The smart road is the type of advanced technology which guides the drivers of vehicles against any object which is in front of the vehicle. These roads help to reduce the vehicle emissions by identifying best and shortest route for any vehicle to reach its destination.An anemometer is a wind measurement tool which measures intensity, wind direction, amplitude and speed. Physicists use it to study the path of airflow. They come in both digital and manual versions. Anemometers are available in a variety of sizes and shapes. Some are moveable handheld anemometers, while others are fixed.

This report provides a deep insight into the global Smart Roads Anemometers market covering all its essential aspects. This ranges from a macro overview of the market to micro details of the market size, competitive landscape, development trend, niche market, key market drivers and challenges, SWOT analysis, value chain analysis, etc.

The analysis helps the reader to shape the competition within the industries and strategies for the competitive environment to enhance the potential profit. Furthermore, it provides a simple framework for evaluating and accessing the position of the business organization. The report structure also focuses on the competitive landscape of the Global Smart Roads Anemometers Market, this report introduces in detail the market share, market performance, product situation, operation situation, etc. of the main players, which helps the readers in the industry to identify the main competitors and deeply understand the competition pattern of the market.

In a word, this report is a must-read for industry players, investors, researchers, consultants, business strategists, and all those who have any kind of stake or are planning to foray into the Smart Roads Anemometers market in any manner.

Smart Roads Anemometers Market Analysis:

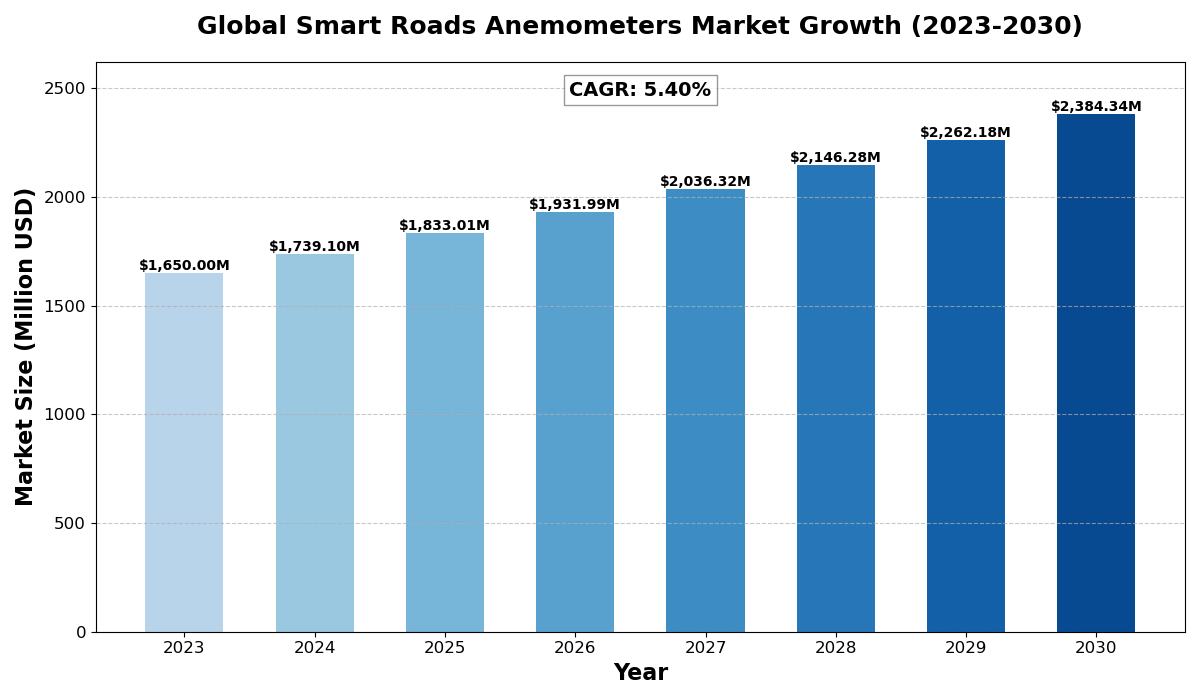

The global Smart Roads Anemometers Market size was estimated at USD 1650 million in 2023 and is projected to reach USD 2384.34 million by 2030, exhibiting a CAGR of 5.40% during the forecast period.

North America Smart Roads Anemometers market size was USD 429.94 million in 2023, at a CAGR of 4.63% during the forecast period of 2025 through 2030.

https://semiconductorinsight.com/wp-content/uploads/2025/03/global-smart-roads-anemometers-market-67d15849239d9-1-300x175.webp 300w, https://semiconductorinsight.com/wp-content/uploads/2025/03/global-smart-roads-anemometers-market-67d15849239d9-1-1024x597.webp 1024w, https://semiconductorinsight.com/wp-content/uploads/2025/03/global-smart-roads-anemometers-market-67d15849239d9-1-768x448.webp 768w, https://semiconductorinsight.com/wp-content/uploads/2025/03/global-smart-roads-anemometers-market-67d15849239d9-1-103x60.webp 103w, https://semiconductorinsight.com/wp-content/uploads/2025/03/global-smart-roads-anemometers-market-67d15849239d9-1-154x90.webp 154w" alt="" width="1200" height="700" data-lazyloaded="1" data-src="https://semiconductorinsight.com/wp-content/uploads/2025/03/global-smart-roads-anemometers-market-67d15849239d9-1.webp" data-warning="Missing alt text" data-srcset="https://semiconductorinsight.com/wp-content/uploads/2025/03/global-smart-roads-anemometers-market-67d15849239d9-1.webp 1200w, https://semiconductorinsight.com/wp-content/uploads/2025/03/global-smart-roads-anemometers-market-67d15849239d9-1-300x175.webp 300w, https://semiconductorinsight.com/wp-content/uploads/2025/03/global-smart-roads-anemometers-market-67d15849239d9-1-1024x597.webp 1024w, https://semiconductorinsight.com/wp-content/uploads/2025/03/global-smart-roads-anemometers-market-67d15849239d9-1-768x448.webp 768w, https://semiconductorinsight.com/wp-content/uploads/2025/03/global-smart-roads-anemometers-market-67d15849239d9-1-103x60.webp 103w, https://semiconductorinsight.com/wp-content/uploads/2025/03/global-smart-roads-anemometers-market-67d15849239d9-1-154x90.webp 154w" data-sizes="(max-width: 1200px) 100vw, 1200px" data-ll-status="loaded">

https://semiconductorinsight.com/wp-content/uploads/2025/03/global-smart-roads-anemometers-market-67d15849239d9-1-300x175.webp 300w, https://semiconductorinsight.com/wp-content/uploads/2025/03/global-smart-roads-anemometers-market-67d15849239d9-1-1024x597.webp 1024w, https://semiconductorinsight.com/wp-content/uploads/2025/03/global-smart-roads-anemometers-market-67d15849239d9-1-768x448.webp 768w, https://semiconductorinsight.com/wp-content/uploads/2025/03/global-smart-roads-anemometers-market-67d15849239d9-1-103x60.webp 103w, https://semiconductorinsight.com/wp-content/uploads/2025/03/global-smart-roads-anemometers-market-67d15849239d9-1-154x90.webp 154w" alt="" width="1200" height="700" data-lazyloaded="1" data-src="https://semiconductorinsight.com/wp-content/uploads/2025/03/global-smart-roads-anemometers-market-67d15849239d9-1.webp" data-warning="Missing alt text" data-srcset="https://semiconductorinsight.com/wp-content/uploads/2025/03/global-smart-roads-anemometers-market-67d15849239d9-1.webp 1200w, https://semiconductorinsight.com/wp-content/uploads/2025/03/global-smart-roads-anemometers-market-67d15849239d9-1-300x175.webp 300w, https://semiconductorinsight.com/wp-content/uploads/2025/03/global-smart-roads-anemometers-market-67d15849239d9-1-1024x597.webp 1024w, https://semiconductorinsight.com/wp-content/uploads/2025/03/global-smart-roads-anemometers-market-67d15849239d9-1-768x448.webp 768w, https://semiconductorinsight.com/wp-content/uploads/2025/03/global-smart-roads-anemometers-market-67d15849239d9-1-103x60.webp 103w, https://semiconductorinsight.com/wp-content/uploads/2025/03/global-smart-roads-anemometers-market-67d15849239d9-1-154x90.webp 154w" data-sizes="(max-width: 1200px) 100vw, 1200px" data-ll-status="loaded"> Smart Roads Anemometers Key Market Trends :

- Growing Adoption of Smart Road Technologies

The integration of AI, IoT, and cloud computing in smart road infrastructure is increasing to enhance road safety and efficiency. - Rising Demand for Traffic Management Solutions

Governments and private firms are investing in smart traffic systems that use anemometers to optimize vehicle movement and reduce congestion. - Expansion of Smart City Projects

The global push towards smart cities is boosting the adoption of intelligent road systems, including advanced anemometers for wind monitoring. - Shift Towards Sustainable and Energy-Efficient Solutions

The focus on reducing vehicle emissions and improving road safety is driving the development of energy-efficient anemometers. - Advancements in Sensor and Communication Technologies

Innovations in sensor accuracy and real-time data processing are improving the efficiency of smart road anemometers.

Smart Roads Anemometers Market Regional Analysis :

-

North America:

Strong demand driven by EVs, 5G infrastructure, and renewable energy, with the U.S. leading the market.

-

Europe:

Growth fueled by automotive electrification, renewable energy, and strong regulatory support, with Germany as a key player.

-

Asia-Pacific:

Dominates the market due to large-scale manufacturing in China and Japan, with growing demand from EVs, 5G, and semiconductors.

-

South America:

Emerging market, driven by renewable energy and EV adoption, with Brazil leading growth.

-

Middle East & Africa:

Gradual growth, mainly due to investments in renewable energy and EV infrastructure, with Saudi Arabia and UAE as key contributors.

Smart Roads Anemometers Market Segmentation :

The research report includes specific segments by region (country), manufacturers, Type, and Application. Market segmentation creates subsets of a market based on product type, end-user or application, Geographic, and other factors. By understanding the market segments, the decision-maker can leverage this targeting in the product, sales, and marketing strategies. Market segments can power your product development cycles by informing how you create product offerings for different segments.

Key Company

- Schneider Electric

- Siemens

- Intel Corporation

- General Electric

- Accenture

- Thales Group

- ABB

- AT&T Intellectual Property

- Honeywell International Inc

- Infineon Technologies AG

- DNV GL

- ALE International

- Kapsch TrafficCom AG

- LG CNS

- Cisco

- Xerox Corporation

- Huawei Technologies Co.

- On-Premise

- On-Cloud

- Transportation and Communication Systems

- Traffic Management System

Market Drivers

- Increase in Smart Road Investments

Governments and private enterprises are heavily investing in smart road infrastructure, boosting demand for advanced anemometers. - Rising Traffic Congestion Issues

Urbanization and the growing number of vehicles are increasing the need for smart traffic management solutions. - Technological Advancements in IoT and AI

The use of AI-driven analytics and IoT sensors is enhancing the efficiency of smart roads anemometers.

Market Opportunities

- Emerging Smart City Initiatives

Increasing global initiatives for smart city development present a major growth opportunity for smart road technologies. - Growing Demand for Real-Time Traffic Solutions

The need for accurate weather and traffic data is driving the adoption of advanced anemometers. - Integration with Renewable Energy Solutions

Smart roads combined with solar and wind energy solutions offer sustainable growth prospects.

Market Challenges

- Complex Implementation Process

The integration of smart road technologies with existing infrastructure poses a significant challenge. - Technical Limitations in Extreme Weather Conditions

Harsh environmental conditions can impact the performance and accuracy of anemometers. - Limited Awareness and Adoption in Developing Regions

Many developing regions lack awareness and resources to adopt smart road solutions efficiently.

Download Free Sample Report: https://semiconductorinsight.com/download-sample-report/?product_id=82585

FAQs

Q: What are the key driving factors and opportunities in the Smart Roads Anemometers market?

Q: Which region is projected to have the largest market share?

Q: Who are the top players in the global Smart Roads Anemometers market?

Q: What are the latest technological advancements in the industry?

Q: What is the current size of the global Smart Roads Anemometers market?

The market is highly fragmented, with a mix of global and regional players competing for market share. To Learn More About the Global Trends Impacting the Future of Top 10 Companies

Related Reports:

https://sites.google.com/view/semiconductorindightreports/home/semiconductor-reports/display-driver-ic-ddic-market

https://sites.google.com/view/semiconductorindightreports/home/semiconductor-reports/industrial-igbt-power-device-market

https://sites.google.com/view/semiconductorindightreports/home/semiconductor-reports/industrial-automatic-door-sensors-market

https://sites.google.com/view/semiconductorindightreports/home/semiconductor-reports/rf-transceiver-ics-market

https://sites.google.com/view/semiconductorindightreports/home/semiconductor-reports/photomasks-for-pcb-market

https://sites.google.com/view/semiconductorindightreports/home/semiconductor-reports/machine-vision-image-acquisition-lens-market

https://sites.google.com/view/semiconductorindightreports/home/semiconductor-reports/5g-base-station-rf-chip-market

https://sites.google.com/view/semiconductorindightreports/home/semiconductor-reports/synchronous-counter-market/graphite-crystallizier-market

https://sites.google.com/view/semiconductorindightreports/home/semiconductor-reports/gas-scrubbers-for-semiconductor-market

CONTACT US:

City vista, 203A, Fountain Road, Ashoka Nagar, Kharadi, Pune, Maharashtra 411014

[+91 8087992013]

help@semiconductorinsight.com

https://semiconductorinsight.com/wp-content/uploads/2025/03/global-single-ended-triode-set-amplifiers-market-67d14e177f808-300x175.webp 300w,

https://semiconductorinsight.com/wp-content/uploads/2025/03/global-single-ended-triode-set-amplifiers-market-67d14e177f808-300x175.webp 300w,