PW Consulting Forecast: Fuel Cell Gasket Market Set to Expand at a Robust 16.5% CAGR Through 2032

Fuel Cell Gasket Market 2026: Strategic Imperatives from PW Consulting’s New Industry Brief

Executive summary

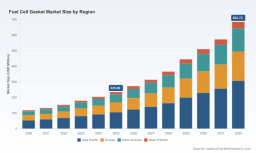

PW Consulting’s latest market research brief on the Fuel Cell Gasket market—anchored on a 2025 base year and projecting to 2032—sets out the commercial and technical playbook that will matter to executives making 2026 investment, sourcing, product and M&A decisions. The global market has shown accelerating momentum, growing from roughly USD 118 million in 2020 to about USD 235 million in 2025, and PW Consulting projects sustained expansion through the forecast horizon at a compound annual growth rate of 16.5%. By 2032 the market is expected to exceed half a billion and push toward three-quarters of a billion in USD terms, signposting clear runway for suppliers, integrators and OEMs.

Fuel Cell Gasket Market

Why this brief matters for 2026 decisions

- Timing: 2026 is the inflection point for many strategic initiatives—scale-up of PEM fuel cell vehicle programs, stationary power deployments and industrial electrolyzer rollouts—that hinge on reliable, high-performance sealing solutions.

- Commercial clarity: Our analysis translates the macro growth vector into decision-ready implications for procurement, product roadmaps, plant investments and strategic partnerships.

- Risk-adjusted playbook: The brief pairs market sizing with scenario-based sensitivity analyses (raw-material volatility, regulatory shifts, automation adoption) so leadership teams can stress-test capital allocations and supplier strategies.

Market outlook — what the numbers mean

The market trajectory is not simply growth for growth’s sake. The near-term step-up through 2026 reflects a combination of accelerating OEM programs, broader hydrogen policy support and industrial-scale electrolyzer demand. Our baseline forecast—a 16.5% CAGR from the 2025 base—reflects conservative uptake assumptions around manufacturing yield improvements, material substitution cycles, and regulatory acceptance pathways. For 2026 specifically, the market is large enough that modest shifts in material or process choices at high-volume OEMs will meaningfully affect supplier economics.

Fuel Cell Gasket Market

Key strategic implications for 2026

- Secure critical elastomer supply and hedge raw-material exposure. High-performance elastomers remain a core input; feedstock swings materially change margins. Procurement teams must combine long-term offtake with indexed contracts and examine backward integration for mission-critical compounds.

- Prioritize validation for hydrogen environments. Testing regimes that demonstrate permeation, compression set, and longevity under fuel cell operating cycles are becoming table stakes. Companies that can certify material suites quickly will secure OEM design wins.

- Invest in automation and process reproducibility. Recent industry moves demonstrate gains from automated dispense and UV/fast-curing approaches that shorten cycle time and improve seal consistency. Capital plans in 2026 should evaluate modular automation cells that scale with product ramps.

- Design for material substitutability. With regulatory pressure mounting on PFAS-containing or restricted chemistries, R&D pipelines must prioritize low-Risk alternative chemistries that meet durability targets without requiring full system redesigns.

- Reassess channel and service models. Given the moderate concentration in the supplier base, partnerships and co-development agreements (rather than pure supplier contracts) will accelerate time-to-market while reducing total cost of ownership for OEMs.

What the PW Consulting report delivers

This brief is an abbreviated, strategic extract of the full PW Consulting Fuel Cell Gasket Market report. The full deliverable is designed as a practical toolkit for 2026 action planning and includes:

Fuel Cell Gasket Market

- Detailed market sizing and forecasting methodology (transparent assumptions, demand drivers and sensitivity levers).

- Scenario modelling (base / accelerated / conservative) that quantifies outcomes for procurement, capex and gross margin under plausible 2026–2030 regimes.

- Supplier scorecards and a CR-mapped competitive positioning framework to help sourcing teams prioritize Tier-1 vs. Tier-2 engagements.

- Technology readiness assessments for core materials (silicones, EPDM, FKM, TPE) and assembly processes including dispensing, molding and post-cure strategies.

- Manufacturing playbooks—layout, cycle time optimization and automation blueprints tailored to fuel cell stack assembly lines.

- Regulatory and standards tracking with action items for PFAS alternatives, hydrogen safety certification and component-level test protocols.

- Commercial playbook for partnerships, IP protection, and an M&A roadmap highlighting attractive target profiles and valuation levers.

Note: The full report contains comprehensive regional and application splits, granular pricing sensitivity tables and downloadable build‑cost models. Those datasets are intentionally withheld from this summary to preserve research value and are available via the PW Consulting report portal.

Competitive landscape — who to watch and why

The sector is characterized by a mix of global sealing specialists, elastomer formulators, and vertically integrated automotive suppliers. Market concentration is meaningful but not prohibitive: the top three firms capture a sizable share of commercial sealing platforms, and the top five firms together form a dominant cluster—creating both opportunity and headwinds for mid‑market entrants.

- Freudenberg Sealing Technologies (Weinheim): Long-standing strength in elastomer sealing and increasing alignment of hydrogen component businesses into core sealing competence following a 2026 organizational integration. Their mix of material know-how and system integration capability positions them well for OEM stack programs and supplier consolidation dynamics.

- NOK Corporation (Tokyo): Deep expertise in integrated separator and gasket designs that improve power-density and water management in PEM stacks. Their engineering-led approach makes them a preferred partner for efficiency-seeking OEMs.

- Trelleborg Sealing Solutions (Trelleborg): Focused product validation for hydrogen environments with purpose-developed materials, offering a strong proposition for customers prioritizing permeation control and safety compliance.

- Parker Hannifin (Cleveland): Broad portfolio including PTFE and injected elastomer seals with high-temperature options—relevant where multi-chemistry or fuel-agnostic solutions are required.

- ElringKlinger (Dettingen): Bridging metal-elastomer hybrid gaskets and e-mobility heritage; recent trade-event showcases signal an intent to leverage thermal and mechanical sealing expertise into fuel cell architectures.

- Specialized players (Stockwell, Takaishi, Nitto Denko, Sumitomo Riko, AVK GUMMI and several regional manufacturers): These firms supply advanced silicone and EPDM formulations, niche die-cutting and thin‑section gasket technologies that matter at volume production and for specific stack designs.

Recent activity underscores market dynamics: automated dispensing system launches, technology showcases at major mobility events, and organizational integrations that signal renewed focus on hydrogen sealing solutions. Collectively these moves point to a market shifting from prototype validation to production readiness.

Manufacturing and supply‑chain dynamics

- Raw-material sensitivity: High-performance elastomers and specialty fluoropolymers exhibit geographic pricing and availability volatility. Scenario testing in our model shows that sustained feedstock price inflation materially compresses supplier margins unless mitigated by index-linked pricing, forward purchases or reformulation.

- Process automation and throughput: Adoption of high-speed dispensing, UV or hybrid curing technologies reduces cycle variability and scrap—critical when scale is necessary to capture 2026 production orders.

- Quality and traceability: As product volumes grow, traceability from raw material batch to final gasket becomes a commercial differentiator—customers will increasingly demand documented test histories and field performance data.

Risk framework & sensitivity

Our report provides a compact risk matrix for 2026 planning, focused on three levers:

- Input-cost shock (raw elastomer and additive price swings).

- Regulatory shift (accelerated restrictions on legacy chemistries and the pace of PFAS alternatives adoption).

- Technical acceptance risk (time-to-qualification for new materials and assembly processes).

Each lever is accompanied by mitigation playbooks: contractual strategies, dual‑sourcing templates, accelerated test programs and go/no-go decision gates for capital deployment.

How to use this brief in board and operational planning

- For boards: Use the market sizing and concentration analysis to validate capital allocation for 2026 and evaluate M&A targets that shorten time-to-design-win.

- For procurement leaders: Activate the supplier scorecards, initiate long-term supply negotiations and pilot index-linked contracts for elastomer purchases.

- For R&D/product teams: Prioritize candidate chemistries for PFAS-free roadmaps and accelerate joint validation programs with strategic OEM partners.

- For manufacturing leaders: Evaluate modular automation investments that can be scaled with product ramps and incorporate inline quality checkpoints to reduce rework.

Conclusion and next steps

The Fuel Cell Gasket market is at a commercially significant juncture in 2026. The size and compound growth trajectory create multiple paths to value: capture of production volume, leadership in validated material systems, and consolidation plays that centrally position sealing specialists in hydrogen value chains. PW Consulting’s full report equips executives with the quantitative detail, scenario analytics and supplier intelligence required to convert market opportunity into sustainable advantage.

To access the complete dataset—regional and application splits, downloadable cost models, the supplier CR-mapped scorecards and the full list of assumptions used in our 2026 scenarios—please visit the PW Consulting report page. The condensed insights in this brief are intentionally strategic; the full report operationalizes them into executable 2026 action plans.

For detailed analysis of this topic, please visit the official page: Fuel Cell Gasket Market

Lacy Lee

Senior Marketing Manager

sales@pmarketresearch.com

00852-95632430

PW Consulting: www.pmarketresearch.com

Tags

PW Consulting

The Best-reviewed Subdivided Market Risk Analysis Firm in the US and East Asia.