projected upcycle in raw-material costs and potential supply bottlenecks, increasing strategic safety stock for critical contact materials and finished assemblies can be a rational short-term hedge. However, do so with disciplined inventory economics informed by the report’s scenario modeling.

-

Commercial and price-pack architecture — reconsider how connector price increases are communicated and contracted. The market now favors transparent, index-linked pricing mechanisms and tiered rebates tied to volume commitments rather than sudden, across-the-board hikes.

-

M&A and partnership windows — margin pressure and supplier fragmentation create opportunistic windows to acquire niche manufacturers, vertically integrate plating capacity, or secure long-term supply through equity partnerships. Our scenario work identifies target archetypes and timing for proactive acquisitions.

What PW Consulting’s Full Report Delivers (Practical & Operational)

-

Robust market-sizing and scenarios: A transparent methodology that reconciles shipment data, contract wins, and component BOM analysis to produce base, upside, and downside scenarios for 2026–2032, with sensitivity to metal prices and regulatory disruptions.

-

Price-impact simulations: Line-itemed margin models that quantify how commodity swings (copper/silver/gold) cascade through to FOB and distributor pricing across common connector families.

-

Supplier benchmarking playbook: Operational scorecards for tiered suppliers that include quality KPIs, lead-time variability, capacity elasticity, and financial resilience metrics — designed for procurement to accelerate RFx and dual-sourcing decisions.

-

Go-to-market and portfolio tactics: Actionable recommendations to optimize SKU rationalization, aftermarket spares strategies, and channel incentives that protect ASP while preserving system reliability for professional audio, lighting, and intercom use cases.

-

Risk and compliance heatmaps: Visualized exposure for metal procurement, export controls, and single-source dependencies to prioritize mitigation investments.

Note: Detailed regional, type and application split tables and granular revenue-by-segment figures are intentionally reserved for subscribers of the full PW Consulting report.

Competitive Landscape — Practical Read for Strategy Teams

The competitive set combines long-established branded incumbents, diversified connector platforms from large electro-mechanical groups, and cost-competitive OEMs. Key market actors assessed in the report include:

-

Neutrik AG (Schaan, Liechtenstein) — A global leader renowned for the professional audio market; offers a full range of 4‑pin cable and chassis connectors with premium plating and mechanical options. Neutrik’s brand equity, broad acceptance across AV and pro‑audio channels, and recent 50th-anniversary portfolio reaffirmation underscore its role as a technology and standards anchor in the market.

-

Switchcraft (United States) — A premium US manufacturer focused on durable, serviceable connectors for harsh environments. Its product positioning — performance, finish options and solder-cup terminations — makes it a preferred supplier for specification-driven OEMs.

-

Amphenol Audio (United States) — Part of a diversified connector group with high production scale and industrial-grade product options. Amphenol’s line-up is competitive where price-performance and supply continuity are decisive.

-

Ningbo Seetronic (Ningbo, China) — A cost-competitive manufacturer with waterproof and value lines that serve the lighting and budget audio segments. Its expanding product variants and price agility make Seetronic a common choice for large-volume programs where cost is a primary selection criterion.

-

IO Audio Technologies (United States) — A niche specialist offering focused 4‑pin solutions targeted at audio and low-voltage power applications; appeals to buyers requiring US-based support and custom engineering.

-

Guangzhou Diwei Electronics (Guangzhou, China) — An OEM capable of custom and standard production runs, often engaged as a private-label partner for system integrators and distributors.

Strategically, the market presents three supplier tiers — global branded specialists, large diversified connector groups, and regionally competitive OEMs. The top‑three and top‑five concentration metrics indicate industry leader influence, but not an immovable oligopoly; nimble OEMs can still capture share on cost and responsiveness. The recent Neutrik Group anniversary highlights brand endurance, while ongoing raw-material-driven price actions by major industry players illustrate how upstream dynamics are rapidly reshaping competitive margins.

Actionable Next Steps for Executives (90–180 Day Roadmap)

-

Initiate a BOM risk audit focused on contact plating and housing alloys; quantify financial exposure across product families using the report’s price-impact templates.

-

Negotiate a two-track sourcing strategy: secure fixed-volume contracts for mission-critical SKUs while retaining a market-linked tranche to exploit short-term price dips.

-

Prioritize design-for-substitution pilots for non-critical SKUs to validate performance with alternative platings and lower-precious-metal contacts.

-

Engage in supplier scorecard rollouts and add manufacturing site audits for critical partners to de-risk single-source dependencies.

Conclusion and How to Access the Full Intelligence

For organizations that depend on reliability, specification integrity, and predictable cost structures — from pro-audio OEMs and broadcast houses to lighting rigs and intercom systems — 2026 is a year to transition from tactical firefighting to strategic redesign. PW Consulting’s 4‑Pin XLR Connector Market report equips leaders with the models, supplier benchmarks, and commercial playbooks necessary to convert commodity volatility into structured, defensible advantage.

To review the full dataset, segment-level forecasts, supplier heatmaps, and downloadable commercial templates, access the complete PW Consulting report. The public primer above is designed to make the strategic imperative clear; the full report contains the granular inputs and executable artifacts your team will need to operationalize a winning response in 2026.

For detailed analysis of this topic, please visit the official page: 4 Pin Xlr Connector Market

Lacy Lee

Senior Marketing Manager

sales@pmarketresearch.com

00852-95632430

PW Consulting: www.pmarketresearch.com

Tags

PW Consulting

The Best-reviewed Subdivided Market Risk Analysis Firm in the US and East Asia.