PW Consulting Forecasts Refined Wood Vinegar Market to Reach USD 11.35 Million by 2032

Refined Wood Vinegar Market — Strategic Outlook for 2026: Signals, Risks and Actionable Plays for Corporate Leaders

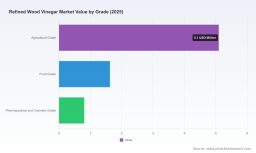

PW Consulting’s new Refined Wood Vinegar Market analysis (base year 2025; historical 2020–2025; forecast 2026–2032) synthesizes commercial, technical and regulatory signals that will matter for strategic decisions in 2026. At the macro level the market shows steady expansion — rising from USD 5.6 Million in 2020 to USD 7.54 Million in 2025, with a projected compound annual growth rate of 6.02% through the 2026–2032 horizon and a forecast market value approaching USD 11.35 Million by 2032. The competitive structure is neither highly fragmented nor tightly consolidated: top-three firms account for roughly 42% of market throughput, and the top-five for about 58% — a profile that enables opportunistic M&A and rapid share shifts for well-capitalized entrants.

Refined Wood Vinegar Market

What this briefing (and the full report) delivers

- Proven market-sizing methodology and scenario-based forecasts calibrated to 2025 primary data and 2026 policy/regulatory inflections.

- Actionable go-to-market playbooks for suppliers, industrial buyers and agri-input distributors — including channel sequencing, pricing frameworks and contract constructs for refined versus crude grades.

- Supply-chain and feedstock intelligence: risk maps for biomass availability, refinement bottlenecks, and capital estimates for scaling purification lines.

- Regulatory and certification roadmap: OMRI, ISO/COA/SGS practices, and implications of high-integrity carbon project standards on co-product commercialization.

- Competitive benchmark dossiers, capability matrices and acquisition candidates ranked by strategic fit and operational readiness.

- Commercial pilots, ROI models and a prioritized 18‑month implementation plan for producers and buyers seeking early advantage.

Why the 2026 decision window is pivotal

Three converging forces make 2026 a strategic inflection point:

Refined Wood Vinegar Market

- Supply-side integration of biochar and pyrolysis projects. Large-scale carbon removal initiatives increasingly couple biochar production with wood vinegar co‑generation. When these projects adopt rigorous MRV frameworks aligned with market-leading registries, they unlock a dual-value chain: long‑duration carbon credits and an agricultural/industrial input stream. Players that secure offtake or equity in such projects can internalize feedstock risk and capture value across both outputs.

- Premiumisation driven by refinement and certification. Refined wood vinegar — where tar, methanol and other undesirable compounds are removed and acetic acid content is controlled — commands quality-sensitive channels (specialty agriculture, feed additives, cosmetics). Certification pathways (OMRI for organic ag inputs; ISO/SGS/COA for industrial buyers) materially widen addressable markets but require capital and process controls.

- Market concentration conducive to consolidation and strategic partnerships. The current CR3/CR5 profile suggests substantial share is already captured by a handful of capable producers, but not so consolidated as to preclude rapid displacement through vertical integration, pricing differentiation or superior supply assurance.

Key strategic takeaways for corporate leaders

- Prioritize feedstock security via upstream partnerships. Short‑term supply contracts with pyrolysis/biochar projects and mid‑term equity or offtake stakes materially reduce volatility in availability and quality of raw wood vinegar.

- Differentiate on refinement and compliance, not just volume. Investment in tar-removal, controlled acetic‑acid formulation, and analytics for residual contaminants will unlock premium channels (organic agriculture, specialty feed, cosmetics) and justify higher margin structures.

- Design product families for channel-specific requirements. A two‑tier product strategy (industrial/crude for commoditized uses; refined, certified SKUs for premium uses) simplifies commercial execution while protecting price integrity.

- Embed carbon-economy narratives into commercial propositions. Where feedstock originates from verified carbon-removal projects, market-facing claims and co-marketing create ESG premium opportunities — but only if MRV and registry requirements are demonstrably met.

- Prepare an M&A and alliance playbook. Given the moderate concentration, targeted acquisitions of distillation/refinement capabilities or regional distributors can accelerate scale and access to end markets.

- Operational risk management: develop quality-assurance labs and standardized Certificates of Analysis to reduce buyer friction and speed adoption among agronomists, feed formulators and cosmetic formulators.

Competitive landscape — practical implications

The market features a blend of specialty distillers, factory-direct industrial suppliers, pyrolysis-integrated producers and regionally focused players. Our report includes company profiles and strategic assessments; below we summarize strategic postures that matter to buyers and investors.

Refined Wood Vinegar Market

- Specialized, high-refinement suppliers (example profile: U.S. and Japan-based producers that emphasize distilled, filtered, and pH‑controlled product lines) are best positioned to win specialized agricultural and cosmetic contracts where performance and absence of undesirable residues are contractual prerequisites. For buyers seeking OMRI-listed inputs or cosmetic‑grade certifications, partnering with or acquiring such suppliers accelerates market entry.

- Factory-direct, high-volume manufacturers (example profile: large Chinese producers with ISO/SGS certifications) are competitive on price and logistics for commodity and industrial applications — they are logical partners for formulators and large feed producers who prioritize cost and supply scale over premium certification.

- Pyrolysis-integrated actors and biochar operators (several regional players and new partnerships announced in 2024–2026) create the most attractive value capture when carbon credits and co‑product commercialization are jointly managed. Recent partnerships that deploy agricultural waste pyrolysis for biochar and collect wood vinegar as a byproduct illustrate a route to circularity and margin stacking.

- Regional specialty players with OMRI-listed SKUs demonstrate a pragmatic route to premium agri-markets: proof points from labeled products and third‑party certifications reduce adoption friction among organic farmers and distributors.

Recent developments that reshape the playbook

- Partnerships between carbon project developers and industrial implementers are creating project stacks where wood vinegar is a planned co-product; these arrangements increase predictability of supply and broaden sustainability narratives for downstream buyers.

- Product rebranding and formulation standardization by select suppliers have clarified quality differentials — the market is increasingly distinguishing between "crude byproduct" and "refined, application‑specific" wood vinegar. This has direct implications for pricing and channel selection.

- Regulatory alignment with organic standards and MRV practices means compliance is now a strategic asset, not just a box to tick: OMRI listings, authenticated COAs and registry‑grade MRV capabilities materially affect buyer trust and escalation velocity into larger distribution networks.

Recommended 90‑ to 360‑day action plan for 2026

- 90 days: Run a rapid due diligence on two upstream pyrolysis partnerships to secure interim offtake; institute standardized lab testing and COA requirements for all incoming inventory.

- 180 days: Launch a certified refined SKU pilot targeted at one premium channel (organic vegetable seed treatments, specialty feed formulation, or cosmetic ingredient) and measure adoption, margin and technical feedback.

- 360 days: Decide on build vs. buy for refinement capacity based on pilot economics; finalize at least one strategic equity or long-term offtake agreement with a biochar/pyrolysis operator and prepare an M&A shortlist of 3–5 regional producers/distributors.

How PW Consulting supports strategic execution

PW Consulting offers a suite of support services built around our market work:

- Rapid market-entry blueprints tailored to your target channel (agriculture, animal feed, food flavoring, cosmetics/medical), including price ladders and contract templates.

- Technical due diligence on refinement technologies, QA protocols and certification pathways; vendor selection for tar‑removal and acid‑control modules.

- M&A support: target screening, valuation frameworks, and integration roadmaps focused on locking feedstock, refinement capability and distribution reach.

- Carbon-project commercial strategies to align MRV-compliant biochar initiatives with wood vinegar commercialization, maximizing total return on invested capital.

Note: This release is a strategic preview. To maintain competitive value for subscribers and clients, detailed regional and application split tables, granular company market shares, pricing curves by grade, and other core segment-level figures have been intentionally omitted from this summary. The full PW Consulting Refined Wood Vinegar Market Report contains these datasets, primary-source interview excerpts, and executable templates referenced above.

For access to the full report, bespoke briefings, or to schedule a strategy workshop with PW Consulting’s bioeconomy practice, contact our advisory desk. Our team will help you convert the 2026 inflection into a durable advantage.

For detailed analysis of this topic, please visit the official page: Refined Wood Vinegar Market

Lacy Lee

Senior Marketing Manager

sales@pmarketresearch.com

00852-95632430

PW Consulting: www.pmarketresearch.com

Tags

PW Consulting

The Best-reviewed Subdivided Market Risk Analysis Firm in the US and East Asia.