PW Consulting: Slope Stabilisation & Erosion Control Market Set to Grow at a 6.5% CAGR in the 2026–2032 Forecast

Slope Stabilisation & Erosion Control Products Market — Strategic Outlook for 2026

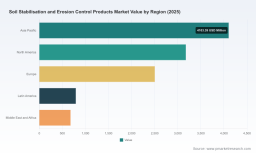

PW Consulting releases its Slope Stabilisation & Erosion Control Product Market intelligence for 2026, delivering an executive-grade briefing designed to inform capital allocation, procurement strategy, and product roadmaps. The global market reaches USD 205.5 Million in our 2025 base year and continues on a steady expansion path with a 6.5% CAGR through the 2026–2032 forecast window; by 2032 the market trajectory points to materially larger scale, underscoring why 2026 is a pivotal year for positioning.

Slope Stabilisation & Erosion Control Product Market

Why 2026 Is a Strategic Inflection Point

Several converging forces make 2026 a year for decisive action rather than incremental adjustments. Regulatory updates, renewed infrastructure cycles, shifting material economics and faster acceptance of bio-based systems are changing the specifications buyers accept and the cost structures suppliers must manage. To convert these shifts into advantage, corporate leaders must pair technical proof-points with procurement agility and targeted investments in design-win capability.

Core market dynamics

- Regulatory tightening and specification convergence — Recent standards updates and state-level mandates are raising the technical bar for temporary and permanent stabilisation; this increases the value of pre-qualified products and system-level solutions.

- Infrastructure-driven demand — Public works programs and expanding road networks remain the largest use-cases for stabilisation products; private sector landscaping and real estate projects add skewed seasonal demand, creating planning and inventory challenges for suppliers.

- Material substitution and sustainability pressure — Biopolymers and plant-derived binders gain traction as ESG criteria climb buyer scorecards, while commodity polymer price volatility reshapes supplier risk models.

- Fragmentation with pockets of scale — The market exhibits low-to-moderate concentration (CR3: 26.5%; CR5: 35.8%), meaning established players hold important advantages but there remains room for niche entrants and regional champions.

- Technical validation becomes a commercial lever — Field trials and performance metrics now determine specification listings; organizations that can supply robust, third‑party-verified evidence win longer-duration contracts.

What the PW Consulting Report Delivers — Tools for 2026 Action

Our report is explicitly designed as an operational toolset for 2026 decision-makers. It goes beyond top-line forecasts to provide applied instruments that map directly to the pain points procurement, operations, and R&D teams face this year.

- Supply-chain maps and vulnerability heat maps — Visualise supplier nodes, logistics chokepoints and single-source exposures that amplify price and delivery risk under stressed conditions.

- BOM decomposition logic — A standardised bill-of-materials break-down that enables engineers and buyers to model substitution scenarios and compare lifecycle cost impact without re-running lab tests.

- Yield-adjustment and unit-cost models — Dynamic templates that translate raw-material swings and plant yield into per-linear-metre and per-tonne cost outcomes for competing product formulations.

- Technical roadmaps and product-space matrices — A staged technology adoption roadmap showing where biopolymers, synthetic geotextiles and construction equipment interact, and what capability gaps matter for 12–36 month product planning.

- Compliance & spec-readiness playbooks — Checklists and pre-qualification tracks aligned to recent standards and major DOT specifications to accelerate approvals and reduce rollout friction.

These modules are intentionally prescriptive about process while withholding project-level proprietary parameters; they equip teams to run their own scenario runs and build internal business cases quickly.

Competitive Landscape — Dimensions that Determine Winners

Our qualitative and quantitative analysis of incumbent and adjacent players maps competitive advantage across several repeatable dimensions. Rather than publish binary rankings, we identify the vectors that determine design wins and defendable positions in 2026.

- Material IP and formulation know-how — Companies with patented polymer blends or proven biodegradable matrices can differentiate on lifecycle and environmental metrics; this matters in ESG-driven tenders.

- System integration and specification influence — Suppliers who provide hydraulically-applied systems, end-to-end erosion-control solutions, or equipment-compatible products tend to capture larger contract share through specification stickiness.

- Distribution and contractor relationships — Geosynthetics and roll products that are stocked locally and supported by contractor training secure faster adoption and repeat business.

- Performance evidence and field-validation — Documented field trials, laboratory correlation and third-party validations are decisive for public agencies and large EPCs; companies that invest in these assets convert pilot projects into regional roll-outs.

- Scale in raw-material sourcing — Players that control upstream sourcing for polymers, binders or lime enjoy margin resilience when commodity prices spike.

Illustrative company positions observed in our layered analysis include: biodegradable blanket specialists with deep brand recognition; hydraulically-applied systems vendors with system-level moats; chemical formulators providing binders and polymer emulsions; established equipment OEMs that influence specifications through installed base; and geosynthetics manufacturers with distribution-led advantage. For the full competitive scorecards, capability matrices and regional positioning, Access the full dataset and company scorecards at https://pmarketresearch.com/chemi/soil-stabilisation-and-erosion-control-products-market .

Regulatory & Standards Update — Immediate Procurement Impacts

- U.S. Army Corps of Engineers (UFS 3‑250‑11, Feb 2026) — The new supplemental guidance tightens chemical stabilisation use and constrains treatment depth for specific pavement applications; procurement teams must re-evaluate specification compliance and warranty terms.

- Virginia Transportation Research Council (Jan 2026 field evaluations) — Recent performance evaluations are being referenced in DOT approved-lists and are reshaping acceptable RECP selections on slopes and vegetation establishment.

- State DOT mandates (e.g., recent Caltrans and New York updates) — Time-bound temporary stabilisation requirements and minimum vegetative cover conditions increase the value of products with rapid germination and erosion attenuation profiles.

- Material dosing and chemistry guidance — Technical notes around fiber types and polymer dosing are influencing product formulations and contractor application standards.

Each regulatory shift shortens the runway to pre-qualification and increases the financial penalty for late compliance. These are not abstract changes: they alter specification language used in thousands of public tenders, making pre-qualification and field evidence a gating factor for 2026 revenues.

Strategic Recommendations for 2026 Capital Allocation

For C-suite and investors, the playbook for 2026 is clear: act to reduce optionality risk, accelerate specification traction, and lock-in supply flexibility.

- Prioritise modular investments — Small, targeted pilots in high-visibility projects generate specification momentum without oversized capital outlays.

- Hedge raw-material exposure — Secure alternative supply lanes for polymers and binders; consider toll-manufacturing or forward-buy programmes for critical inputs.

- Invest in field-validation — Fund controlled trials and third-party testing to convert product claims into defensible specification inclusions.

- Make ESG credentials bankable — Where procurement scores include lifecycle or carbon metrics, align product development to measurable sustainability indicators.

- Explore bolt-on acquisitions — The fragmented structure (CR5 ~35.8%) makes tuck-ins an efficient route to expand geographic reach or add complementary formulations.

How practitioners use this report in 2026

Procurement teams use the BOM and yield models to re-price long-term frameworks; product teams use the technical roadmap to prioritize R&D investments; corporate development groups use the competitive scorecards to size M&A targets. The report is formatted to move from insight to action in 30–90 day decision cycles.

Methodology — Why Our Outputs Are Actionable

PW Consulting applies a Layered Triangulation methodology combining patent-citation analysis, multi-wave primary interviews and confidential supplier audits. We calibrate public tender data and lab-test results with proprietary procurement records and on-site validation to produce reconciled estimates. Where public datasets are thin, we deploy targeted field trials and CWG (construction workgroup) interviews to capture specification adoption velocity.

To assemble non-public signals we rely on structured primary research — including vetted interviews with OEM procurement leads, anonymised supplier scorecards, and on‑project monitoring — all governed by contractual confidentiality. This approach enables us to surface near-term shifts in design-wins, supplier power, and application preferences without disclosing customer-level confidentiality.

Access and Next Steps

PW Consulting’s Slope Stabilisation & Erosion Control Product Market report is constructed to be a working resource for 2026 decision-making. For the complete regional and application distributions, downloadable toolkits (BOM templates, yield-model spreadsheets), and the full competitive appendix, visit the report page at https://pmarketresearch.com/chemi/soil-stabilisation-and-erosion-control-products-market .

Executives preparing budgets or evaluating M&A targets should prioritise rapid access to the underlying datasets; the next 12 months will separate firms that adapt specifications and supply chains from those that react to them.

For detailed analysis of this topic, please visit the official page: Slope Stabilisation & Erosion Control Product Market

Lacy Lee

Senior Marketing Manager

sales@pmarketresearch.com

00852-95632430

PW Consulting: www.pmarketresearch.com

Tags

PW Consulting

The Best-reviewed Subdivided Market Risk Analysis Firm in the US and East Asia.